The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively. With IRS enforcement activity increasing, a poorly documented study can mean deductions reversed, penalties applied, and tax savings lost. This guide breaks down what the ATG requires, what the IRS scrutinizes during an audit, and how to build a study that withstands examination.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | — |

| January 1, 2023 – December 31, 2023 | 80% | TCJA phase-down |

| January 1, 2024 – December 31, 2024 | 60% | TCJA phase-down |

| January 1, 2025 – January 18, 2025 | 40% | TCJA phase-down |

| January 19, 2025 – December 31, 2030 | 100% | Applies if acquisition date is January 19, 2025 or later |

| 2025 (if acquisition date is before January 19, 2025) | 40% | TCJA phase-down still in effect |

| 2026 (if acquisition date is before January 19, 2025) | 20% | TCJA phase-down still in effect |

TLDR

- The IRS ATG defines what a "quality" study looks like and what gets flagged during audits

- Engineering-based studies prepared by qualified professionals with construction and tax credentials meet IRS quality standards

- Compliant studies require thorough documentation, precise component classification, and full reconciliation to actual costs

- Common audit triggers include rule-of-thumb methods, inadequate documentation, and asset misclassification

- Working with CCSP-certified, engineering-based providers reduces audit risk and supports defensible results

What Is the IRS Cost Segregation Audit Techniques Guide?

The Cost Segregation Audit Techniques Guide (ATG) is an internal IRS reference document used by revenue agents to guide the examination of cost segregation claims. While it is not binding law, it functions as the IRS's public playbook, showing taxpayers and preparers exactly what standard of quality the IRS expects.

The ATG was last updated on February 6, 2025, incorporating changes related to the Inflation Reduction Act, Section 179D deductions, bonus depreciation, Qualified Improvement Property (QIP), and industry-specific guidance for residential rental properties. The 2025 update also includes refined technical guidance on electrical distribution systems, parking structures, and detailed cost estimate approaches.

The ATG carries a strict disclaimer: "This document is not an official pronouncement of the law or the position of the Service and cannot be used, cited, or relied upon as such." Despite that, tax professionals treat it as the practical compliance standard — it shows exactly how IRS examiners evaluate studies.

The ATG doesn't dictate which methodology is "required," but it makes clear which approaches produce defensible studies and which are most likely to be challenged.

What the IRS Looks For in a Quality Cost Segregation Study

The ATG defines two linked standards: a "quality cost segregation study" (the analytical process) and a "quality cost segregation report" (the documented output). Both must meet specific criteria for an examination to conclude favorably.

Study Methodology: The IRS Preferred Approach

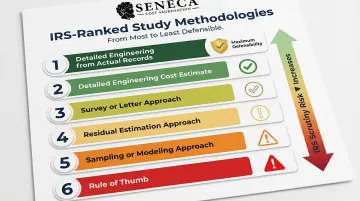

The ATG outlines six study methodologies, ranked from most to least defensible:

Detailed engineering from actual records – Uses contemporaneous construction and accounting records. The ATG calls this "the most methodical and accurate approach, relying on solid documentation of the construction costs and minimal cost estimating."

Detailed engineering cost estimate approach – Similar to actual cost approach but estimates costs using construction-based documents when actual records are unavailable.

Survey or letter approach – Relies on contacting contractors and suppliers to provide cost breakdowns after the fact.

Residual estimation approach – Subtracts estimated short-lived asset costs from total project cost, assigning the remainder to the building. The ATG warns this method "can also be less accurate."

Sampling or modeling approach – Uses a model to analyze multiple identical facilities. Examiners note that improper sampling may not reflect a valid estimate.

Rule of thumb – Based on preparer's "experience" or industry averages. The ATG explicitly warns: "An examiner should view this approach with caution since it lacks sufficient documentation to support its allocation of project costs."

Methodology Quick Reference:

| Rank | Methodology | Defensibility |

|---|---|---|

| 1 | Detailed engineering from actual records | Highest — "most methodical and accurate approach" |

| 2 | Detailed engineering cost estimate approach | Strong when actual records are unavailable |

| 3 | Survey or letter approach | Moderate — post-fact contractor/supplier breakdowns |

| 4 | Residual estimation approach | Lower — "can also be less accurate" |

| 5 | Sampling or modeling approach | Moderate risk if sampling is improper |

| 6 | Rule of thumb | Lowest — examiners warned to "view this approach with caution" |

The practical takeaway: rule-of-thumb methods invite scrutiny, while detailed engineering from actual records gives examiners little to challenge.

Preparer Qualifications

The ATG stresses that studies must be prepared by "qualified individuals" with demonstrated competency in construction processes, tax law, and depreciation rules. No formal IRS certification exists, but the ATG assumes studies come from "professional firms" competent in design, construction, auditing, and estimating.

The Certified Cost Segregation Professional (CCSP) designation from the American Society of Cost Segregation Professionals (ASCSP) is the recognized credential that signals this expertise to examiners. Earning CCSP status requires a minimum of 7 years and 7,000 hours of direct experience, a sample report submission, references, and a written exam. The ATG notes that studies conducted by construction engineers are more reliable than those from preparers without a construction background — and quality studies explicitly document preparer credentials, experience, and expertise.

Components of a Quality Study and Report

Examiners expect specific elements in both the study process and the final report. The following represent the most audit-critical requirements in each category:

| Quality Study Requirements | Quality Report Requirements |

|---|---|

| Preparation by an individual with direct construction expertise | Executive summary and narrative methodology section |

| Detailed methodology description with appropriate documentation | Asset and cost schedules organized by recovery period |

| Legal analysis supporting each property classification | Engineering procedures description with preparer certification |

| Engineering take-offs with unit cost determination | Statement of assumptions and limiting conditions |

| Reconciliation of all allocated costs to actual project costs | Exhibits including cost reconciliations and photographs |

| Identification of Section 1245 property and treatment of indirect costs | Legal citations supporting every classification |

The ATG specifies additional sub-elements within each category. Studies missing the core components above are the most frequent targets during examination.

Documentation Standards

Examiners look for:

- Construction invoices and contractor pay applications (AIA Forms G-701, G-702, G-703, G-704)

- As-built drawings and blueprints

- Change orders and purchase agreements

- Appraisals and cost certifications

- Engineering take-offs with derived unit costs

When estimates are unavoidable, the methodology behind those estimates must be especially well-documented. Thin documentation is a losing position in Tax Court.

In AmeriSouth XXXII, Ltd. v. Commissioner (T.C. Memo. 2012-67), the taxpayer sought to reclassify over 1,000 components to shorter recovery periods. The court sided with the IRS on nearly every count — not because the reclassifications were inherently wrong, but because the taxpayer couldn't produce evidence that the assets were non-permanent or regularly replaced.

How to Build an Audit-Ready Cost Segregation Study

Building a study that withstands IRS scrutiny requires a methodical, stage-by-stage approach grounded in what the ATG actually requires.

Step 1 – Identify the Property and Confirm Eligibility

Confirm that the property qualifies: newly constructed, recently purchased, or significantly renovated real estate placed in service after 1986. Key property types covered include:

- Commercial buildings (offices, retail, warehouses)

- Industrial facilities (manufacturing, distribution centers)

- Multi-family properties (apartments, condominiums)

- Short-term and long-term rentals

- Owner-occupied businesses

- Medical facilities and hotels

Both residential rental property (27.5-year recovery) and non-residential real property (39-year recovery) qualify for cost segregation, with components reclassified to 5-, 7-, or 15-year schedules. Cost segregation becomes cost-effective for properties with a depreciable basis starting at $300,000 (excluding land value), with optimal ROI typically occurring at $450,000 or higher.

Step 2 – Engage Qualified Professionals Early

The IRS's own guidance points to the value of engaging professionals with engineering, construction, and tax expertise before the study begins—not after. Credentials the IRS looks for in a preparer include:

- CCSP certification

- Licensed engineer on staff

- Experience with actual construction documentation

- Demonstrated competency in tax law and depreciation rules

Firms like Seneca Cost Segregation pair licensed engineers with CCSP-certified professionals to meet exactly these standards — combining construction documentation expertise with working knowledge of depreciation rules before a single component is classified.

Step 3 – Gather Source Documents and Conduct Site Analysis

Documentation collected at this stage should include:

- Architectural drawings or blueprints

- Purchase agreements and closing statements

- Construction contracts and invoices

- Change orders and cost certifications

- Previous depreciation schedules

- Property tax records and appraisals

A physical site visit (or detailed virtual inspection for remote properties) is critical for accurate component identification. The IRS accepts virtual inspections using video walkthroughs as compliant with ATG guidelines. Virtual inspections typically take 30 to 45 minutes and can reduce study completion time to 2-3 weeks compared to 4-6 weeks for on-site visits.

Contemporaneous documentation—gathered at or near the time of construction or acquisition—is more defensible than reconstructed records. When actual costs are unavailable, the documentation of the estimation methodology itself becomes critical.

Step 4 – Classify and Cost Each Component

With source documents in hand, every building component must be individually identified, classified into the correct depreciation category, and assigned a defensible cost basis. The classification process applies the Whiteco six-factor test, a legal standard that evaluates whether property qualifies as tangible personal property (5-7 year) or structural components (27.5-39 year).

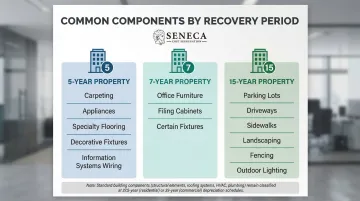

Common Components Reclassified to Shorter Lives

| Recovery Period | Typical Components |

|---|---|

| 5-year | Carpeting, appliances, specialty flooring, decorative fixtures, information systems wiring |

| 7-year | Office furniture, filing cabinets, certain fixtures |

| 15-year | Parking lots, driveways, sidewalks, landscaping, fencing, outdoor lighting |

Electrical and Complex System Allocations

For electrical distribution systems, the IRS requires a "functional allocation approach" based on electrical demand load. The portion feeding building equipment remains 39-year property; the portion allocable to process machinery qualifies as Section 1245 property.

Studies must document load studies referencing National Electric Code (NEC) panel schedules and kilo-Volt Amp (KVA) splits.

Misclassification, in either direction, is a primary audit trigger. General HVAC and plumbing serving the building remain 39-year property unless the "sole justification" test is met, meaning the system was installed solely to meet temperature or humidity requirements essential for specific equipment.

Step 5 – Assemble the Report and Reconcile to Costs

The report must meet the ATG's "quality report" standard:

- All asset schedules must reconcile to the tax basis or purchase price

- Allocated costs must tie back to actual invoices or documented estimates

- The report must include a certification statement from the preparer

- Engineering calculations and legal citations must support every classification

- Hundreds of photographs and blueprints with personal property highlighted

This reconciliation step separates a defensible report from one that invites challenge. The IRS explicitly requires that studies "reconcile allocated costs to actual costs to ensure the accuracy of an allocation."

Common Mistakes That Trigger IRS Scrutiny: How to Avoid Them

Common Audit Triggers at a Glance

| Mistake | Description | IRS Risk |

|---|---|---|

| Rule-of-thumb methods | No engineering analysis or site review; lacks component-level detail | High |

| Inadequate or missing documentation | Missing invoices, construction docs, or methodology narrative | High |

| Misclassification of structural components | Aggressive reclassification without documented legal analysis | High |

| Not using qualified preparers | Studies by generalist accountants without engineering credentials; contingency fee arrangements scrutinized | High |

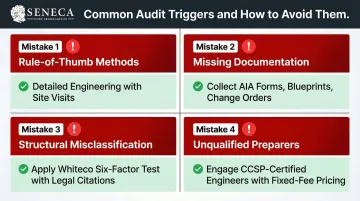

Mistake 1: Relying on Rule-of-Thumb Methods

Studies using industry averages or percentage-based shortcuts with no engineering analysis or site review are the most likely to be challenged. These studies often lack the component-level detail the IRS requires and cannot be substantiated during an examination. The ATG's explicit language warns examiners to "view this approach with caution since it lacks sufficient documentation."

Compliant approach: Detailed engineering from actual cost records with site visits, component-by-component analysis, and documented engineering take-offs produces the substantiation the IRS requires.

Mistake 2: Inadequate or Missing Documentation

Studies that lack supporting invoices, construction documents, or a clear methodology narrative give IRS examiners immediate grounds for disallowance. When actual costs are unavailable (for example, acquisition of a used building), the documentation of the estimation methodology itself becomes critical, and many studies fail here.

Compliant approach: Compliant studies include original construction records, AIA payment applications, blueprints, and change orders. When using estimates, the engineering methodology is documented with cost guides, unit costs, and reconciliation to total project cost.

Mistake 3: Misclassification of Structural Components

Certain components, including HVAC systems serving only general building climate, standard electrical panels, and structural elements, must remain as 39-year property unless specific use-case criteria are met. Overly aggressive reclassification without documented legal analysis is a common red flag.

The 2025 ATG added specific guidance on two frequently misclassified assets:

- Primary electrical switchgear: new allocation guidance clarifies treatment

- Stand-alone open-air parking structures: confirmed as 39-year property, not 15-year land improvements

Compliant approach: The Whiteco six-factor test is applied, the "sole justification" analysis is documented for specialty systems, and legal citations support every classification decision.

Mistake 4: Not Using Qualified Preparers

The IRS ATG references the need for studies conducted by "professional firms" competent in construction, engineering, and tax law. Studies prepared by generalist accountants without engineering support or cost segregation-specific credentials draw more IRS scrutiny.

The ATG also warns that contingency fee arrangements "create the incentive to maximize the amount of costs attributed to Section 1245 property, usually through 'aggressive' legal interpretations" and instructs examiners to "closely scrutinize" these studies.

Compliant approach: Studies by CCSP-certified professionals at firms with licensed engineers on staff and fixed-fee pricing structures face reduced IRS scrutiny.

How Seneca Cost Segregation Can Help

Seneca Cost Segregation's methodology prioritizes IRS compliance at every step: engineering-based studies, licensed engineers on staff, CCSP certification, and proprietary technology tested for compliance. Over 10,200 studies have been completed nationwide with an average first-year deduction of $171,243.

The AuditDefense program addresses audit risk directly. A study's real quality shows when it faces IRS scrutiny. If an audit results in a depreciation adjustment greater than 5% due to a Seneca error, the firm refunds 100% of the cost segregation services fees.

Full IRS audit representation and defense is also included at no additional charge for as long as you own the property.

Studies are completed within 2-4 weeks for properties with moderate complexity and readily available documentation. Seneca serves all 50 states with both virtual and on-site inspection capabilities.

Ready to see how much you could save? Contact Seneca for a complimentary tax assessment at 503-383-1158 or info@senecacostseg.com.

Conclusion

The IRS ATG sets a clear standard for what a defensible cost segregation study looks like: engineering methodology, qualified preparers, thorough documentation, and component-level cost reconciliation. Following that standard protects the tax savings you've earned and keeps them secure long after the study is filed.

The right time to think about audit readiness is before the study is conducted, not after a notice arrives. Investors who engage qualified, engineering-based professionals from the start protect both their deductions and their peace of mind. Seneca Cost Segregation backs every study with an AuditDefense guarantee, meaning if the IRS questions your deductions, you have a team of engineers and tax professionals ready to respond. With bonus depreciation provisions continuing to offer significant first-year deductions, getting the methodology right from day one matters more than ever.

Frequently Asked Questions

What is the cost segregation method?

Cost segregation is a tax strategy that identifies building components eligible for shorter depreciation schedules (5, 7, or 15 years) instead of the standard 27.5 or 39 years. This allows property owners to front-load deductions and reduce taxable income in the early years of ownership, improving cash flow and enabling faster reinvestment.

What are the requirements for a cost segregation study?

The IRS ATG sets four core requirements for a valid cost segregation study:

- Prepared by qualified professionals with engineering and tax expertise

- Uses an appropriate methodology (detailed engineering from actual cost records is preferred)

- Thoroughly documents all asset classifications

- Includes a report reconciling allocated costs to actual costs, with preparer certification

Can you use cost segregation on residential rental property?

Yes, residential rental properties depreciated over 27.5 years qualify for cost segregation. Components like appliances, carpeting, cabinetry, specialty flooring, and land improvements can be reclassified to shorter depreciation lives, often generating first-year savings of $40,000 to over $100,000 depending on property value.

Is residential rental property classified as Section 1245 or 1250 property?

The building structure itself is Section 1250 property (27.5-year for residential), but the personal property components identified through a cost segregation study, such as fixtures, appliances, and certain improvements, are reclassified as Section 1245 property with shorter recovery periods. This reclassification is precisely the goal of the study.

What is Form 3115 for cost segregation?

Form 3115 (Application for Change in Accounting Method) is filed when a taxpayer wants to claim accelerated depreciation on a property they already own. It allows them to catch up on missed deductions without amending prior returns, typically through a Section 481(a) adjustment that produces a lump-sum deduction in the year of filing.

Can you write off a cost segregation study?

Yes, the cost of a cost segregation study is generally deductible as an ordinary and necessary business expense under Section 162, though capitalization rules may apply depending on timing and property status.