Introduction

Depreciation is one of the largest recurring tax deductions available to real estate investors and property owners, yet it's also one of the most commonly mishandled — particularly when the method needs to be changed. While switching depreciation approaches may sound like a routine accounting adjustment, the IRS has strict rules governing when such changes qualify as accounting method changes under Section 446, whether formal filing is required, and which adjustments must be made.

Getting this wrong can trigger audits or cost thousands in missed deductions. For real estate investors, the stakes are especially high — improperly classifying assets or failing to correct depreciation errors can mean leaving substantial tax savings on the table, or facing penalties when the IRS comes knocking.

This article covers what qualifies as a depreciation method change, how to handle it properly, and the most common mistakes to avoid.

TL;DR

- Changing a depreciation method is usually an accounting method change under Sec. 446 and requires filing Form 3115, not amending returns

- A Section 481(a) adjustment captures cumulative differences between old and new methods across all prior years

- Negative 481(a) adjustments (under-depreciation) are fully deductible in the year of change, producing immediate tax savings

- Mathematical errors are corrected via amended returns, not Form 3115 — not every change qualifies as a method change

- Cost segregation studies frequently trigger legitimate method changes that recover missed deductions retroactively

What Qualifies as a Depreciation Method Change (vs. a Simple Correction)

Under Sec. 446, a depreciation method change means shifting from one systematic approach to computing depreciation to another. This covers changing from straight-line to declining balance, reclassifying property from a 39-year to a 5-year asset class, or correcting from an impermissible method — such as claiming no depreciation at all — to a permissible one.

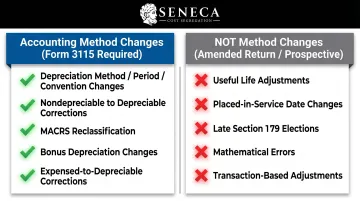

What the IRS Classifies as Accounting Method Changes

Under Treasury Regulation §1.446-1(e)(2)(ii)(d), these actions constitute accounting method changes requiring IRS consent:

- Changing the depreciation method, recovery period, or convention on a depreciable asset

- Correcting an asset from nondepreciable to depreciable status

- Changes in MACRS classification resulting in different recovery periods

- In certain circumstances, changes to or from bonus depreciation

- Treating an asset as depreciable when it was previously expensed in the year of purchase

What the IRS Does NOT Treat as Method Changes

The following corrections are handled via amended returns or prospective adjustments, not Form 3115:

- Adjustments to useful life (unless moving to or from a Code-prescribed life)

- Changes in the placed-in-service date

- Late or revoked Section 179 elections

- Corrections due to mathematical or posting errors

- Adjustments based on transactions clearly different in substance from previous events

The Two-Year Rule and Its Waiver

If an impermissible depreciation method has been used in two or more consecutively filed returns, the taxpayer has formally "adopted" that method under Rev. Rul. 90-38. Switching to the correct method then requires Form 3115 — not amended returns — even if the statute of limitations remains open for those prior years.

That said, the IRS has waived the two-year rule for certain depreciation changes under Rev. Proc. 2015-13, allowing taxpayers to file Form 3115 without IRS advance consent and without the change being blocked by prior-year adoption.

How to Change Your Depreciation Method Step-by-Step

Step 1: Identify the Scope of the Change

Begin by determining which assets are affected, what depreciation method has been used, and whether that method is permissible or impermissible under applicable IRS code sections (Sec. 167, 168, 197, etc.). Confirm whether the change qualifies as an accounting method change per Treas. Reg. §1.446-1(e)(2)(ii)(d) or whether it's a correction that can be made via amended return.

Key questions to answer:

- Which properties or assets need reclassification?

- What method has been applied (straight-line, MACRS, none)?

- Is the current method permissible or impermissible under the Code?

- Does this qualify as an accounting method change or a simple correction?

Step 2: Compile Prior Depreciation Records

Gather all depreciation schedules, fixed asset registers, and tax returns for all prior years the affected property has been in service. Identify the total depreciation taken under the old method versus the total depreciation allowable under the new method for each prior year.

Required documentation:

- Complete fixed asset registers

- All prior-year tax returns

- Depreciation schedules by year

- Asset acquisition dates and costs

- Prior depreciation method documentation

Step 3: Calculate the Section 481(a) Adjustment

The 481(a) adjustment equals the difference between total depreciation claimed under the former method and the total depreciation allowable under the new method. It covers all open and closed years prior to the year of change.

Critical distinctions:

- Negative adjustment (taxpayer-favorable): You've under-depreciated — the full catch-up deduction hits in the year of change, often generating or increasing a Net Operating Loss (NOL) that offsets other income.

- Positive adjustment (unfavorable): You've over-depreciated — you recognize the excess as income, spread over four tax years. If the total is under $50,000, you may elect to include it all in the year of change.

- Basis adjustment: Under Sec. 1016(a)(2), basis must reflect the allowable — not the allowed — depreciation as of the beginning of the year of change.

Step 4: File Form 3115 (Application for Change in Accounting Method)

Most depreciation method changes qualify for automatic consent under Rev. Proc. 2015-13 and its successors, meaning no prior IRS approval is needed and there's no user fee — but the form must still be filed properly and on time.

Filing requirements:

- Attach the original Form 3115 to the timely filed tax return (including extensions) for the year of change

- Send a signed copy to the IRS national office in Ogden, UT via mail, private delivery, or designated fax

- Include the correct Designated Change Number (DCN) from the IRS list:

- DCN 7: Impermissible-to-permissible changes on assets still in service

- DCN 8: Permissible-to-permissible method (general depreciation)

- DCN 200: Permissible-to-permissible method for MACRS property

- DCN 205-207: Disposed assets (buildings, tangible property, general asset accounts)

Required attachments (Schedule E):

- Detailed description of the former and new methods

- Statement describing the business activity

- Statement of facts and law supporting the new method and asset classification

- Year the property was placed in service

- Property description, type, and use in trade or business

- Type and amount of any tax credits, subsidies, or grants received

When Should You Change Your Depreciation Method?

A depreciation method change is appropriate — and often financially beneficial — in three main situations:

- The current method is impermissible, such as when no depreciation was ever claimed on an eligible asset

- An asset was assigned the wrong recovery period, for example 39 years instead of 5 years for personal property components

- A completed cost segregation study reveals that portions of a real estate purchase should have been depreciated over shorter lives

Cost Segregation Studies: The Primary Trigger

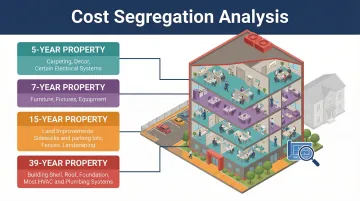

Cost segregation studies are the most common trigger for depreciation method changes. These engineering-based analyses identify building components eligible for 5-, 7-, or 15-year depreciation schedules instead of 27.5 or 39 years.

When a study is completed on a property already in service, the resulting reclassification typically requires filing Form 3115 to claim a catch-up Section 481(a) deduction for all prior missed depreciation. Industry data from over 8,000 studies shows that typically 20-30% of a property's depreciable basis is reclassified from long-life real property to shorter recovery schedules.

Example impact: On a $2 million property, reclassifying 25% of the basis ($500,000) from 39-year to 5-year and 15-year property can generate a negative 481(a) adjustment exceeding $150,000 in the year of the study — an immediate, often six-figure deduction.

Seneca Cost Segregation has assessed over 10,200 properties nationwide and offers complimentary feasibility analyses to help investors determine whether a method change is warranted before committing to a study.

When Caution Is Required

A change is not recommended or requires careful planning when:

- The 481(a) adjustment will be positive (meaning income must be recognized)

- The property is already under IRS examination without proper notification procedures

- Disposition of the property has already occurred (different rules apply for disposed-asset method changes under DCNs 205-207)

Key Variables That Affect Your Depreciation Method Change Outcome

Getting the filing right is only part of the equation. These four variables determine whether your depreciation method change delivers maximum savings — or creates an unexpected tax bill.

Variable 1 — Direction of the 481(a) Adjustment

A negative (favorable) adjustment means an immediate deduction — potentially large enough to generate a net operating loss that offsets other income in the year of change. A positive adjustment works the other way: income is recognized over four years, gradually increasing tax liability and reducing cash flow throughout the adjustment period.

Variable 2 — Asset Classification and Recovery Period

The recovery period assigned to each asset — 5-year, 7-year, 15-year, 27.5-year, or 39-year — determines the depreciation method, rate, and total deduction size. Misclassification is one of the most common and costliest errors in this process.

Common recovery periods under IRC §168:

| Property Type | Recovery Period | Convention |

|---|---|---|

| Computers, vehicles, equipment | 5 years | Half-year / Mid-quarter |

| Office furniture, fixtures | 7 years | Half-year / Mid-quarter |

| Land improvements (paving, fences) | 15 years | Half-year / Mid-quarter |

| Residential rental property | 27.5 years | Mid-month |

| Nonresidential real property | 39 years | Mid-month |

Reclassifying even a moderate share of a building's cost into shorter-lived asset categories can produce six-figure deductions in the year of change.

Variable 3 — Timing of the Change (Year of Change Selection)

The year designated as the "year of change" controls when the 481(a) adjustment hits and which tax return Form 3115 must accompany. Filing in a high-income year maximizes the value of a negative adjustment. Delay carries real risk — if tax rates shift or the property sells before the change is filed, the benefit can shrink significantly.

Variable 4 — Whether the Property Has Been Disposed Of

Disposed property follows a separate set of rules. Key differences include:

- Different Form 3115 change codes apply (DCNs 205–207)

- The year of disposal becomes the year of change

- Gain/loss character can shift between capital and ordinary income

Correcting depreciation on a sold asset directly affects how sale proceeds are taxed. Section 1250 recapture is taxed at up to 25%, while long-term capital gains may qualify for significantly lower rates — so getting the classification right on disposed property has real dollar consequences.

Common Mistakes When Handling Depreciation Method Changes

Mistake 1 — Amending Returns Instead of Filing Form 3115

Many taxpayers and even some preparers attempt to correct multi-year depreciation errors by filing amended returns for each prior year. This is incorrect once the impermissible method has been used for two or more consecutive years.

Correct approach: File a single Form 3115 in the year of change, with the full 481(a) catch-up taken in that year. Amended returns are only appropriate for mathematical errors, one-year corrections, or when the two-year adoption rule hasn't been triggered.

Mistake 2 — Failing to Attach Required Statements or Using the Wrong Change Code

Form 3115 has specific attachment requirements and designated change codes (e.g., DCN 7, 8, 200, 205-207). Submitting a vague description of the method change or using the wrong code can result in rejection or audit scrutiny.

Rev. Proc. 2022-14 explicitly states that general descriptions like "MACRS to MACRS," "erroneous method to proper method," or "claiming less than the depreciation allowable to claiming the depreciation allowable" are unacceptable and will cause the application to fail.

Always provide a detailed description of the former and new methods, including specific asset classes, recovery periods, and conventions — vague descriptions are a common and avoidable rejection trigger.

Mistake 3 — Ignoring the "Allowed or Allowable" Rule When Selling Property

Under Sec. 1016(a)(2), basis must be reduced by the depreciation that was allowable — not just what was actually claimed. Failing to account for this before selling means an underreported gain and potential penalties.

If you never claimed depreciation — or claimed less than allowable — you still must reduce your basis by the full allowable amount when calculating gain on sale. That means paying tax on "phantom" depreciation you never actually deducted.

Filing Form 3115 before or at the time of disposition closes this gap. It aligns claimed depreciation with allowable depreciation, so you capture the deduction before recognizing gain.

Frequently Asked Questions

How is a change in depreciation method accounted for?

A depreciation method change is treated as an accounting method change under Sec. 446. The taxpayer files Form 3115 for automatic IRS consent and calculates a Section 481(a) adjustment capturing the cumulative difference between the old and new methods across all prior years.

What is the journal entry for the change in depreciation method?

For tax purposes, the 481(a) adjustment is recorded as a deduction or income item in the year of change, not spread across prior years. Under GAAP, a depreciation method change is treated prospectively under ASC 250 as a change in accounting estimate, so prior periods are not restated.

How to account for change in depreciation rate?

A change in depreciation rate (such as moving from one recovery period to another) that involves a Code-prescribed life is treated as an accounting method change, requiring Form 3115 and a 481(a) adjustment. A non-Code useful life adjustment is handled prospectively without a 481(a) adjustment.

Is changing depreciation method a change in accounting policy?

For tax purposes, it's a Sec. 446 accounting method change requiring Form 3115 and a 481(a) adjustment. For GAAP/IFRS, a change in depreciation method is generally considered a change in accounting estimate, applied prospectively, not retrospectively — meaning prior periods are not restated under financial accounting standards.

Can a company change its depreciation method?

Yes, but the company must follow IRS procedures: filing Form 3115 for automatic consent and making the required 481(a) adjustment. Both permissible-to-permissible and impermissible-to-permissible changes qualify for automatic consent with no user fee.

What are the methods of changing depreciation?

The main pathways are: (1) filing Form 3115 under automatic consent for most method changes including impermissible-to-permissible corrections; (2) filing an amended return in limited cases (mathematical errors, one-year errors, or certain elections); and (3) prospective adjustment for non-method-change corrections like useful life estimates not tied to a Code-prescribed life.