Introduction

Most real estate investors who complete a cost segregation study leave significant tax savings on the table — not because the study was wrong, but because they filed it incorrectly. Form 3115, the IRS Application for Change in Accounting Method, is the required form for switching to accelerated depreciation schedules. Without it, changing depreciation numbers on your return creates compliance gaps and eliminates audit protection.

This guide is for property owners, real estate investors, and their CPAs who have completed (or are considering) a cost segregation study and need to understand how to correctly implement it on a tax return. Whether your property was placed in service last year or a decade ago, Form 3115 determines how you claim missed depreciation.

By the end, you'll know exactly how to file Form 3115, calculate the Section 481(a) catch-up adjustment, and decide whether it beats amending prior returns for your situation.

TL;DR

- Form 3115 is required when applying cost segregation retroactively to property depreciated under slower methods

- Section 481(a) adjustment lets you claim all missed depreciation in one tax year — no amended returns needed

- No IRS approval or user fee required — it files as an automatic change under DCN 7

- Filing Form 3115 is faster than amending prior returns and bypasses the three-year amendment statute

- The bonus depreciation rate used depends on the property's placed-in-service year, not when you file

What Is Form 3115 and Why Does Cost Segregation Require It?

Form 3115 (Application for Change in Accounting Method) is the 8-page IRS form used to formally change how you account for an item. In cost segregation contexts, this means changing from depreciating all building components over 27.5 or 39 years to reclassifying components into 5-, 7-, and 15-year asset classes under MACRS.

Without filing Form 3115, the IRS has no record of the method change. Reporting different depreciation numbers on your return without the form makes your filing non-compliant and eliminates audit protection — even when you're moving from an impermissible method to a permissible one.

Form 3115 is a formal request to change accounting methodology, not a correction for a math error or an optional election. It's typically automatic for cost segregation, covering future depreciation plus a one-time catch-up for prior years. Different IRS rules and procedures apply to method changes versus corrections or elections, so the category your filing falls into has real consequences.

The MACRS Reclassification

Cost segregation reallocates building costs from §1250 real property into §1245 tangible personal property and land improvements. Instead of waiting 27.5 years (residential) or 39 years (commercial) to depreciate everything, you accelerate components across shorter recovery periods.

| Asset Class | Recovery Period | Common Examples |

|---|---|---|

| Personal property | 5 years | Carpets, appliances, decorative fixtures |

| Personal property | 7 years | Furniture, office equipment |

| Land improvements | 15 years | Landscaping, parking lots, site improvements |

| Real property | 27.5 / 39 years | Structural components, building shell |

This reclassification is the accounting method change that triggers the Form 3115 requirement.

Who Needs to File Form 3115 for Cost Segregation?

Any property owner who has been depreciating a property under the standard method and now wants to apply accelerated depreciation through a cost segregation study must file Form 3115 for the year the change is applied. This applies to individuals, partnerships, S-corporations, and C-corporations.

The Look-Back Scenario

If you perform a cost segregation study on a property placed in service in a prior year—even many years prior—Form 3115 lets you claim all missed depreciation in the current tax year without amending every prior return.

There is no statutory limit on how far back a look-back study can reach using Form 3115—unlike the standard three-year amendment window. The Section 481(a) adjustment captures the cumulative depreciation difference "without regard to the statute of limitations," per the IRS Internal Revenue Manual. That means a property acquired a decade ago can still generate a substantial catch-up deduction today.

The Study Foundation Matters

A high-quality, engineering-based cost segregation study is the essential foundation for a defensible Form 3115 filing. The study must include:

- A cost summary allocating total building costs across applicable class lives

- A component-level cost detail with individual class life assignments

- Engineering methodology from qualified construction or engineering professionals (the IRS actively prefers this over non-engineering approaches)

Meeting that engineering standard matters when the IRS reviews a Form 3115 filing. Seneca Cost Segregation's engineering team has completed over 10,200 studies across all 50 states, and every study includes AuditDefense coverage—so the documentation supporting your Section 481(a) adjustment is built to hold up under scrutiny.

How to File Form 3115 for a Cost Segregation Study

Form 3115 is 8 pages, but only 4 pages typically need completion for a standard cost segregation change. The form is filed in duplicate:

- Original: Attached to your tax return

- Signed copy: Mailed to the IRS National Office in Ogden, UT

Current mailing addresses (verify before filing):

- Standard mail: Internal Revenue Service, Ogden, UT 84201, Attn: M/S 6111

- Private delivery: Internal Revenue Service, 1973 N. Rulon White Blvd., Ogden, UT 84201, Attn: M/S 6111

- Fax: 844-249-8134

Understanding the DCN (Designated Change Number)

The DCN identifies the type of change you're making. For cost segregation method changes, use DCN 7 (Impermissible to permissible method of accounting for depreciation) per IRS Rev. Proc. 2025-23, Section 6.01. This number goes on Part I, Line 1a.

DCN 7 qualifies as an automatic change, meaning no IRS approval is required before filing and no user fee is required.

Step 1: Complete the Cost Segregation Study

Complete the cost segregation study before filing Form 3115. You'll need two documents:

- Cost Summary: Allocates total building cost across class lives

- Cost Detail: Lists individual components (cabinets, flooring, parking lots, etc.) and their assigned class lives

Both must be attached to or referenced in the Form 3115 filing — they're the supporting documentation the IRS expects to see if your return is examined.

Step 2: Complete the Key Pages of Form 3115

Each page serves a specific purpose. Here's what to complete and what to skip for a standard cost segregation filing:

Page 1:

- Enter taxpayer information (name, address, EIN/SSN)

- Check "Depreciation or Amortization" box

- Complete Part I with DCN 7

- Answer Part II questions

Page 2:

- Answer standard questions (most will be "No" for a typical cost seg filing)

Page 3:

- Complete Part II continuation questions

- Part III generally does not apply — it covers non-automatic changes

Pages 4–7:

- Left blank for cost segregation-only filings

- These schedules apply to inventory methods, long-term contracts, and other accounting changes

Page 8 (Schedule E):

- Answer questions about the depreciation change

- Attach a statement describing:

- The property (address, type, placed-in-service date)

- The present (incorrect) method (e.g., "straight-line over 27.5 years")

- The proposed (correct) method (e.g., "MACRS with accelerated schedules for reclassified components")

- How the change affects current and future years

Step 3: Calculate and Report the Section 481(a) Adjustment

Part IV of Form 3115 is where you report the Section 481(a) catch-up adjustment: the net additional depreciation you're claiming in the year of change. This figure drives the tax benefit, so accuracy here matters most. The detailed calculation section below covers how to derive it.

Step 4: File with the Tax Return

Timing is critical:

- The original Form 3115 attaches to your timely filed (including extensions) federal tax return for the year of change

- A signed duplicate copy must be sent to the IRS National Office no earlier than the first day of the year of change and no later than the date the original is filed

- The IRS does not issue an acknowledgment for automatic change requests

- No response is expected unless there is a problem

Important: Filing only the original or only the duplicate creates a procedural defect that can void automatic consent and eliminate audit protection.

How to Calculate the Section 481(a) Adjustment

The Section 481(a) adjustment is the "catch-up" amount: the difference between total depreciation that was actually claimed under the old method and what would have been claimed under the accelerated method from the original placed-in-service date through the beginning of the year of change. This entire amount is deducted in the year of change.

Calculation Logic by Asset Class

For each class life identified in the cost seg study (5-year, 7-year, 15-year, 27.5/39-year):

Step 1: Determine what total depreciation should have been taken from the placed-in-service date to the start of the year of change using the correct MACRS method and rates for each class.

Step 2: Subtract what was actually claimed under the old 27.5- or 39-year method.

Step 3: The positive difference is the 481(a) adjustment for that class.

Step 4: Sum all class-level adjustments to get the total 481(a) adjustment.

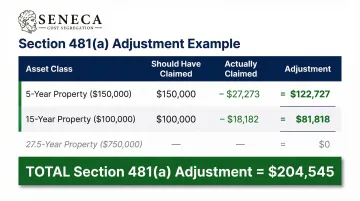

Numerical Example

Assume you purchased a $1 million residential rental property in 2020 and have been depreciating it straight-line over 27.5 years. In 2025, you complete a cost segregation study that reclassifies the basis as:

- 5-year property: $150,000

- 15-year property: $100,000

- 27.5-year property: $750,000

Calculate the 481(a) adjustment for years 2020-2024 (5 years):

Note: These examples assume 100% bonus depreciation was available in the placed-in-service year.

5-year property ($150,000):

- Should have claimed (MACRS + 100% bonus): $150,000

- Actually claimed (straight-line 27.5): $27,273

- Adjustment: $122,727

15-year property ($100,000):

- Should have claimed (MACRS + 100% bonus): $100,000

- Actually claimed (straight-line 27.5): $18,182

- Adjustment: $81,818

27.5-year property ($750,000):

- Should have claimed (straight-line 27.5): $136,364

- Actually claimed: $136,364

- Adjustment: $0

Total Section 481(a) adjustment: $122,727 + $81,818 = $204,545

This $204,545 is deducted in 2025 (the year of change) in addition to your current-year depreciation.

Bonus Depreciation and the Placed-in-Service Year Rule

The bonus depreciation percentage applied through the 481(a) adjustment is determined by the year the property was placed in service, not the year Form 3115 is filed.

Recent legislative changes: The One, Big, Beautiful Bill Act (OBBBA) of 2025 restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. However, for properties placed in service before that date, the phase-down schedule still applies:

| Placed-in-Service Date | Bonus Depreciation |

|---|---|

| Sept 28, 2017 – Dec 31, 2022 | 100% |

| Jan 1, 2023 – Dec 31, 2023 | 80% |

| Jan 1, 2024 – Dec 31, 2024 | 60% |

| Jan 1, 2025 – Jan 19, 2025 | 40% |

| After Jan 19, 2025 | 100% |

Example: If your property was placed in service in 2023, you use the 80% bonus rate for your 481(a) calculation, even if you file Form 3115 in 2025.

How the 481(a) Adjustment Flows Through Your Return

For rental properties, the 481(a) adjustment typically flows through Schedule E as "other expenses." The passive or non-passive character of the catch-up deduction is determined by the activity's status in the year of change, not the original placed-in-service year.

Real Estate Professional Status (REPS) advantage: If you qualify as a real estate professional under IRC § 469(c)(7) and materially participate in the rental activity during the year of filing Form 3115, the 481(a) adjustment is treated as non-passive. That means it offsets active income, even if the activity generated passive losses in prior years.

Form 3115 vs. Amending Your Tax Return

Choosing between Form 3115 and amending prior returns is one of the most consequential filing decisions a real estate investor faces — and the right answer depends on your specific tax situation.

Core Distinction

| Form 3115 | Amended Returns |

|---|---|

| Forward-looking accounting method change | Corrects errors within specific prior years |

| Pulls all missed depreciation into current year | Refund limited to specific years amended |

| No statute of limitations on look-back period | Subject to 3-year statute for refund claims |

| One filing (plus duplicate to IRS) | Must amend each year separately |

| No "sandwiched year" complications | Can create housekeeping issues |

| Lower professional fees | Higher fees (multiple returns) |

| Audit protection for prior years not under exam | Prior years remain open if amended |

When Amending Makes More Sense

Amending a prior-year return may be more advantageous when:

- A specific prior year had unusually high income

- You qualified as a real estate professional (REPS) in a prior year but not currently

- You used the short-term rental loophole in a prior year

- The refund opportunity in that specific year is substantial

- The statute of limitations is still open for that year

Example: Say you had $500,000 of active income in 2022 when you qualified as a real estate professional, but you're not a REPS in 2025. Amending 2022 to claim $200,000 of cost segregation depreciation offsets that high-income year at your top tax rate.

Claiming the same amount as a 481(a) adjustment in 2025 as a passive loss, by contrast, may provide little or no current benefit.

Practical Advantages of Form 3115

For most investors, Form 3115 offers:

- Files as a single form rather than separate amendments for each prior year

- Processes faster than amended returns through the IRS

- Avoids reconciling "sandwiched" years that amendments can create

- Shields prior years from audit exposure when not already under examination

- Carries lower professional fees than amending multiple returns

Common Mistakes When Filing Form 3115 for Cost Segregation

Incomplete or Low-Quality Cost Segregation Study

The IRS Cost Segregation Audit Techniques Guide defines a "quality" study using 13 principal elements. Studies that lack engineering-based methodology, detailed component breakdowns, or clear class-life allocations create audit exposure.

What the IRS expects:

- Preparation by individuals with engineering/construction expertise

- Detailed methodology and documentation

- Determination of unit costs and engineering "take-offs"

- Proper legal analysis for §1245 vs. §1250 property classification

Simplified estimates or software-only studies without engineering validation are not adequate support for Form 3115 filings. If a study can't demonstrate compliance with these 13 elements, it's a liability — not an asset — when the IRS comes calling.

Incorrect or Missing 481(a) Calculation

One of the most common errors is calculating the catch-up depreciation incorrectly. Common mistakes include:

- Using wrong MACRS rates or recovery periods

- Skipping or miscounting prior-year deductions already claimed

- Applying the wrong bonus depreciation percentage (using current year instead of placed-in-service year)

- Failing to attach a detailed computation statement showing how the adjustment was derived

IRS expectation: The IRS expects to see the math. Your Form 3115 should include a statement showing the calculation by asset class, with clear documentation of what was claimed versus what should have been claimed.

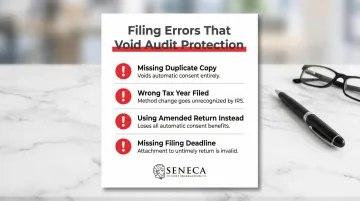

Filing Errors That Reduce Audit Protection

Procedural errors can void automatic consent and eliminate audit protection:

- Failing to send the duplicate copy: Not filing the signed duplicate with the IRS National Office in Ogden violates automatic change procedures

- Filing for the wrong tax year: Form 3115 must be filed for the year the change takes effect, not retroactively for a prior year

- Using amended returns where Form 3115 is required: Attempting to amend when a method change is required eliminates the benefits of the automatic consent procedure

- Missing the filing deadline: Form 3115 must be attached to a timely filed return (including extensions)

Any of these errors gives the IRS grounds to reverse the method change upon examination. That means reverting to the original — and incorrect — depreciation method. It can also trigger penalties for prior years where the wrong method was applied.

Frequently Asked Questions

Does cost segregation require Form 3115?

When a cost segregation study is applied retroactively to a property already placed in service, Form 3115 is required to formally change the accounting method. If cost segregation is applied in the same year the property is placed in service for the first time, you simply adopt the correct MACRS methods on your original return—no Form 3115 is needed.

How do I enter cost segregation on my tax return?

Cost segregation is reflected through updated depreciation schedules that split previously single-line assets into multiple class-life entries, and through the Section 481(a) catch-up deduction reported on Form 3115. For rental properties, the increased depreciation flows through Schedule E.

Who needs to file Form 3115?

Any taxpayer — individual, partnership, S-corporation, or similar entity — changing their depreciation accounting method must file Form 3115. This includes property owners doing a look-back study on properties held for one year or more.

Can I apply Form 3115 to a property I've owned for several years?

Yes. Form 3115 can be used to retroactively apply cost segregation to properties owned for many years with no statutory cutoff on how far back the look-back can reach (unlike the 3-year amendment window). The Section 481(a) adjustment captures all missed depreciation since the placed-in-service date, no matter how many years have passed.

How do I get Form 3115?

Form 3115 is available directly from the IRS website at IRS.gov. The December 2022 revision is the current version, with instructions published separately by the IRS.