Introduction

For real estate investors, the difference between choosing the right and wrong depreciation method can mean tens of thousands of dollars in tax savings—or missed opportunities—every year. A $1,000,000 property depreciated using the standard straight-line method delivers roughly $36,000 in annual deductions over 27.5 years. That same property, analyzed through cost segregation and paired with bonus depreciation, can generate over $250,000 in first-year deductions alone.

Most property owners default to straight-line depreciation simply because their CPA files the return that way. But the IRS offers faster, fully compliant methods that front-load deductions, improve cash flow, and accelerate wealth building. This guide breaks down each method, when it applies, and how to determine which approach generates the most after-tax value for your portfolio.

TL;DR

- The IRS requires MACRS for real estate — residential rentals depreciate over 27.5 years, commercial property over 39 years

- Bonus depreciation and cost segregation front-load deductions into year one, boosting near-term cash flow

- Bonus depreciation is now permanently restored at 100% for property placed in service after January 19, 2025

- Your ideal method depends on property type, tax bracket, income classification, holding period, and reinvestment goals

- Cost segregation reclassifies 20–40% of building costs into 5-, 7-, and 15-year categories — unlocking immediate deductions few investors use

What Is Depreciation and Why Does It Matter for Real Estate Investors?

Depreciation allows property owners to recover the cost of income-producing assets over their useful life, reducing taxable income each year the asset remains in service. The IRS treats buildings as depreciating assets—physical structures wear out—so you deduct a portion of the purchase price annually.

What qualifies as depreciable real estate:

- Residential rentals depreciate over 27.5 years under MACRS GDS

- Commercial properties use a 39-year recovery period

- Land improvements (parking lots, sidewalks, fencing) qualify as 15-year property

- Land itself is never depreciable

Why this matters financially:

A $750,000 single-family rental (excluding land) generates $27,273 in annual depreciation under straight-line MACRS. At a 37% marginal tax rate, that's $10,091 in annual tax savings each year.

Run that same property through cost segregation, and the math shifts sharply. Identifying $180,000 in short-lived components eligible for 100% bonus depreciation means a $180,000 year-one deduction—$66,600 in immediate tax savings at the same rate.

The Joint Committee on Taxation notes that accelerated depreciation allowances lower the user cost of capital and increase the present value of after-tax cash flows compared to straight-line methods. A dollar recovered now compounds faster than the same dollar claimed a decade from now.

Depreciation Methods for Real Property: Know Your Options

The IRS recognizes multiple depreciation methods, each with different timing and deduction profiles. Understanding these options is the first step to optimizing tax outcomes.

Straight-Line Depreciation (MACRS Default)

This is the default method for real property: equal deductions each year across the asset's recovery period (27.5 or 39 years). A $1,100,000 commercial building depreciates at $28,205 annually for 39 years.

It's simple, predictable, and requires no special elections. The tradeoff: it's the slowest path to recovering your investment, spreading deductions across decades.

Accelerated Depreciation (Declining Balance Under MACRS GDS)

MACRS allows 200% or 150% declining balance methods for certain personal property components within a real estate asset: fixtures, appliances, and specialty electrical systems. These methods front-load deductions in early years.

One important constraint: the full building structure defaults to straight-line under GDS. Declining balance applies only to tangible personal property reclassified through cost segregation.

Bonus Depreciation

Bonus depreciation allows investors to immediately deduct a large percentage of eligible property costs in the year placed in service. Under the One Big Beautiful Bill Act (Public Law 119-21), 100% bonus depreciation is permanently restored for qualified property acquired and placed in service after January 19, 2025.

What qualifies:

- Property with a recovery period of 20 years or less

- Personal property and land improvements reclassified through cost segregation

- New and used property (unlike prior law)

What doesn't qualify:

- Buildings depreciated over 27.5 or 39 years (unless reclassified)

- Property subject to the Alternative Depreciation System (ADS)

Section 179 Expensing

Section 179 allows a dollar-capped immediate deduction for qualifying property placed in service during the tax year. For 2025, the maximum deduction is $2,500,000, with a phase-out beginning at $4,000,000 in total property placed in service.

The critical difference from bonus depreciation comes down to losses:

- Section 179 cannot create a net loss — it's capped at taxable income from the active conduct of any trade or business

- Bonus depreciation can generate a loss carryforward, giving real estate investors with large capital expenditures more flexibility

Alternative Depreciation System (ADS)

ADS mandates longer recovery periods and straight-line depreciation. ADS applies to:

- Foreign-used property

- Tax-exempt use property

- Real property trades or businesses electing out of the IRC §163(j) interest deduction limitation

ADS extends recovery periods significantly compared to standard MACRS:

| Property Type | GDS Recovery Period | ADS Recovery Period |

|---|---|---|

| Residential rental | 27.5 years | 30 years |

| Commercial real property | 39 years | 40 years |

Property required to use ADS is not eligible for bonus depreciation.

Key Factors to Consider When Choosing the Best Depreciation Method

The "best" method isn't universal—it depends on your financial situation, goals, and property characteristics. Consider these decision variables:

Property Type and Asset Classification

Residential rentals (27.5 years) and commercial properties (39 years) have different default recovery periods. But many property components — flooring, fixtures, specialty HVAC, land improvements — qualify for 5-, 7-, or 15-year lives.

Why classification matters:

A $1,200,000 apartment building might have $300,000 in personal property and land improvements eligible for 5- and 15-year depreciation. Proper classification makes that $300,000 eligible for immediate deductions under 100% bonus depreciation, versus spreading it over 27.5 years.

Current Tax Bracket and Income Type

High-income investors in upper tax brackets (35–37%) benefit most from front-loaded deductions. But passive activity rules complicate the picture.

Passive activity limitations:

Depreciation deductions from rental property are passive losses, which can only offset passive income — unless you qualify as a real estate professional.

Non-real estate professionals can deduct up to $25,000 in rental losses against nonpassive income if they actively participate. That allowance phases out completely when modified adjusted gross income (MAGI) exceeds $150,000.

Real estate professional exception:

You avoid passive loss limits if you:

- Perform more than 750 hours of services in real property trades or businesses during the year

- Spend more than half of your total working hours in those activities

Cash Flow Needs and Reinvestment Goals

A large deduction now is worth more than the same deduction spread over 27 years (time value of money). Investors looking to reinvest tax savings into additional properties benefit most from accelerated strategies.

Example:

$100,000 in year-one tax savings reinvested at a 10% annual return grows to $259,374 over 10 years. The same $100,000 spread evenly over 10 years ($10,000 annually) grows to just $175,312. Front-loading saves you $84,062 in future value.

Planned Holding Period

Your reinvestment strategy is only half the equation. How long you plan to hold the property shapes which depreciation approach actually pays off — investors with long-term holds face different tradeoffs than those planning to sell within five years.

Depreciation recapture:

When you sell, the IRS taxes depreciation deductions taken as unrecaptured Section 1250 gain at up to 25%. Personal property (Section 1245) recapture is taxed as ordinary income. Plan for this when modeling exit scenarios.

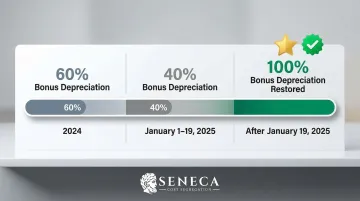

Year-of-Purchase Timing and Current Bonus Depreciation Rules

The year property is placed in service determines which bonus depreciation percentage applies. Under current law, property placed in service after January 19, 2025, qualifies for 100% bonus depreciation.

Key dates:

| Placed in Service | Bonus Depreciation Rate |

|---|---|

| 2024 | 60% |

| January 1–19, 2025 | 40% |

| After January 19, 2025 | 100% (permanent) |

How Cost Segregation Amplifies Your Depreciation Benefits

Cost segregation is an IRS-compliant engineering study that reclassifies components of a real estate asset from 27.5- or 39-year property into 5-, 7-, or 15-year categories. Instead of waiting decades to recover costs, you deduct a significant portion in the first few years.

What gets reclassified:

- 5-year property: Carpeting, decorative finishes, specialty electrical

- 7-year property: Furniture, fixtures, equipment

- 15-year property: Parking lots, sidewalks, landscaping, site utilities

Dollar Impact

According to industry benchmarks, 20-40% of a building's components typically qualify for shorter depreciation schedules. For a $750,000 single-family rental, a cost segregation study identifying $180,000 in short-lived assets generates $59,415 in first-year federal tax savings at a 37% bracket with 100% bonus depreciation—compared to $10,091 under straight-line alone.

Interaction with Bonus Depreciation

When cost segregation reclassifies assets into 5-, 7-, or 15-year property, those assets also qualify for bonus depreciation. Under 100% bonus depreciation, you deduct the entire reclassified amount in year one, compounding the benefit significantly.

Who Benefits Most

- Property owners with buildings valued at $500,000 or more

- Investors who recently purchased or renovated a property

- High-income earners looking to offset taxable income

- Investors planning to reinvest tax savings into additional acquisitions

Timing matters: studies initiated at acquisition or immediately after a major renovation capture the largest reclassifiable asset pool—and generate the biggest first-year deduction.

How Seneca Cost Segregation Can Help You Maximize Deductions

Seneca Cost Segregation is a veteran-owned, engineering-based firm with over 12 years of experience and more than 10,200 studies completed nationwide. Their approach is built on IRS-compliant methodology, backed by AuditDefense and a money-back guarantee.

Key differentiators:

- Studies completed within 2–4 weeks

- Average first-year deduction of $171,243

- Complimentary tax assessments covering retirement loss deductions, partial disposition analysis, and energy efficiency credits

- 95% client referral rate across more than 10,200 completed engagements

Seneca serves all 50 states, providing property-level evaluations that match each investor to the depreciation strategy that fits their situation. Whether you're optimizing a recent acquisition, planning a renovation, or running a lookback study on a property held for years, their engineering team delivers the analysis needed to capture the largest available deductions.

Ready to assess whether your property qualifies? Seneca's team can evaluate your specific situation and deliver a detailed estimate of your potential tax savings.

Frequently Asked Questions

What is the best method of depreciation for tax purposes?

For most real estate investors, MACRS is the required IRS framework. Accelerated strategies like cost segregation and bonus depreciation typically deliver the greatest tax benefit by front-loading deductions in early ownership years, which improves cash flow and speeds up reinvestment.

How do I know which depreciation method to use?

The right method depends on property type, tax bracket, income classification (passive vs. active), holding period, and cash flow goals. A qualified tax advisor or cost segregation specialist can match the right method to your specific situation and keep you IRS-compliant.

Is it better to take Section 179 or bonus depreciation?

Section 179 has a $1,220,000 deduction cap (2024) and cannot create a net loss, while bonus depreciation has no income limitation and can generate a loss carryforward. Bonus depreciation is generally more flexible for real estate investors with large capital expenditures, especially when combined with cost segregation.

What depreciation method is required by the IRS?

The IRS requires MACRS for property placed in service after 1986, with residential rental property depreciated over 27.5 years and commercial property over 39 years by default. Investors can elect bonus depreciation, Section 179, or ADS under specific qualifying conditions.

Do companies prefer straight-line or accelerated depreciation?

For tax purposes, most real estate investors benefit more from accelerated methods because they reduce taxable income sooner. Straight-line is simpler and often preferred for financial reporting. The two aren't in conflict — you can use accelerated methods for tax filings and straight-line for book reporting simultaneously.

Which method of depreciation is most commonly used for tax purposes?

MACRS is the most commonly used system for tax purposes in the U.S. Straight-line depreciation serves as the MACRS default for real property. Many experienced investors layer in bonus depreciation or cost segregation studies to accelerate recovery beyond what standard MACRS delivers.