Introduction

Commercial property owners making interior improvements forfeit tens of thousands of dollars in immediate tax deductions by misunderstanding Qualified Improvement Property (QIP) rules. A tenant finish-out costing $300,000 might generate $180,000 in first-year deductions if properly classified, or just $7,700 if treated as standard real property. That's $172,000 in lost cash flow that could have funded your next acquisition.

This guide covers:

- What QIP is and which improvements qualify

- How the 15-year depreciation schedule and bonus depreciation work together

- How engineering-based cost segregation studies identify components eligible for faster write-offs than QIP alone provides

TLDR

- QIP is interior improvements to nonresidential buildings made after the building's original placed-in-service date

- Qualifies for 15-year depreciation and 100% bonus expensing, for property placed in service after January 19, 2025

- Excludes building enlargements, elevators, and structural framework, but roofs and exterior HVAC qualify for Section 179

- Cost segregation studies identify renovation components qualifying as 5- or 7-year property, pushing deductions further than QIP alone

What Is Qualified Improvement Property?

Qualified Improvement Property (QIP) is any improvement made to the interior of a nonresidential building placed in service after the building's original in-service date. IRC Section 168(e)(6) governs these rules.

Two critical conditions must both be met:

- Only improvements you commission and pay for qualify. A buyer cannot treat work done by a previous owner as QIP.

- The building must be nonresidential real property. Residential rental properties, including apartment complexes and long-term rentals, do not qualify.

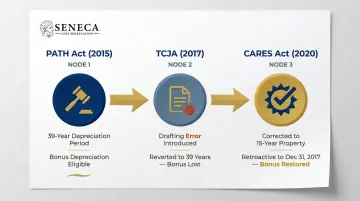

Legislative History That Shapes Today's Rules

QIP's current treatment reflects three major legislative actions:

| Act | Year | Effect on QIP |

|---|---|---|

| PATH Act | 2015 | Introduced QIP at a 39-year recovery period, eligible for bonus depreciation |

| Tax Cuts and Jobs Act (TCJA) | 2017 | Intended to assign QIP a 15-year life but inadvertently omitted the designation due to a drafting error, making QIP ineligible for bonus depreciation and defaulting it to 39 years |

| CARES Act | 2020 | Issued a retroactive technical correction assigning QIP a 15-year recovery period under MACRS GDS (20 years under ADS). This restored bonus depreciation eligibility for property placed in service after December 31, 2017 |

That legislative history sets the framework — but QIP eligibility also hinges on a precise timing rule.

Timing Requirement: "After the Building"

Improvements made simultaneously with the building's initial placement in service do not qualify as QIP. The improvement must come after the original in-service date, even if only by one day.

Example: You construct a new office building and complete tenant build-outs before opening. Those build-outs are not QIP because they were placed in service at the same time as the building. However, renovations to that same space two years later would qualify.

What Qualifies as QIP and What Doesn't

What Typically Qualifies

Interior improvements to nonresidential buildings that meet QIP criteria include:

| Interior Improvement | QIP Status |

|---|---|

| Interior non-load-bearing drywall partitions | Qualifies |

| Interior finish work (ceilings, painting, wall coverings) | Qualifies |

| Interior lighting fixtures serving general illumination | Qualifies |

| Interior plumbing for bathrooms and kitchens | Qualifies |

| Interior HVAC components (VAV boxes, interior ductwork, zone controls) | Qualifies |

Three Statutory Exclusions

Even if an improvement is interior and nonresidential, it is disqualified if it involves:

- Building enlargements: Additions that expand the building's footprint

- Elevators and escalators: New installations or modernizations

- Internal structural framework: Load-bearing walls, beams, structural supports

Common Items That Do NOT Qualify

Several common improvements fall outside QIP because they are exterior components:

| Item | QIP Status | Alternative Treatment |

|---|---|---|

| Roofs | Does not qualify | Excluded from QIP, but replacements on nonresidential buildings may qualify for Section 179 immediate expensing |

| Exterior HVAC equipment (rooftop units, chillers, outdoor condensers) | Does not qualify | Section 179 may apply |

| Windows | Does not qualify | Fail the interior requirement regardless of the improvement scope |

Residential vs. Nonresidential Distinction

Improvements to residential rental properties do not qualify as QIP. Under IRC Section 168(e)(2)(A)(i), the IRS classifies a building as residential rental property when 80% or more of its gross rental income comes from dwelling units.

Short-term rental (STR) properties that fall below the 80% threshold may be classified as nonresidential, making interior improvements potentially QIP-eligible. STR classification typically turns on whether average guest stays run under 7 days and how rental income is structured.

The Flooring Gray Area

Flooring classification determines depreciation treatment:

| Flooring Type | Classification | Depreciation Treatment |

|---|---|---|

| Removable flooring (carpet, modular tile) | Personal property | Not QIP, but eligible for 5- or 7-year accelerated depreciation |

| Permanently attached flooring (glued-down hardwood, poured concrete) | Real property | Can qualify as QIP with a 15-year recovery period |

Getting this wrong means leaving accelerated depreciation on the table. An engineering-based cost segregation study identifies which flooring assets qualify for each treatment and documents the classification in a format that holds up to IRS scrutiny.

How QIP Depreciation Works

Standard Depreciation Treatment

QIP is depreciated using the straight-line method over a 15-year recovery period under MACRS General Depreciation System (GDS). Under the Alternative Depreciation System (ADS), which is required for businesses electing out of the Section 163(j) interest limitation, the recovery period extends to 20 years.

QIP defaults to the half-year convention unless the mid-quarter convention applies (triggered when more than 40% of total depreciable basis lands in the final quarter).

| Depreciation System | Recovery Period | When It Applies |

|---|---|---|

| GDS (standard) | 15 years | Most businesses |

| ADS | 20 years | Businesses electing out of §163(j) interest limitation |

Bonus Depreciation Eligibility

QIP qualifies for bonus depreciation, allowing a percentage of the cost to be deducted in the first year. For property acquired and placed in service after January 19, 2025, the One Big Beautiful Bill Act restored 100% bonus depreciation permanently.

If you elect out of bonus depreciation for the 15-year property class, QIP reverts to straight-line depreciation over 15 years.

Section 179 Expensing

Bonus depreciation isn't the only way to front-load your deduction. QIP also qualifies for Section 179 expensing, offering another route to immediate expensing. For 2025, the deduction limit is $2,500,000 with a $4,000,000 phase-out threshold (for property placed in service after January 19, 2025).

Key limitation: Section 179 cannot create a net taxable loss, unlike bonus depreciation. Disallowed amounts carry forward to future years.

Election Mechanics

QIP falls within the 15-year MACRS property class. One important constraint: electing out of bonus depreciation applies to the entire class. That means forfeiting bonus depreciation on every 15-year asset placed in service that year, not just QIP. The election is made at the property class level, not on an asset-by-asset basis.

QIP and the Bonus Depreciation Phase-Down

Current Bonus Depreciation Schedule

Under the TCJA, bonus depreciation was scheduled to phase down. The One Big Beautiful Bill Act (Pub. L. 119-21) restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025.

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

| Period | Bonus Depreciation % | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | — |

| January 1, 2023 – December 31, 2023 | 80% | TCJA Phase-down |

| January 1, 2024 – December 31, 2024 | 60% | TCJA Phase-down |

| January 1, 2025 – January 18, 2025 | 40% | TCJA Phase-down |

| January 19, 2025 – December 31, 2030 | 100% (if acquisition date is January 19, 2025 or later) | One Big Beautiful Bill Act |

If acquisition date is before January 19, 2025:

- 40% bonus depreciation applies in 2025

- 20% bonus depreciation applies in 2026

Strategic Implications

Whatever bonus rate applies when you place property in service, a cost segregation study determines how much of your investment qualifies for it. Identifying personal property components — 5- or 7-year assets — and reclassifying them away from 39-year treatment is what converts the applicable bonus percentage into actual first-year deductions.

Note: Tax law can change. Current bonus depreciation rules in effect at the time property is placed in service govern the applicable deduction rate.

Section 179 for Non-QIP Building Improvements

Some building improvements are excluded from QIP but still qualify for immediate expensing under Section 179, which can be just as valuable depending on your tax situation. Per IRC Section 179(d)(1)(B)(ii) and (e), eligible improvements include:

- Roofs

- HVAC property

- Fire protection and alarm systems

- Security systems

These must be placed in service after the building's original in-service date and installed on nonresidential buildings.

2025 Section 179 Limits:

| Limit Type | 2025 Amount |

|---|---|

| Maximum deduction | $2,500,000 |

| Phase-out threshold | $4,000,000 |

One important constraint: Section 179 cannot generate a tax loss. The deduction is capped at taxable income from active business operations, so in a year where income is low or zero, the deduction may be reduced or unavailable entirely. Bonus depreciation doesn't carry this restriction, which is why it's often the stronger tool for investors in early or transitional years.

How QIP and Cost Segregation Work Together

Complementary but Distinct

Cost segregation and QIP classification work together but serve different purposes:

- Cost segregation reclassifies building components into shorter depreciation lives (5-year, 7-year, 15-year personal property and land improvements)

- QIP specifically addresses interior real property improvements to nonresidential buildings at 15 years

A component initially classified as QIP may be reclassified through cost segregation into an even shorter personal property category, yielding faster deductions.

Engineering-Based Studies Maximize All Deductions

An engineering-based cost segregation study identifies:

- Which items qualify as QIP (15-year interior real property)

- Which qualify as personal property (5- or 7-year assets) eligible for even faster depreciation

- Which must remain at 39 years as structural components

Seneca Cost Segregation uses an engineering-based methodology that maps each component to the correct asset class and produces documentation aligned with the IRS Cost Segregation Audit Techniques Guide, reducing misclassification risk and supporting defensible returns.

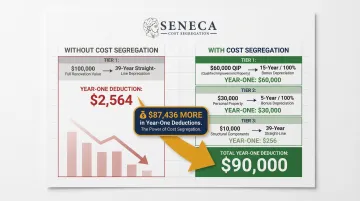

Practical Scenario

Knowing which items fall into which category changes the deduction picture significantly. A commercial property owner renovating a tenant space might assume the entire project qualifies as QIP. However, a proper engineering study may reveal that built-in cabinetry, specialized lighting, and removable fixtures qualify as 5- or 7-year personal property, yielding a larger first-year deduction than QIP alone.

What that looks like on a $100,000 renovation:

| Asset Classification | Amount | Depreciation Life | Bonus Eligible |

|---|---|---|---|

| Total renovation cost | $100,000 | — | — |

| QIP | $60,000 | 15-year | Yes (100%) |

| Personal property | $30,000 | 5-year | Yes (100%) |

| Structural components | $10,000 | 39-year | No |

Without cost segregation, you'd depreciate the full $100,000 over 39 years, producing just $2,564 in year-one deductions instead of $90,000.

Frequently Asked Questions

Who is eligible for QIP?

Any taxpayer who makes interior improvements to a nonresidential building already placed in service is potentially eligible, including property owners and tenants who commission improvements at their own expense. Residential rental property owners generally do not qualify.

Can I take Section 179 on leasehold improvements in 2024?

The TCJA eliminated the old "qualified leasehold improvement" category and replaced it with QIP, which is Section 179 eligible. Roofs, HVAC, fire protection systems, and security systems on nonresidential property also qualify for Section 179 as separate line items.

What does not qualify for qualified improvement property?

The three statutory exclusions are building enlargements, elevators/escalators, and internal structural framework. Other ineligible items include roofs, exterior HVAC equipment, windows, and any improvements to residential rental properties.

Is a new roof considered qualified improvement property?

No. A new roof is an exterior component, not an interior improvement, so it does not qualify as QIP. However, roof replacements on nonresidential buildings may qualify for Section 179 immediate expensing, subject to annual dollar limits.

Is HVAC considered qualified improvement property?

Only interior HVAC components (interior VAV boxes, interior ductwork) may qualify as QIP. Exterior HVAC equipment (rooftop units, outdoor condensers) does not qualify. Exterior HVAC on nonresidential buildings may qualify for Section 179 instead.

Is flooring a qualified leasehold improvement?

It depends on classification. Permanently affixed flooring (glued-down hardwood, poured concrete) qualifies as QIP. Removable flooring, such as carpet or raised access systems, does not qualify as QIP but may still qualify for faster depreciation under a shorter MACRS schedule.