Introduction

You've just closed on your rental property, and now you're staring at a settlement statement filled with dozens of line items totaling thousands of dollars in fees. The down payment is clear enough, but what about all those other costs—title insurance, attorney fees, recording charges, prepaid taxes, and mortgage points? Which ones can you actually deduct on your taxes?

The IRS does allow rental property owners to benefit from closing costs on their taxes, but not all costs work the same way. Some are deductible immediately in the year of purchase. Most others must be added to your property's cost basis and recovered through depreciation over 27.5 years.

A third category — selling costs — reduces your taxable gain when you eventually dispose of the property. Beyond those three buckets, advanced strategies like cost segregation can sharply accelerate how quickly you recover basis additions and offset rental income.

Understanding which closing costs fall into which bucket is critical. Miss the distinctions and you'll either leave deductions on the table or invite IRS scrutiny. Get it right and you'll maximize every dollar spent at closing — building a solid tax foundation from day one.

TLDR:

- Only three closing costs are immediately deductible: mortgage interest, prorated real estate taxes, and mortgage points

- Most settlement fees (title insurance, recording fees, legal fees) go into your property's cost basis, not a current deduction

- Selling costs like commissions reduce your taxable gain at disposition — not in the purchase year

- A few costs, such as casualty insurance premiums, can't be deducted or added to basis at all

- Cost segregation reclassifies building components into 5–15-year schedules, accelerating years of deductions into months

What Are Closing Costs on a Rental Property?

Closing costs are the fees and expenses paid to finalize the purchase of a rental property, separate from your down payment. For most transactions, these costs range from 2% to 5% of the purchase price, meaning a $400,000 rental property typically carries $8,000 to $20,000 in closing costs.

Common closing cost categories include:

- Inspection and appraisal fees covering property condition assessments and lender-required valuations

- Origination fees, underwriting charges, credit report costs, and flood certification

- Prepaid property taxes and hazard insurance premiums collected at closing

- Attorney charges, CPA consultations, and tax advisor services

- Escrow services, recording fees, transfer taxes, and title insurance premiums

- Mortgage insurance premiums, required when your down payment is below 20%

Each category gets different tax treatment under IRS rules — some are immediately deductible, others must be added to your property's cost basis and recovered through depreciation over time.

Closing Costs You Can Deduct in the Year of Purchase

According to IRS Publication 527 and official IRS guidance, only three types of closing costs qualify for immediate deduction in the year you purchase a rental property. These deductions appear on Schedule E (Form 1040) and directly reduce your taxable rental income for the year.

Mortgage Interest Paid at Closing

The interest portion of your mortgage—including any prepaid interest collected at closing for the remaining days of the closing month—is fully deductible in the year paid. Principal payments, by contrast, are never deductible.

Your lender issues Form 1098 at year-end documenting the total mortgage interest you paid. This form simplifies tax preparation and provides IRS-compliant documentation for the deduction.

Mortgage Points (Discount Points)

Mortgage points are fees paid to the lender in exchange for a reduced interest rate. Each point equals 1% of the loan amount. For example, one point on a $300,000 loan costs $3,000.

Important distinction for rental properties: Unlike primary residences where points can sometimes be fully deducted in the purchase year, rental property points must generally be deducted ratably over the life of the loan — spread evenly across each year of the loan term. If you pay $3,000 in points on a 30-year mortgage, you deduct $100 annually for 30 years. Form 1098 reports the deductible portion each year in Box 6.

Prorated Real Estate Taxes

Property taxes are prorated at closing from the purchase date through year-end. This prorated share is deductible in the year of purchase.

Example: If annual property taxes are $3,600 and you close on September 1, you own the property for four months of the tax year (September through December). Your deductible amount is $1,200 (4 months ÷ 12 months × $3,600).

One nuance worth knowing: if the seller already paid the full year's property taxes, you reimburse them at closing for your ownership period. That reimbursement appears on your settlement statement and is fully deductible — even though the payment went to the seller rather than directly to the taxing authority.

Closing Costs That Increase Your Basis (and How Depreciation Works)

Most closing costs cannot be deducted immediately. Instead, they're added to your property's cost basis, forming an "adjusted basis" that drives two critical tax calculations: annual depreciation deductions and eventual capital gains upon sale. The deduction isn't lost — it's deferred, recovered gradually through depreciation.

What Gets Added to Your Basis

IRS Publication 551 provides the authoritative list of closing costs that become basis additions:

- Abstract fees and title search costs

- Utility installation charges

- Legal fees for contract and deed preparation

- Recording fees and surveys

- Transfer taxes (state and local)

- Title insurance premiums

- Any seller-owed costs you agree to pay (such as back taxes or outstanding liens)

Not every cost qualifies for basis addition. IRS Publication 527 specifically excludes fire and casualty insurance premiums, charges for occupancy before closing, escrow amounts for future taxes and insurance, and loan-related costs (appraisal fees, credit reports, origination fees). Loan costs must be amortized separately over the loan term.

How Depreciation Recovers These Costs Over Time

The IRS allows residential rental property to be depreciated over 27.5 years using the straight-line method. Each year, you deduct 1/27.5 (approximately 3.636%) of your depreciable basis.

Step-by-step calculation:

- Determine total adjusted basis: Purchase price ($200,000) + depreciable closing costs ($5,000) = $205,000

- Exclude land value: If land represents $30,000, your depreciable basis is $175,000 ($205,000 - $30,000)

- Calculate annual depreciation: $175,000 ÷ 27.5 years = $6,364 per year

Land never depreciates and must always be excluded from the depreciable basis. At $6,364 per year, recovering a $175,000 basis takes nearly three decades. Cost segregation shortens that timeline considerably.

Cost Segregation: Accelerating Basis Recovery

Cost segregation reclassifies building components into shorter depreciation schedules, front-loading deductions into the early years of ownership. The IRS Cost Segregation Audit Techniques Guide recognizes this strategy as legitimate when supported by proper engineering analysis.

How it works: An engineering-based cost segregation study identifies components that qualify for accelerated depreciation:

- 5-year property: Appliances, carpets, window treatments, certain fixtures

- 7-year property: Office furniture and equipment

- 15-year property: Landscaping, site improvements, parking lots, fencing

Instead of depreciating these components over 27.5 years, you recover them in 5, 7, or 15 years — which means more deductions now rather than spread across decades. Seneca Cost Segregation's clients average $171,243 in first-year deductions, converting slow-drip depreciation into meaningful early-year cash flow gains.

Closing Costs When Selling a Rental Property

Selling costs are handled differently than purchase closing costs. They're not deductible as ordinary expenses; instead, they reduce the "amount realized" from the sale, which lowers your taxable gain.

Selling-side costs that reduce gain:

- Real estate agent commissions (typically 5-6% of sale price)

- Attorney fees and legal costs

- Transfer taxes and recording fees

- Title insurance fees

- Deed preparation charges

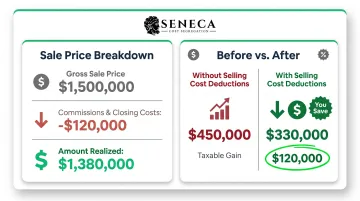

Example: You sell a rental property for $500,000 and pay $30,000 in commissions and $2,000 in other closing costs. Your amount realized is $468,000 ($500,000 - $32,000), not $500,000. This $32,000 reduction directly lowers your taxable gain.

Depreciation Recapture

When you sell, the IRS "recaptures" all depreciation deductions taken during ownership. This recaptured amount is taxed as ordinary income at a maximum rate of 25%, regardless of your actual tax bracket.

If you claimed $50,000 in depreciation over 10 years, you'll owe recapture tax of up to $12,500 (25% × $50,000) when you sell. That's a real number with real consequences — which is why thorough record-keeping of all depreciation, including accelerated depreciation from cost segregation, matters before you ever list the property.

Capital Gains Tax Considerations

Once selling costs reduce your amount realized and recapture tax is settled, any remaining gain faces capital gains tax. The rate hinges on two factors: how long you held the property and your total taxable income for the year.

2025 long-term capital gains rates (property held over one year):

- 0%: Taxable income up to $48,350 (single) / $96,700 (married filing jointly)

- 15%: Income from $48,350 to $533,400 (single) / $96,700 to $600,050 (married filing jointly)

- 20%: Income above $533,400 (single) / $600,050 (married filing jointly)

Short-term gains — property held one year or less — are taxed as ordinary income at your marginal rate, which can exceed 37% for high earners.

How to Maximize Tax Savings Beyond Closing Costs

Closing costs establish your tax foundation, but ongoing deductions provide continuous savings throughout ownership.

Annual deductions available to rental property owners:

- Mortgage interest on the full loan balance

- Repairs and maintenance (immediate deduction, unlike improvements)

- Property management fees (typically 8-10% of rent collected)

- Insurance premiums (hazard, liability, flood)

- Professional services (CPA, attorney, tax advisor fees)

- Travel expenses to inspect, maintain, or manage the property

- Qualified Business Income (QBI) deduction of up to 20% for eligible pass-through rental income

Depreciation, particularly when accelerated through cost segregation, often delivers the most powerful tax benefit of all. As a non-cash deduction, it can offset or eliminate taxable rental income entirely while your actual cash flow remains untouched.

Investors who pair a high adjusted basis (from capitalized closing costs) with a cost segregation study capture both advantages at once. A cost segregation study uses engineering analysis to reclassify property components into shorter depreciation schedules, front-loading deductions into the early years of ownership rather than spreading them over 27.5 or 39 years.

What to keep on file: Maintain your HUD-1 or Closing Disclosure statement permanently. These documents underpin all basis calculations, depreciation schedules, and eventual gain computations. A CPA with real estate experience can review these records to confirm every closing cost lands in the right category — deductible, capitalized, or basis-adjusting — before you file.

Frequently Asked Questions

Can I write off closing costs on my rental property?

Yes, but through three different mechanisms depending on the cost type. Mortgage interest and prorated property taxes are immediately deductible in the purchase year. Most settlement fees (title insurance, recording fees, legal fees) are added to your property basis and recovered through 27.5-year depreciation. Selling costs reduce your taxable gain at disposition rather than generating current deductions.

What is the $2,500 expense rule?

The IRS de minimis safe harbor rule (Reg. 1.263(a)-1(f)) allows taxpayers to deduct items costing $2,500 or less per invoice as current expenses rather than capitalizing them. The election requires written accounting procedures in place at the start of the tax year and must be applied consistently across eligible closing-related costs or property components.

How much are closing costs on a $400,000 rental property?

Closing costs typically range from 2% to 5% of the purchase price, meaning a $400,000 property generally incurs $8,000 to $20,000 in settlement fees. The exact amount depends on your loan type, lender fee structure, location (state and local transfer taxes vary widely), and whether you negotiate seller concessions to cover part of the closing costs.

What closing costs cannot be deducted or added to basis?

Certain costs fall into a third category — neither immediately deductible nor basis-eligible. IRS Publication 527 specifically identifies fire insurance premiums, pre-closing occupancy charges, escrow deposits for future taxes and insurance, and loan-related fees (appraisals, credit reports, origination fees) as non-basis items. These loan-related fees in particular catch many investors off guard, since they feel like legitimate acquisition costs but the IRS treats them differently.

Can you deduct closing costs when you refinance a rental property?

Refinancing generates a new set of closing costs with different tax treatment. Points, appraisal fees, credit reports, and recording fees are capitalized as loan costs and amortized over the life of the new loan — not deducted upfront. Mortgage interest and prorated property taxes remain immediately deductible, the same as in the purchase year.