Introduction

The BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) builds real estate portfolios through cash flow and equity capture—but the strategy's most powerful advantage is rarely the one investors talk about. Tax-free cash-out refinancing, accelerated depreciation, and cost segregation can turn 20–40% of your property costs into immediate write-offs. That's the part that actually compounds wealth.

Most BRRRR investors file returns that report passive rental income without touching the deductions that could reduce or eliminate their federal tax bill entirely. This post covers how to pull equity tax-free, how depreciation generates paper losses that offset real income, and how cost segregation front-loads those benefits starting in year one.

TLDR:

- Cash-out refinance proceeds are borrowed money, not taxable income—extract equity without IRS bills

- Depreciation creates non-cash deductions that offset rental income, often generating tax losses despite positive cash flow

- Cost segregation reclassifies components into shorter depreciation schedules, with average first-year deductions exceeding $171,000

- 100% bonus depreciation was permanently restored in 2025, making first-year write-offs larger than they've been in years

- 1031 exchanges and stepped-up basis can eliminate or defer depreciation recapture when you exit

BRRRR and Taxes: Why This Strategy Is Built for Tax Savings

BRRRR—Buy, Rehab, Rent, Refinance, Repeat—is an acquisition strategy where investors purchase undervalued properties, renovate to force appreciation, stabilize rental income, then refinance to pull equity and fund the next deal.

Unlike house flipping, which triggers ordinary income tax at rates up to 37% plus 15.3% self-employment tax, BRRRR builds wealth through equity extraction without ever triggering a taxable sale event.

The tax efficiency of BRRRR rests on three foundational pillars that this post breaks down:

- Non-taxable refinance proceeds - Extract tens or hundreds of thousands in equity without paying federal income tax at withdrawal

- Depreciation-generated paper losses - Reduce taxable income with non-cash deductions while keeping cash flow positive

- Accelerated deductions through cost segregation and bonus depreciation - Reclassify building components into shorter depreciation schedules and claim 100% bonus depreciation on qualifying assets, front-loading tax savings into year one

On top of depreciation, rental property owners deduct operating expenses—property management fees, insurance, mortgage interest, and repairs—making BRRRR among the most tax-efficient strategies in real estate.

A cash-flow-positive BRRRR property can show a tax loss on your return, sheltering other income and deferring tax bills for decades.

Tax-Free Cash-Out Refinancing: The BRRRR Investor's Secret Weapon

The Core Principle: Proceeds Are Debt, Not Income

The IRS treats cash-out refinance proceeds as borrowed money with an obligation to repay, not as taxable income. This means investors can pull out tens or hundreds of thousands of dollars in equity without paying a dollar in federal income tax at the time of withdrawal. No Form 1099, no capital gains calculation, no ordinary income reporting—just tax-free liquidity that can be redeployed immediately into the next acquisition.

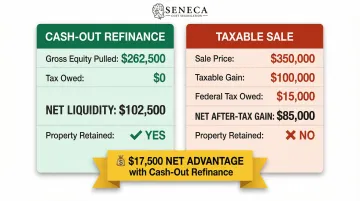

The Cost of the Alternative: Sale vs. Refinance

Consider an investor who purchases a property for $200,000, invests $50,000 in rehab, and stabilizes the property at a $350,000 after-repair value (ARV). After seasoning the property for 6-12 months, the investor refinances at 75% loan-to-value (LTV), pulling out $262,500. After paying off the original $160,000 acquisition loan, the investor nets $102,500 in cash—completely tax-free.

Now compare that to a sale scenario. If the investor sold at $350,000:

- Gross sale price: $350,000

- Less: adjusted basis ($200,000 purchase + $50,000 improvements): $250,000

- Taxable gain: $100,000

- Federal tax at 15% long-term capital gains rate: $15,000

- After-tax proceeds from gain: $85,000

The refinance strategy delivers $17,500 more in after-tax liquidity—and the investor still owns the property, continues collecting rent, and keeps all future appreciation. That retained equity goes straight toward the next acquisition instead of to the IRS.

Interest Deductibility Benefit

When refinance proceeds are reinvested into another rental property or used for business purposes, the interest on that loan is generally deductible under IRC §163. This creates a two-layer tax benefit: the cash-out itself is tax-free, and the cost of carrying that debt reduces taxable rental income going forward.

Proper interest tracing is required. If proceeds are used for personal expenses, the allocable interest is non-deductible—so document the use of funds carefully.

Basis Impact: Why Your Loan Balance Doesn't Matter

A cash-out refinance does not change the property's cost basis. Your adjusted basis remains the original purchase price plus capital improvements, minus accumulated depreciation. When you eventually sell, the taxable gain calculation uses this adjusted basis—not the current loan balance.

Three things to keep in mind:

- Basis is fixed at purchase plus capital improvements, regardless of refinancing activity

- Depreciation reduces your basis over time, increasing the eventual taxable gain

- Loan balance is irrelevant to the IRS—what you paid and what you've deducted determines your tax bill

Accurate records of every improvement and depreciation deduction taken aren't optional—they're what protect you when you sell.

The Compounding Effect: The BRRRR Flywheel in Tax Terms

Each cycle of tax-free equity extraction finances the next acquisition without triggering capital gains taxes. Using untaxed equity to acquire more cash-flowing, depreciating assets—that's the BRRRR flywheel in action.

Instead of surrendering 15-25% of your gain to the IRS every time you sell, you retain 100% of that equity to redeploy, compounding portfolio growth while pushing the tax bill further into the future.

How Depreciation Works in the BRRRR Method

Fundamentals: 27.5-Year Residential, 39-Year Commercial

The IRS allows residential rental properties to be depreciated over 27.5 years and commercial properties over 39 years. Only the building value is depreciable—land does not wear out, so it cannot be depreciated. At purchase, investors must allocate the total acquisition cost between land and building based on fair market value, often using county tax assessments or appraisals. A $300,000 purchase with a 20% land allocation means $240,000 of depreciable building basis and $60,000 of non-depreciable land.

The "Paper Loss" Concept

Depreciation is a non-cash deduction. The investor doesn't write a check to claim it, but it reduces taxable rental income on paper. A property generating $18,000 in annual rent with $240,000 in building basis depreciates $8,727 per year ($240,000 ÷ 27.5 years). If operating expenses total $6,000, the investor shows $12,000 in cash flow ($18,000 rent - $6,000 expenses) but only $3,273 in taxable income ($18,000 - $6,000 - $8,727). In many cases, depreciation turns a cash-flow-positive property into a tax loss.

Passive Activity Loss Rules

Depreciation losses from rental properties are classified as "passive" under IRC §469 and can only offset passive income. However, taxpayers who actively participate in rental real estate can deduct up to $25,000 of passive losses against non-passive income (such as W-2 wages) annually, provided their modified adjusted gross income (MAGI) is below $100,000. This allowance phases out by 50 cents for every dollar of MAGI above $100,000 — so an investor with $120,000 MAGI can deduct up to $15,000 — and disappears entirely at $150,000 MAGI.

Bonus Depreciation: 100% Restored in 2025

Shorter-lived assets classified as 5-, 7-, and 15-year property qualify for accelerated first-year deductions under bonus depreciation rules. The Tax Cuts and Jobs Act (TCJA) initially provided 100% bonus depreciation but scheduled phase-downs to 40% in 2025 and 20% in 2026.

The One Big Beautiful Bill Act (Public Law 119-21), enacted in July 2025, permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. Investors can now write off 100% of qualifying short-lived assets in year one, making front-loaded deductions larger than they've been since the TCJA's original passage.

How BRRRR's Rehab Phase Compounds the Benefit

Renovation costs that create new 5-, 7-, or 15-year assets—rather than merely extending the building's useful life—are depreciable over shorter schedules. Assets installed during the rehab phase that commonly qualify for reclassification include:

- Flooring and finish materials — 5-year property

- Specialized electrical systems — 5-year property

- Landscaping — 15-year property

- Site improvements (paving, fencing, lighting) — 15-year property

This is where BRRRR's forced-appreciation strategy intersects powerfully with cost segregation: the renovation creates a clear record of newly installed components, making cost segregation studies more precise and the reclassifiable asset pool larger.

Cost Segregation: Accelerating BRRRR Tax Savings

What a Cost Segregation Study Does

A cost segregation study is an engineering-based analysis that breaks a property into individual components and reclassifies them from 27.5-year (residential) or 39-year (commercial) real property into shorter depreciation classes. Common reclassified components include:

- Flooring and carpeting

- Cabinetry and specialty electrical

- Plumbing serving equipment

- Landscaping and site improvements

This reclassification significantly accelerates depreciation, moving deductions from decades away into the first few years of ownership.

Which BRRRR Properties Qualify

Cost segregation isn't reserved for large apartment complexes. These property types all qualify — especially after significant renovation:

- Single-family rentals

- Small multifamily properties

- Commercial buildings

Properties with a building basis (excluding land) of $300,000 or more typically justify an engineering-based study. Properties as low as $150,000–$200,000 can still be cost-effective, depending on renovation scope and study pricing.

Front-Loading Impact: Illustrative Example

Consider a BRRRR investor who purchases a single-family rental for $250,000 (with $200,000 allocable to the building) and invests $100,000 in rehab—creating a total depreciable basis of $300,000. Without cost segregation, the investor would depreciate $300,000 over 27.5 years, claiming roughly $10,909 annually.

With cost segregation, 30-40% of the $300,000 basis is reclassified into shorter-lived property:

- 5-year property (flooring, carpeting, appliances): $60,000

- 7-year property (furniture, equipment): $20,000

- 15-year property (landscaping, site improvements): $40,000

- 27.5-year property (building structure): $180,000

Applying 100% bonus depreciation to the $60,000 of 5-year property and the $20,000 of 7-year property generates an $80,000 first-year deduction. Adding standard depreciation on the 15-year ($2,667) and 27.5-year ($6,545) components, the total first-year deduction exceeds $89,000—compared to $10,909 without cost segregation. This $78,000 difference in year-one deductions can offset rental income, W-2 income (if the investor qualifies under REPS or active participation rules), and other passive income.

Seneca Cost Segregation reports an average first-year deduction of $171,243 across their client base—showing what's possible when cost segregation and bonus depreciation are combined.

The BRRRR-Specific Advantage

BRRRR investors conduct a renovation before placing the property in service, creating a clear, documented record of newly installed components. Receipts, invoices, contractor agreements, and before/after photos give engineers the foundation for precise component identification. That documentation also expands the reclassifiable asset pool beyond what a standard acquisition without capital improvements could support. The rehab phase, in other words, doubles as a tax-planning opportunity.

Seneca Cost Segregation: Engineering-Based Studies with Audit Defense

Seneca Cost Segregation provides engineering-based cost segregation studies for BRRRR and rental property investors across all 50 states. Studies are completed in 2–4 weeks and include complimentary tax strategy assessments to help investors maximize deductions within their overall tax picture. Every study is backed by AuditDefense with a money-back guarantee.

With over 10,200 properties assessed and a 95% client referral rate, Seneca's licensed engineering team produces IRS-compliant studies built to hold up under audit — so investors can reinvest their tax savings with confidence.

Depreciation Recapture and Long-Term Exit Planning

Depreciation Recapture (Section 1250)

When a property is sold, the IRS "recaptures" accumulated depreciation deductions at a rate of up to 25% under Section 1250. Investors who front-loaded deductions through cost segregation will face a larger recapture bill at sale, which is why exit planning matters from day one.

Personal property components (5- and 7-year assets reclassified through cost segregation) carry additional exposure: Section 1245 recapture, taxed at ordinary income rates up to 37%.

Three Primary Strategies to Manage or Defer Recapture

1. 1031 Exchange IRC §1031 defers both capital gains and depreciation recapture by rolling proceeds into a like-kind property of equal or greater value. Strict timelines apply: 45 days to identify a replacement, 180 days to close. When executed properly, investors can pyramid equity across multiple properties without triggering recapture or capital gains tax.

2. Long-Term Hold Strategy Refinance, never sell, and pass the property to heirs at a stepped-up basis under IRC §1014. At death, the basis resets to fair market value, which can eliminate both the embedded capital gain and depreciation recapture liability. This "buy, borrow, die" approach lets families build generational wealth while avoiding federal income tax on appreciation and accumulated depreciation.

3. Installment Sales IRC §453 allows capital gains to be recognized proportionally as payments are received, spreading the tax bill across multiple years. However, any Section 1245 or Section 1250 recapture must be recognized as ordinary income in the year of sale, even if no cash is received that year—limiting the benefit for heavily depreciated properties.

Why Front-Loading Still Wins: Time Value of Money

Even with eventual recapture, the time value of money favors taking large deductions now. Consider a $50,000 deduction in year one at a 37% rate: that's $18,500 back in your pocket immediately.

Hold the property for 20 years, and you've had two decades to reinvest and compound that $18,500 — well beyond what the eventual 25% recapture rate will cost. With the right exit strategy (a 1031 exchange or stepped-up basis at death), that recapture bill may never come due at all.

Additional BRRRR Tax Strategies Worth Knowing

Three additional strategies can extend BRRRR's tax advantages well beyond standard depreciation — each with distinct qualification rules worth understanding before tax season.

Real Estate Professional Status (REPS)

Investors who qualify as a Real Estate Professional under IRC §469(c)(7) can treat rental losses as non-passive, meaning depreciation from BRRRR properties can offset W-2 or other ordinary income without the $25,000 passive loss limitation ceiling. To qualify, an investor must:

- Spend more than 750 hours per year in real property trades or businesses

- Spend more than 50% of total working hours in real estate activities

This status materially expands BRRRR's tax impact, allowing six-figure depreciation losses to shelter high W-2 income entirely.

Short-Term Rental Loophole

BRRRR properties operated as short-term rentals (average guest stay of 7 days or fewer) may qualify under Treasury Regulation §1.469-1T(e)(3) for a separate classification that allows losses to offset non-passive income — even without REPS qualification.

If the investor materially participates in the STR activity, income and losses are treated as non-passive. This is highly fact-specific and requires CPA guidance to navigate safely.

Qualified Business Income (QBI) Deduction

Rental income from BRRRR properties may qualify for the Section 199A QBI deduction, which allows pass-through entities to deduct up to 20% of qualified business income — rising to 23% for tax years beginning after December 31, 2025 under the One Big Beautiful Bill Act.

Qualifying under the Rev. Proc. 2019-38 safe harbor requires:

- 250+ hours of rental services performed annually

- Contemporaneous records documenting those hours

- Separation of rental activity from personal use or other business activities

Frequently Asked Questions

What is the 70% rule for BRRRR?

The 70% rule is a buying guideline: investors should pay no more than 70% of the property's after-repair value (ARV) minus estimated rehab costs.

Maximum Allowable Offer = (ARV × 0.70) − Repair Costs

This ensures enough equity post-renovation to refinance profitably and recover most invested capital.

What are the tax benefits of the BRRRR method?

The main tax benefits are: tax-free cash-out refinancing proceeds, annual depreciation deductions that reduce taxable rental income, and the ability to accelerate deductions through cost segregation and 100% bonus depreciation—all without triggering a capital gains event. BRRRR shelters rental income while freeing up cash to grow your portfolio.

What is depreciation recapture and how does it affect BRRRR investors?

Depreciation recapture requires investors to pay tax on accumulated depreciation deductions when they sell—up to 25% for Section 1250 real property and up to 37% for Section 1245 personal property. BRRRR investors can defer this through 1031 exchanges or eliminate it entirely by holding until death, when heirs receive a stepped-up basis.

Can I use cost segregation on a BRRRR property?

Cost segregation works especially well on BRRRR properties because the renovation creates new, clearly identifiable assets that can be reclassified into shorter depreciation schedules. Even single-family rentals can yield significant first-year deductions when combined with 100% bonus depreciation on 5- and 7-year property.

Does Real Estate Professional Status change how BRRRR depreciation works?

Qualifying as a Real Estate Professional removes the passive loss limitation on depreciation. That means losses from BRRRR properties can directly offset W-2 or other active income. This can result in significantly larger annual tax savings—potentially sheltering six-figure incomes through accelerated depreciation strategies.