Introduction

Section 179 lets you write off the full cost of certain property in year one. But mention this to your CPA and you'll often hear that your rental doesn't qualify. Both things can be true, and the difference comes down to how your rental is structured and operated.

Section 179 isn't an automatic benefit for landlords. The IRS treats most rental activities as passive investments by default, which disqualifies them from Section 179 treatment. If your rental qualifies as an active trade or business, though, you can claim immediate first-year deductions on appliances, carpets, furniture, and more.

This guide covers everything rental property owners need to know:

- What Section 179 actually allows (and what it doesn't)

- How to determine whether your rental qualifies

- Which items are eligible for the deduction

- How Section 179 compares to bonus depreciation and cost segregation

Key Takeaways

- Section 179 covers personal property like appliances, carpets, and equipment, not building structures, land, or most improvements

- Your rental must qualify as an active trade or business; passive investors typically can't use this deduction

- Bonus depreciation is often more flexible, particularly in states that don't follow federal bonus depreciation rules

- A cost segregation study identifies exactly which components qualify, maximizing your first-year deductions

What Is Section 179 and How Does It Apply to Rental Properties?

Section 179 allows businesses to immediately deduct the full purchase price of qualifying property placed in service during the tax year. Instead of spreading deductions across an asset's useful life, you expense the entire cost in year one, a direct boost to first-year cash flow.

For rental property owners, this creates a significant opportunity. Standard real estate depreciation spreads deductions over 27.5 years for residential rentals or 39 years for commercial properties. Section 179 accelerates this substantially for qualifying items.

The 2018 Game-Changer

Before the Tax Cuts and Jobs Act (TCJA) of 2018, Section 179 could not be used for personal property in residential rental units. The TCJA removed that restriction, letting landlords expense items like appliances, carpets, and drapes in the year of purchase.

Core Limitations Still Exist

Even after the TCJA, Section 179 cannot be applied to:

- The building structure itself

- Land

- Land improvements (fences, pools, paved parking areas)

It only applies to tangible personal property and certain nonresidential building improvements.

Section 179 is one piece of a broader depreciation strategy. It works best when combined with bonus depreciation and cost segregation — which identifies additional property components eligible for accelerated deductions — based on your income levels and passive activity rules.

The Trade or Business Requirement: Does Your Rental Property Qualify?

The primary hurdle for rental property owners is the "trade or business" requirement under IRC Section 162. To claim Section 179, your rental activity must constitute an active trade or business, not a passive investment.

What "Trade or Business" Means for Landlords

The Supreme Court standard established in Commissioner v. Groetzinger requires that the activity be conducted with "continuity and regularity" and a primary profit motive. Landlords who actively manage operations, rather than simply holding property for appreciation, generally meet this threshold.

IRS Evaluation Factors

The IRS and courts evaluate whether a rental qualifies as a trade or business based on:

- Commercial properties qualify more readily than single-family homes

- Owning multiple properties demonstrates business scale

- Active management decisions (repairs, tenant screening, vendor oversight) strengthen your case

- Providing services to tenants (cleaning, maintenance, utilities) adds weight

- Short-term leases signal active business operations rather than passive holding

The "Active Conduct" Standard

Section 179 requires "active conduct" of a trade or business, a lower bar than the "material participation" test under passive activity rules. Meaningful involvement in management decisions (overseeing a property manager, making repair decisions, screening tenants) is generally sufficient. You don't need to count hours or meet strict participation tests.

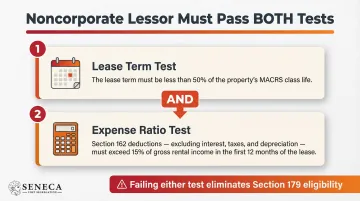

The Noncorporate Lessor Trap

Clearing the active conduct bar doesn't guarantee qualification. Individual landlords face a separate hurdle under IRC §179(d)(5). To claim Section 179, noncorporate lessors must either have manufactured the property or meet a two-part test:

| Test | Requirement |

|---|---|

| Lease term test | The lease term must be less than 50% of the property's class life |

| Expense ratio test | Allowable Section 162 deductions (excluding interest, taxes, and depreciation) must exceed 15% of rental income from that property in the first 12 months |

This is where many landlords fail. Standard 12-month residential leases often exceed 50% of the 5-year class life of appliances and furniture, and the property loses Section 179 eligibility entirely.

What Property Qualifies (and What Doesn't) Under Section 179 for Rental Properties

Personal Property Inside Rental Units

After the TCJA, these items clearly qualify for Section 179:

- Kitchen appliances (stoves, refrigerators, dishwashers)

- Carpets and area rugs

- Drapes, blinds, and window treatments

- Window air conditioning units

- Furniture (beds, sofas, tables)

- Decorative lighting fixtures

- Similar tangible personal property with useful lives of 20 years or less

Rental Business Equipment

Items used in the management of your rental business also qualify:

- Computers and office equipment

- Office furniture

- Cell phones used for business

- Maintenance equipment (lawnmowers, power tools)

- Vehicles used in the rental business

Nonresidential and Short-Term Rental Properties

Nonresidential rental properties—including commercial properties and short-term rentals with average guest stays of 30 days or less—qualify for expanded Section 179 categories that long-term residential landlords cannot access. Under IRC §179(f), the TCJA added:

- Roofing systems

- HVAC systems

- Fire protection and alarm systems

- Security systems

These four items do not qualify for Section 179 in standard long-term residential rentals.

| Improvement Type | Nonresidential / STR (avg. stay ≤30 days) | Long-Term Residential |

|---|---|---|

| Roofing systems | Qualifies | Does not qualify |

| HVAC systems | Qualifies | Does not qualify |

| Fire protection and alarm systems | Qualifies | Does not qualify |

| Security systems | Qualifies | Does not qualify |

What Does NOT Qualify

Section 179 explicitly excludes:

- Building structures and structural components

- Land

- Land improvements (fences, swimming pools, paved parking areas, landscaping, sidewalks)

- Property used outside the United States

- Inherited property

- Property received as a gift

- Property purchased from related parties (family members or controlled entities)

Key Limits, Restrictions, and Recapture Rules for Rental Property Owners

Annual Deduction Cap

The One Big Beautiful Bill Act (P.L. 119-21) raised the 2025 Section 179 deduction limit to $2.5 million, with a phase-out beginning at $4 million in total equipment purchases. For 2026, these limits adjust to approximately $2.56 million and $4.09 million respectively.

| Tax Year | Section 179 Deduction Limit | Phase-Out Begins At |

|---|---|---|

| 2025 | $2.5 million | $4 million |

| 2026 | ~$2.56 million | ~$4.09 million |

For most individual landlords, the annual cap isn't the binding constraint; the taxable income limitation is.

Taxable Income Limitation

Section 179 cannot create a net loss. The deduction is capped at your total taxable business income for the year (including W-2 wages if filing jointly). Any unused Section 179 amount carries forward indefinitely to future years, unlike bonus depreciation, which carries no income limitation.

Bonus depreciation carries no income limitation and can generate a net loss, making it applicable when a tax loss is the objective.

Section 179 Recapture

Recapture applies when an asset expensed under Section 179 ceases to be used predominantly (more than 50%) in a trade or business during its recovery period. At that point, you must recognize ordinary income equal to the Section 179 deduction claimed minus what straight-line depreciation would have allowed.

Common recapture triggers include:

- Converting the rental property to personal use

- Business-use percentage dropping below 50%

- Selling or disposing of the asset before its recovery period ends

Recapture is reported on Part IV of Form 4797 (Sales of Business Property).

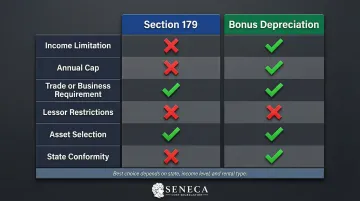

Section 179 vs. Bonus Depreciation: Choosing the Right Strategy for Rental Property Owners

Both Section 179 and bonus depreciation allow accelerated first-year deductions, but they have critical differences:

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| Income limitation | Cannot create/increase loss | No limit; can create NOLs |

| Annual cap | $2.56 million (2026) | None |

| Trade or business requirement | Yes | No |

| Noncorporate lessor restrictions | Strict two-part test applies | No lessor restrictions |

| Asset selection | Apply asset-by-asset | Must apply to entire class |

| State conformity | Most states conform | Many states decouple |

The 2025 Bonus Depreciation Update

The One Big Beautiful Bill Act restored 100% bonus depreciation for property placed in service after January 19, 2025, through 2030. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | — |

| January 1, 2023 – December 31, 2023 | 80% | TCJA phase-down |

| January 1, 2024 – December 31, 2024 | 60% | TCJA phase-down |

| January 1, 2025 – January 18, 2025 | 40% | TCJA phase-down |

| January 19, 2025 – December 31, 2030 | 100% (acquisition date January 19, 2025 or later) | OBBBA restoration |

| 2025 (acquisition date before January 19, 2025) | 40% | TCJA phase-down still applies |

| 2026 (acquisition date before January 19, 2025) | 20% | TCJA phase-down still applies |

For qualifying property with an acquisition date of January 19, 2025 or later, this delivers the larger first-year federal deduction in most scenarios. That said, federal law is only part of the picture, and where your property sits matters just as much.

State Conformity: The Deciding Factor

Many states decouple from federal bonus depreciation rules and do not allow this deduction at the state level. Major states that require full addbacks include:

| State | Treatment | State-Level Recovery Method |

|---|---|---|

| California | Full addback | Depreciate under CA rules |

| New York | Full addback | Form IT-225 |

| Pennsylvania | Full addback | Recover 3/7 of MACRS annually |

| Michigan | Full addback | Deduct pre-OBBBA amounts |

| Connecticut | Full addback | Subtract 25% over next 4 years |

| Delaware | Full addback | Follow pre-OBBBA phase-down |

In states that decouple from federal bonus depreciation, Section 179 is often the more effective accelerated depreciation strategy, even when bonus depreciation is available federally. Most states conform to Section 179 limits, so you keep the acceleration benefit at both levels rather than recapturing it on your state return.

How Cost Segregation Unlocks Greater Depreciation Benefits Alongside Section 179

A cost segregation study is the foundational tool that makes Section 179 and bonus depreciation actionable at scale. By reclassifying building components from 27.5-year or 39-year property into 5-, 7-, and 15-year property, it identifies the specific items eligible for accelerated depreciation treatment.

How Cost Segregation and Section 179 Work Together

The cost segregation study surfaces the list of qualifying assets. You and your CPA then decide which assets to expense under Section 179, which to bonus depreciate, and how to optimize across tax years based on income levels and passive activity considerations.

For example, in a typical residential rental property study, engineers identify:

| Property Class | Recovery Period | Examples |

|---|---|---|

| 5-year property | 5 years | Carpeting, appliances, decorative fixtures, non-structural cabinets |

| 7-year property | 7 years | Office furniture and equipment |

| 15-year property | 15 years | Land improvements (parking lots, fencing, landscaping) |

These reclassified components become immediately eligible for Section 179 or 100% bonus depreciation.

What a Quality Cost Segregation Study Delivers

The quality of the study determines how much you can actually claim. Seneca Cost Segregation delivers a detailed asset-by-asset breakdown (completed within 2–4 weeks and backed by an AuditDefense guarantee) that you can hand directly to your CPA and act on immediately. Across 10,200+ properties studied, the average first-year deduction reaches $171,243.

Seneca's engineers apply the Whiteco Industries factors to determine which components qualify as tangible personal property rather than inherently permanent structures, the distinction that controls whether an asset can be accelerated at all. That analysis is what separates a defensible study from one that collapses under IRS scrutiny.

Frequently Asked Questions

Can I take Section 179 on residential rental property?

Yes, Section 179 can be used for personal property items inside residential rental units (appliances, carpets, furniture) after the 2018 TCJA change. However, your rental activity must qualify as an active trade or business, and the building structure itself remains ineligible.

Can I claim 100% depreciation on my rental property?

Qualifying personal property and certain improvements can be fully expensed in year one through bonus depreciation, which was restored to 100% for assets with an acquisition date of January 19, 2025 or later. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively. The building structure itself must still be depreciated over 27.5 or 39 years. A cost segregation study pinpoints which components qualify.

What is the 50% rule in rental property?

In the context of Section 179, the 50% rule is a recapture trigger. If a deducted asset's business use drops to 50% or below during its recovery period, you must report the difference between what you expensed and what straight-line depreciation would have allowed as ordinary income.

What items qualify for Section 179 in a rental property?

Qualifying items include appliances, carpets, drapes, blinds, and office equipment used in the rental business. Nonresidential and STR properties also unlock HVAC systems, roofing, and security systems. The building structure, land, and land improvements never qualify.

What is the difference between Section 179 and bonus depreciation for rental properties?

Section 179 is capped by taxable income (cannot create a loss) and has an annual dollar limit, while bonus depreciation has no income requirement or cap. Many states do not recognize bonus depreciation, making Section 179 the preferred accelerated deduction tool in those jurisdictions.

Does Section 179 apply differently to short-term rentals?

Yes. STRs with an average guest stay of 30 days or less are treated as nonresidential property, which unlocks expanded Section 179 eligibility (including HVAC, roofing, and security systems), categories that are off-limits for traditional long-term residential rental owners.