Introduction

Cost segregation has never been more powerful. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively. Yet the results you get depend almost entirely on who conducts the study.

Bonus Depreciation Timeline

| Period | Condition | Bonus Depreciation Rate |

|---|---|---|

| Sep 27, 2017 – Dec 31, 2022 | Any | 100% |

| Jan 1, 2023 – Dec 31, 2023 | Any | 80% |

| Jan 1, 2024 – Dec 31, 2024 | Any | 60% |

| Jan 1, 2025 – Jan 18, 2025 | Any | 40% |

| Jan 19, 2025 – Dec 31, 2030 | Acquisition date on or after January 19, 2025 | 100% |

| 2025 (placed in service after Jan 19, 2025) | Acquisition date before January 19, 2025 | 40% |

| 2026 (placed in service) | Acquisition date before January 19, 2025 | 20% |

A poorly chosen provider can miss significant deductions, deliver a report that collapses under IRS scrutiny, or take months to turn around. A qualified firm can unlock six figures in first-year tax savings, documented and defensible.

The IRS Cost Segregation Audit Techniques Guide is direct on this point: studies conducted by construction engineers with detailed documentation are far more reliable than those performed without engineering backgrounds.

This guide covers what real estate investors need to evaluate before hiring a cost segregation firm:

- Key selection criteria to apply when comparing providers

- Red flags that signal a substandard or risky study

- Questions to ask before signing any engagement agreement

TLDR

- Provider quality directly affects how much you save and whether those savings hold up under IRS examination

- Evaluate credentials (ASCSP/CCSP), engineering-based methodology, audit defense policies, and verified track record

- Avoid desktop-only methods, inflated projected savings, and contingency-based pricing

- Expect flat fees based on property complexity, not percentages of savings

- The right provider delivers ongoing tax strategy, not just a one-time study

What Does a Cost Segregation Study Provider Actually Do?

A cost segregation provider delivers a detailed engineering analysis that reclassifies components of your property from the standard 27.5- or 39-year depreciation schedule into 5-, 7-, or 15-year categories, generating front-loaded tax deductions.

Under the Modified Accelerated Cost Recovery System (MACRS), residential rental property depreciates over 27.5 years and commercial property over 39 years. Without cost segregation, your entire building basis depreciates slowly using the straight-line method.

| Property Type | Standard MACRS Life | Cost Segregation Reclassification |

|---|---|---|

| Residential rental | 27.5 years | Components reclassified to 5-, 7-, or 15-year |

| Commercial | 39 years | Components reclassified to 5-, 7-, or 15-year |

A proper study identifies and reallocates portions of your building's costs to tangible personal property and land improvements, which qualify for shorter recovery periods and accelerated depreciation methods.

How much you actually recover depends heavily on who performs the study. Some licensed engineering firms conduct on-site inspections and blueprint analysis. Others offer "desktop-only" services that estimate values using cost databases without ever visiting the property, an approach the IRS explicitly views with caution.

A qualified provider delivers:

- Accurate asset identification with engineering documentation

- IRS-compliant reports meeting all 13 quality elements

- Direct delivery to your CPA with ready-to-file forms

- Ability to defend the report if challenged during an audit

Key Factors to Look for in a Cost Segregation Provider

Not all providers are equal. Factors like credentials, methodology, and experience vary dramatically across firms, and each factor has a direct impact on both your tax savings and your audit risk.

ASCSP Certification and Professional Credentials

The American Society of Cost Segregation Professionals (ASCSP) is the industry's primary credentialing body. Firms that employ Certified Cost Segregation Professionals (CCSPs) have passed rigorous exams and must adhere to professional standards and ethics.

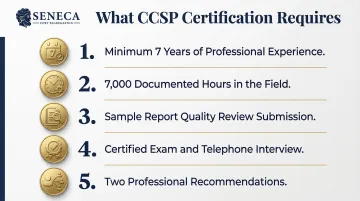

CCSP certification requires:

- Minimum 7 years of direct cost segregation experience

- Documentation of at least 7,000 hours of direct experience

- Submission of sample reports for quality review

- Passing grade on the Certified exam and telephone interview

- Recommendations from two Certified members or Board of Directors

ASCSP certification is relatively rare, making it a meaningful signal of quality. Firms with CCSP-designated professionals on staff and active involvement in industry organizations are indicators of provider quality.

Engineering-Based Methodology

Engineering-based studies and desktop-only methods are not interchangeable. Engineering-based studies include on-site inspections, blueprint analysis, and detailed asset tagging. Desktop or invoice-based methods estimate values from cost databases without field verification — a shortcut that introduces error and audit exposure.

| Feature | Engineering-Based Study | Desktop-Only Study |

|---|---|---|

| Site Inspection | On-site inspection conducted | No site visit |

| Approach | Blueprint analysis, detailed asset tagging | Cost database estimation |

| IRS ATG Alignment | "Detailed engineering approach from actual cost records" — most methodical and accurate | Viewed with caution by IRS |

| Field Verification | Yes | No |

The IRS Cost Segregation Audit Techniques Guide explicitly states that the "detailed engineering approach from actual cost records" is the most methodical and accurate approach. Studies conducted by construction engineers are generally more reliable than those done by someone without an engineering or construction background.

While the IRS doesn't legally mandate a specific methodology, the ATG states that a field inspection is "recommended for all quality studies, whether the studies are for new or used properties." That inspection documents physical details, construction materials, building systems, and property condition, the foundation for accurate asset classification.

A qualified firm can clearly and specifically walk through their inspection and classification process. Inability to answer directly is an indicator of a substandard methodology.

Audit Defense and IRS Compliance Standards

A legitimate provider should include documented methodology, supporting workpapers, and IRS-aligned classifications in every report, and should be willing to represent their findings in the event of an audit.

The IRS ATG outlines 13 principal elements that constitute a "quality" cost segregation study, including:

- Preparer qualifications and credentials

- Detailed methodology narrative

- Legal analysis with citations of regulations and rulings

- Cost source reconciliation

- Exhibits and photographs

There's a meaningful difference between genuine audit defense (a written guarantee with active representation) and vague promises of "support." A key question is whether the provider will represent the taxpayer before the IRS if the study is examined.

The strength of the original report documentation is your best protection. A study that includes all 13 ATG elements greatly expedites the IRS's review and minimizes the audit burden.

Years of Experience and Track Record

Cost segregation studies can be reviewed by the IRS years after filing. A provider that has only been in business two or three years may not be around when that happens. Longevity is a practical requirement, not just a prestige signal.

Concrete performance indicators include:

- Number of completed studies

- Average first-year deductions achieved

- Client referral rates

- Years in business

These are concrete performance indicators, not vague claims of "experience." Providers with 10+ years in business and thousands of completed studies demonstrate staying power and expertise.

Turnaround Time and Delivery Process

Top firms deliver studies within 2 to 4 weeks of receiving necessary documents — and should commit to that timeline in writing at the proposal stage. Cost segregation results must be reflected in your tax return by the applicable filing deadline, so delays can cost you a full year of deductions.

Watch for both extremes:

- Promises of immediate turnaround: suggests desktop shortcuts, not engineering rigor

- Timelines stretching into months: indicates capacity problems or inefficient processes

Client Reviews, References, and Transparency

Client testimonials and third-party review scores reveal what working with a provider actually looks like: professionalism, thoroughness, and whether projected savings matched delivered results.

Verified review platforms and references from clients with similar property types provide the clearest picture of actual performance. A multifamily investor's experience may differ significantly from a hotel owner's. A firm that cannot provide references or has no traceable reviews should be treated with caution.

Red Flags to Watch Out For When Evaluating Providers

Certain warning signs should immediately disqualify a cost segregation provider from consideration. Watch for these three in particular:

- Inflated savings projections designed to win the engagement

- Outsourced engineering work passed off as in-house expertise

- Contingency-based pricing that violates professional standards

| Red Flag | What It Signals |

|---|---|

| Inflated savings projections | Final report underdelivers; no recourse |

| Outsourced engineering work | Delays, weakened quality control, accountability gaps |

| Contingency-based pricing | Incentive to over-classify assets; violates ASCSP Rule 2.12, Treasury Circular 230, AICPA Code of Professional Conduct |

Inflated Projected Savings

Some providers use inflated savings estimates on proposals to win the engagement. They lowball their methodology but overbid the benefits, and the final report underdelivers — leaving you with less than promised and no recourse.

Outsourced Engineering Work

Firms that send engineering work to third-party subcontractors, rather than keeping it in-house, create real liability. Outsourcing causes delays, weakens quality control, and creates accountability gaps if the study is ever audited. You're paying for the firm's expertise, not a marked-up version of someone else's work.

Contingency-Based Pricing

Contingency-based fees, where the provider charges a percentage of identified tax savings, violate professional standards. The ASCSP Code of Ethics Rule 2.12 explicitly prohibits members from accepting fees on a contingent basis for federal income tax depreciation services. Treasury Circular 230 and the AICPA Code of Professional Conduct take the same position.

This fee structure creates a direct incentive to over-classify assets, which compromises IRS compliance and exposes you to penalties. Firms that propose contingency-based pricing operate in direct violation of these professional standards.

Questions to Ask Before You Hire a Cost Segregation Provider

Before signing an agreement, the following essential questions provide a framework for evaluating any provider:

| # | Question | What to Evaluate |

|---|---|---|

| 1 | What is your specific methodology for this property type, and do you conduct on-site inspections? | Engineering analysis, blueprint review, physical or virtual site visits |

| 2 | What credentials and certifications do the professionals performing the study hold? | CCSP designations, licensed professional engineers, ASCSP membership |

| 3 | What is your process if this study is questioned by the IRS, and is audit support included in the fee? | Active representation, documentation supplied, written defense commitment |

| 4 | Can you provide a sample report or example deliverable? | Methodology clarity, documentation depth, CPA usability |

| 5 | Do you have experience with my specific property type? | Multifamily, short-term rentals, commercial mixed-use specialization |

1. What is your specific methodology for this property type, and do you conduct on-site inspections?

A qualified provider gives details about engineering analysis, blueprint review, and physical or virtual site visits. Providers that reference "desktop studies" or "estimation models" warrant close scrutiny regarding documentation and IRS defensibility.

2. What credentials and certifications do the professionals performing the study hold?

CCSP designations, licensed professional engineers, and ASCSP membership are meaningful credentials. Years of direct cost segregation experience and number of completed studies are concrete performance indicators.

3. What is your process if this study is questioned by the IRS, and is audit support included in the fee?

The provider should explain their audit defense policy clearly: whether they provide active representation, what documentation they'll supply, and whether additional fees apply. A written audit defense commitment or money-back guarantee signals genuine confidence in the work.

4. Can you provide a sample report or example deliverable?

A redacted sample report reveals methodology clarity, documentation depth, and how usable the deliverable will be for your CPA. If a firm won't show its work, that's a major red flag.

5. Do you have experience with my specific property type?

A firm experienced in multifamily may not know the nuances of short-term rentals or commercial mixed-use. Different property types carry different depreciation opportunities, and that specialized knowledge directly affects your results.

Why Seneca Cost Segregation Stands Out

Seneca Cost Segregation is a veteran-owned firm with over 12 years of experience and more than 10,200 completed studies nationwide. Founded by real estate investors who have personally used cost segregation to grow their portfolios, the team understands what matters to property owners, not just accountants.

Co-founder Paul Spies, a Marine Corps Sergeant with over 8 years of real estate construction expertise, successfully flipped over 150 homes in 4 years and led ground-up multifamily projects. Having used cost segregation since 2018, Paul and co-founder Dylan Scandalios started Seneca to bring the same competitive edge they benefited from to investors at an affordable price with on-time delivery.

That investor-first foundation is backed by rigorous engineering credentials:

| Credential / Capability | Detail |

|---|---|

| ASCSP membership | CCSP designation |

| Engineering staff | Licensed professional engineers on staff |

| Technology | Proprietary in-house technology built and tested for compliance |

| Turnaround time | Studies delivered within 2 to 4 weeks |

| Engineering analysis | All engineering analysis performed in-house (no outsourcing) |

The firm's track record reflects those standards in concrete terms:

| Performance Metric | Result |

|---|---|

| Average first-year deduction | $171,243 |

| Client referral rate | 95% |

| Audit defense | AuditDefense program with money-back guarantee |

| Total property costs analyzed | Over $5 billion |

Seneca serves all 50 states and pairs every study with a complimentary tax assessment to identify additional savings across your portfolio. The free assessment means individual investors get the same strategic analysis typically reserved for institutional clients, with no upfront cost to find out where you stand.

Frequently Asked Questions

How much should I pay for a cost segregation study?

Fees typically vary based on property type and complexity and are usually structured as flat fees. Contingency-based pricing, where a firm charges a percentage of your tax savings, is a red flag that violates professional standards. The quality and defensibility of the study matters more than the lowest price.

Who should I hire for a cost segregation study?

CCSP credentials, a sample report, and confirmation of in-house engineers rather than outsourced teams are key indicators of a qualified provider. Documented audit defense and a demonstrated track record of completed studies are equally important. Experience and transparency are the two fastest filters for weeding out unqualified providers.

What credentials should a cost segregation provider have?

CCSP designation from the ASCSP is the industry's leading credential, requiring 7,000 hours of experience over 7 years. Providers should also have licensed engineers on staff. CPAs or tax preparers without engineering expertise are not sufficient on their own.

What is the difference between an engineering-based and a desktop cost segregation study?

Engineering-based studies involve physical site inspections, blueprint review, and detailed asset tagging. Desktop studies rely on cost estimation models without field verification. The engineering approach produces more comprehensive and defensible deductions that align with IRS standards.

Can a cost segregation study be done on a property I've already owned for several years?

Yes, a lookback study (also called a catch-up study) can be performed on properties owned for multiple years. Using Form 3115 and a Section 481(a) adjustment, you can claim all previously missed accelerated depreciation in a single year without amending prior returns.

Does a cost segregation study increase the risk of an IRS audit?

The IRS explicitly recognizes cost segregation as a legitimate tax strategy. The risk comes from poorly documented or over-aggressive studies, not the approach itself. According to the 2024 IRS Data Book, individual audit rates remain at 0.40%. A high-quality engineering-based report with proper workpapers is your best defense.