Introduction

Physicians consistently earn incomes that place them in the 32–37% federal tax brackets—the highest marginal rates in the U.S. tax code. In 2025, married physicians filing jointly enter the 32% bracket at $394,601 and the 37% bracket at $751,601, and compensation data shows that many specialties far exceed these thresholds—Neurosurgery averages $763,908, Orthopaedic Surgery $654,815, Cardiology $565,485, and Anesthesiology $494,522.

Unlike business owners who can deduct dozens of operating expenses, W-2 physicians have very few tools to legally reduce taxable income. Real estate depreciation is one of the most powerful exceptions — and for doctors earning $400K–$750K+, the dollar impact is substantial.

This article breaks down how depreciation actually works for physicians at those income levels: the specific deductions available, how cost segregation accelerates them, and what the compounding effect looks like over a 5–10 year investment horizon.

TL;DR

- Real estate depreciation creates a non-cash IRS deduction that reduces taxable income each year—even when a property generates positive cash flow

- Residential rental properties depreciate over 27.5 years; commercial over 39—with no additional spending required

- Cost segregation accelerates deductions into year one, front-loading years of deductions for high-bracket physicians

- Skipping a cost segregation study means leaving tens of thousands in annual deductions unclaimed

- Without recapture planning, depreciation savings can reverse into unexpected tax bills when you sell

What Is Real Estate Depreciation?

Real estate depreciation is an IRS-approved deduction that assumes a property's physical structure loses value over time due to wear and tear. Each year, you can deduct a portion of the building's value as a "paper loss" — regardless of what the property is actually worth on the market.

Where It Applies:

- Residential rental properties: 27.5-year depreciation schedule

- Commercial properties: 39-year depreciation schedule

- Land: Never depreciable, as only structures and qualifying components count

For physicians generating cash flow from real estate, this matters more than most people realize. Rental income can appear as a loss on paper through depreciation — directly cutting the amount of that income subject to tax, sometimes to zero.

Key Tax Advantages of Real Estate Depreciation for Physicians

The advantages below aren't abstract—each maps directly to your tax return, net income, and ability to reinvest faster. The value compounds over time, especially for those in the highest marginal brackets.

Advantage 1: Taxable Income Reduction Without Spending a Dollar

Depreciation creates a "phantom expense": you deduct thousands of dollars each year without any actual cash leaving your pocket. This directly reduces the rental income subject to tax.

Take a physician who owns a residential rental property with a $400,000 depreciable basis (excluding land). Using the 27.5-year straight-line schedule:

- Annual depreciation: $400,000 ÷ 27.5 = $14,545

- Tax savings at 37%: $14,545 × 37% = $5,382 in federal tax savings every year

Why This Matters for Physicians Specifically:

High-income physicians save far more per dollar of deduction than lower-bracket earners. Many physician specialties fall squarely into the 32–37% federal brackets, meaning every $10,000 in depreciation deductions saves $3,200 to $3,700 in federal taxes alone—before state taxes.

This advantage hits hardest during peak clinical earning years. Offsetting even a portion of passive income with non-cash depreciation keeps more dollars available to reinvest, rather than sending them to the IRS now.

Advantage 2: Accelerated Deductions Through Cost Segregation

A cost segregation study breaks a property down beyond just "building and land." It identifies components like flooring, cabinetry, appliances, electrical systems, and land improvements that qualify for 5-, 7-, or 15-year depreciation schedules instead of 27.5 or 39 years, dramatically front-loading deductions.

How This Works in Practice:

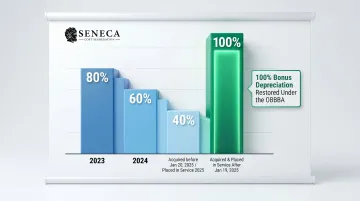

After a cost segregation study, bonus depreciation (under current rules) allows physicians to deduct a significant portion of those shorter-life components in year one. The One Big Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation for property acquired and placed in service after January 19, 2025.

Bonus Depreciation Phase-Out Schedule:

| Acquisition & Placed-in-Service Date | Bonus Depreciation % |

|---|---|

| 2023 | 80% |

| 2024 | 60% |

| Acquired before Jan 20, 2025 (Placed in service 2025) | 40% |

| Acquired & Placed in Service AFTER Jan 19, 2025 | 100% |

Why This Creates Outsized First-Year Impact:

A physician buying a $1–2M rental property can often claim $100,000–$200,000 in first-year deductions through cost segregation and bonus depreciation, offsetting a substantial portion of clinical income or passive gains. Seneca Cost Segregation's engineering team, which has completed over 10,200 studies nationwide, reports an average first-year deduction of $171,243 per client.

A professional cost segregation study from a CCSP-certified firm is required to identify and document qualifying components in an IRS-compliant, audit-defensible way. Seneca's engineers follow the IRS Cost Segregation Audit Techniques Guide precisely, ensuring documentation that holds up under scrutiny.

The downstream effects show up across several metrics:

- First-year tax savings and effective tax rate on rental income

- Year-one cash-on-cash return after tax benefit

- Time to reinvest into the next property

When It Matters Most:

Most impactful immediately after acquisition, during major renovations, or when purchasing properties where a high percentage of value is in shorter-life personal property components—such as furnished short-term rentals or medical office buildings with significant equipment and fixtures.

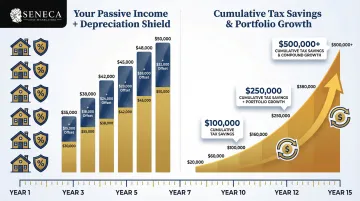

Advantage 3: Sheltering Passive Income and Compounding Wealth Faster

Depreciation losses from real estate can directly shelter passive income, including distributions from syndications, rental cash flow, and K-1 income from real estate funds, reducing or eliminating the tax owed on those dollars each year.

Carry-Forward Mechanism:

If depreciation losses exceed passive income in a given year, the unused losses aren't wasted. They're "suspended" and carry forward to offset future passive income—or are released in full when the property is eventually sold, reducing the taxable gain at exit.

Why This Compounds for Physicians:

A physician earning $400K in W-2 clinical income who also receives $30–50K in passive real estate distributions can potentially owe $0 in tax on those distributions when depreciation losses are applied. That effectively increases the real after-tax yield of the investment without changing the property itself.

For physicians building a passive portfolio over 5–15 years, this effect compounds. Accumulated depreciation losses systematically shelter a growing income stream, accelerating the path to financial independence without requiring active day-to-day involvement in the properties.

What Happens When Physicians Ignore Real Estate Depreciation

The Opportunity Cost in Concrete Terms

A physician who owns rental property but doesn't properly claim depreciation—or has never had a cost segregation study done—is overpaying taxes on passive income every single year.

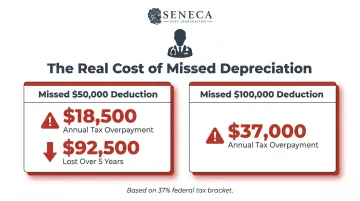

Consider a physician in the 37% bracket who misses a $50,000 annual depreciation deduction:

- Tax overpayment: $50,000 × 37% = $18,500 per year

- Over 5 years: $92,500 in unnecessary taxes paid

Missing a $100,000 deduction costs $37,000 annually in overpaid federal taxes alone.

The Compounding Cost of Delay

Those annual losses don't exist in isolation — each year without a cost segregation study on a qualifying property is a year of front-loaded deductions permanently lost. The IRS allows "catch-up" depreciation through a cost segregation lookback study for properties already owned—but only if proactively requested using Form 3115. Physicians who wait years lose the first-year bonus depreciation advantage entirely.

Plan for Depreciation Recapture Before It Plans for You

Physicians who claim depreciation without accounting for an eventual sale can face a significant tax bill at closing. Depreciation recapture is taxed at up to 25% on amounts previously deducted — a hit that catches many off guard. Strategies like 1031 exchanges and long-term holds can manage this exposure, but they need to be part of the investment plan from the start.

How Physicians Get the Most Value from Real Estate Depreciation

Work with a Real Estate-Focused CPA

A CPA who specializes in real estate investing—not a generalist—ensures depreciation is claimed correctly every year, all qualifying deductions are captured, and the property's depreciation schedule reflects its actual component values.

When to Commission a Cost Segregation Study

Cost segregation typically becomes cost-effective for properties with a building basis of $500,000 or more. Studies generally take 2–4 weeks to complete from engagement to delivery. Seneca Cost Segregation offers complimentary preliminary assessments to estimate potential tax savings before commissioning a full study.

Real Estate Professional Status (REPS)

Depreciation benefits are deferred, not eliminated. At sale, recapture is taxed at up to 25%. The right exit strategy determines how much of that tax you actually pay. Options include:

- 1031 exchanges: Roll proceeds into a new property, deferring recapture

- Estate step-up in basis: Inherited property's basis is stepped up to fair market value at death, eliminating accumulated depreciation recapture for heirs

- Long-term holds: Defer recapture indefinitely while cash flow compounds

For physicians in the 37% bracket, each of these strategies can mean the difference between keeping or surrendering a substantial portion of accumulated depreciation savings — making recapture planning as important as the depreciation strategy itself.

Conclusion

Real estate depreciation is a built-in IRS mechanism that rewards property ownership — and for physicians in the highest tax brackets, it's one of the most efficient legal tools available to reduce taxable income and grow wealth simultaneously.

The advantages are cumulative and strategic:

- Straight-line depreciation reduces taxes every year

- Cost segregation front-loads those savings for maximum early impact

- Passive income sheltering compounds the benefit across an entire investment portfolio

Each strategy strengthens the others — but only if they're actually being used. That's the conversation worth having with your CPA.

Physicians who already own real estate should ask:

- Is every qualifying depreciation deduction being captured?

- Has a cost segregation study been completed on this property?

- Are passive losses being applied against the right income streams?

Every year without these strategies in place is a year of deductions you can't recover.

Frequently Asked Questions

Can a doctor be a real estate professional?

A doctor can technically qualify for Real Estate Professional Status (REPS), but it's extremely difficult as a full-time physician—the IRS requires more than 750 hours per year in qualifying real estate activities AND real estate must represent more than 50% of all professional time. A non-physician spouse filing jointly who meets these criteria is the most realistic path for most physician households.

What can a doctor write off on taxes related to real estate?

Physician-owners can deduct depreciation (straight-line and accelerated), mortgage interest, property taxes, repairs and maintenance, property management fees, and insurance. Depreciation is typically the most valuable because it's a non-cash deduction — it reduces taxable income without requiring additional spending.

What qualifies for accelerated depreciation?

Components identified through a cost segregation study as having shorter useful lives—such as carpeting, cabinetry, appliances, specialty electrical, parking lots, and landscaping—qualify for 5-, 7-, or 15-year depreciation schedules. These may also qualify for bonus depreciation, allowing a portion or all of their value to be deducted in the first year of ownership.

How does cost segregation work for physician-owned properties?

A cost segregation study is an engineering-based analysis that breaks a property into its component parts and assigns each a depreciation life per IRS guidelines. The result: physician-owners front-load deductions instead of spreading them across 27.5 or 39 years, generating larger write-offs precisely when income and tax brackets are highest.

Do passive rental losses from depreciation offset a physician's W-2 income?

In most cases, passive rental losses (including depreciation) can only offset other passive income—not W-2 or 1099 clinical income—unless the physician or their spouse qualifies as a real estate professional under REPS. Unused losses are "suspended" and carried forward to offset future passive income or capital gains when the property is sold.

What is depreciation recapture and how should physicians plan for it?

Depreciation recapture is the IRS's mechanism to tax previously claimed depreciation deductions when a property is sold, at a rate of up to 25%. Physicians can defer or minimize this through 1031 exchanges, long-term holds, or estate strategies like the step-up in basis at death. Early planning with a real estate-focused CPA is essential.