Introduction

Property taxes are climbing faster than home values across the United States. According to ATTOM's 2025 Property Tax Analysis, average single-family home tax bills jumped 3% to $4,427, pushing the national effective rate to 0.9%—even as average home values dropped 1.7%. That gap points to something most homeowners miss: rising tax bills aren't always tied to rising values. Municipal millage rate increases and compounding valuation errors quietly inflate assessments year after year.

Property taxes are not fixed expenses. They're recalculated annually (or on multi-year cycles) based on two variables: your property's assessed value and the local tax rate. Both can be influenced, contested, or reduced through deliberate action.

This article covers three dimensions of effective property tax reduction: pre-assessment decisions, management during the assessment process, and broader strategies including exemptions, appeals, and — for real estate investors — income tax tools like cost segregation that complement property tax savings.

TL;DR

- Property taxes multiply your assessed value by the local mill rate—address both sides to cut costs

- Over 56% of property tax appeals result in reductions, and filing fees are minimal in most jurisdictions

- Exemptions for primary residences, seniors, veterans, and disabled homeowners can reduce taxable value directly

- Assessment errors (incorrect square footage, phantom improvements) are common and legally must be corrected

- Real estate investors can combine property tax strategies with tools like cost segregation for compounded tax savings

How Property Tax Bills Build Up — and What Keeps Driving Them Higher

Property taxes are a recalculated obligation tied to two moving parts: the local millage rate (tax rate) set by your municipality and the assessed value assigned to your property by the county assessor. The formula is straightforward:

Property Tax = Assessed Value × Mill Rate ÷ 1,000

For example, a home assessed at $300,000 in a jurisdiction with a 25-mill rate would generate a $7,500 annual property tax bill ($300,000 × 0.025 = $7,500).

Three triggers cause property tax bills to increase:

- Rising assessed value — Formal reassessment cycles, neighborhood appreciation, or recorded improvements (pools, decks, additions) push your assessed value higher

- Millage rate hikes — Municipalities raise tax rates to fund schools, infrastructure, or public services, generating more revenue from the same tax base

- Special assessments — One-time levies for specific public improvements like new sidewalks, streetlights, or sewer systems

Reassessment cycles vary dramatically by state. Some reassess annually (Arizona, Georgia, Michigan), while others operate on 3-5 year cycles (Alabama, Connecticut, Florida, Tennessee). In states with infrequent reassessments, valuation errors or outdated property data can go undetected for years before homeowners notice.

A 2025 Cook County audit revealed $444 million in missed new construction value, leading to sudden back-tax bills exceeding $23,000 for individual homeowners when the county finally corrected its records.

Strategies That Reduce Property Taxes by Changing Your Decisions

The most effective cost-reduction strategies happen before the assessor ever visits your property. Smart timing around construction, improvements, and reassessment cycles can keep your assessed value lower for years.

Know your local reassessment schedule

Find out when your jurisdiction conducts reassessments and plan visible property changes around that calendar. Improvements completed just before a reassessment cycle will be captured in the next assessment. If your county reassesses every four years and you're two years into the cycle, delaying major additions by 12-18 months could keep your current assessed value frozen for several more years.

Avoid structural additions before scheduled assessments

California Board of Equalization guidelines confirm that adding pools, decks, sheds, or garage expansions triggers partial reassessments, while replacing a roof or updating kitchen counters qualifies as non-assessable routine maintenance. If you're planning a $40,000 pool addition, completing it immediately after a reassessment (rather than immediately before) can defer the tax impact for the entire reassessment cycle—potentially saving thousands.

Before breaking ground on any addition:

- Contact your local building and tax department to estimate the tax impact

- Research comparable properties to see how similar improvements affected their assessed values

- Consider whether cosmetic upgrades (new paint, landscaping, updated fixtures) might deliver similar satisfaction without triggering reassessment

Be strategic about curb appeal ahead of assessor visits

Assessors factor visible property condition into their valuations. Completing major exterior improvements—new siding, landscaping overhauls, fresh paint—in the weeks before a scheduled evaluation can push your assessed value above comparable neighbors. Time those projects for after the assessment window closes, not before it opens.

Audit your property tax card before making improvements

Review your property tax card to understand your current assessed baseline and verify the details on file: square footage, bedroom count, fixtures, lot size, and improvement history. Correcting discrepancies before making new improvements ensures you're not compounding errors that already inflate your assessment.

Strategies That Reduce Property Taxes by Managing the Assessment Process

Once an assessment is underway or a bill has been issued, several management-level actions can directly influence the outcome. The assessor's evaluation isn't final until it's finalized, and engaged homeowners consistently achieve fairer valuations.

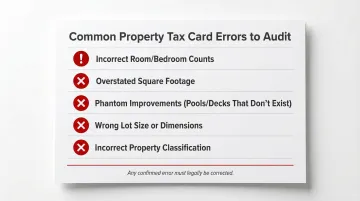

Request and Audit Your Property Tax Card

Property tax cards (also called field cards or property record cards) are public documents maintained by the assessor that list your property's characteristics. Request a copy from your local assessor's office and audit it for errors:

- Incorrect room counts or bedroom counts

- Overstated square footage

- Phantom improvements (pools, decks, or additions that don't exist)

- Wrong lot size or property dimensions

- Incorrect property classification

Any confirmed error must legally be corrected and will reduce your assessed value. These errors are more common than most homeowners realize, so review your card as soon as possible.

Compare Your Assessment to Neighboring Properties

Pull the tax cards of comparable properties in your neighborhood using public records (most assessor websites offer free online access). If a neighboring home with more square footage, more bedrooms, or better amenities is assessed lower than yours, you have grounds to raise a discrepancy with the assessor's office.

Document the differences with photos and property details before contacting the assessor. The stronger your evidence, the harder the discrepancy is to dismiss.

Allow Assessor Access and Guide the Visit

Municipalities that receive no property access often default to assigning the maximum assessed value for that property type. Granting access and actively guiding the assessor through your home ensures deficiencies are documented rather than overlooked:

- Point out aging HVAC systems and outdated fixtures

- Highlight visible cracks, water damage, or structural wear

- Note the lack of garage, finished basement, or other value-add features

- Show deferred maintenance items like worn flooring or outdated appliances

In most states, you can legally deny interior access and still challenge your assessment — but doing so forces assessors to rely on less accurate data, which often results in overvaluation. Check your state's specific rules before deciding.

Strategies That Reduce Property Taxes by Changing the Context Around Your Property

Disputing your assessed value is one path to a lower tax bill. But the more reliable approach often involves changing the legal and administrative context around the property entirely — through exemptions, formal appeals, and for investors, coordinating property tax strategy with federal income tax planning.

Research and apply for every applicable exemption

Common exemption programs include:

- Homestead exemption — Reduces assessed value for primary residences (Texas mandates a $140,000 school tax exemption; Florida offers up to $50,000)

- Senior citizen exemptions — Typically for homeowners age 65+ (income thresholds vary by state)

- Veteran and service-connected disability exemptions — Texas provides 100% exemption for veterans awarded 100% disability compensation

- Agricultural use exemptions — Special appraisal valuing land based on agricultural productivity, not market value

- Low-income relief programs — Circuit breaker programs like Maryland's Homeowners' Property Tax Credit cap taxes based on income

Most programs require a formal application and have annual or one-time filing deadlines (often in January). Missing the deadline means waiting another year. Despite their value, circuit breakers and exemptions suffer from underutilization—many eligible households fail to claim available relief.

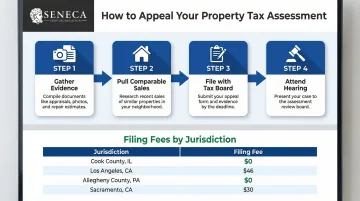

File a formal appeal when assessment appears inflated

If your assessed value appears genuinely inflated compared to recent comparable sales or an independent appraisal, file a formal appeal with your local tax board. Over 56% of property tax appeals in Cook County result in a reduction, while initial filing fees remain low or free across major jurisdictions:

- Cook County, IL: $0 for homeowners

- Los Angeles County, CA: $46

- Allegheny County, PA: $0

- Sacramento County, CA: $30

Document your case with:

- Photos illustrating current property condition

- Recent sale prices of 3-6 comparable properties

- Independent appraisal report (if available)

- List of deficiencies or deferred maintenance

A successful appeal permanently lowers your base assessed value (in most jurisdictions), generating ongoing savings for years. However, California's Proposition 8 grants temporary decline-in-value reductions that assessors must review annually—as markets recover, these values can increase rapidly back to the factored Prop 13 base year value.

Coordinate property tax management with income tax strategies

For real estate investors, property taxes are one piece of a larger tax burden — one that also includes income taxes on rental income, depreciation recapture, and capital gains. Reducing your assessed value helps at the local level, but the federal side often holds the bigger opportunity.

Cost segregation reclassifies 20-40% of a property's cost into accelerated depreciation categories — 5, 7, and 15-year schedules instead of 39 years. That acceleration often generates six-figure deductions in year one. Seneca Cost Segregation has completed over 10,200 engineering-based studies nationwide, helping investors achieve an average first-year deduction of $171,243.

Layered tax optimization combines:

- Property tax appeals and exemptions — reduce assessed value at the local level

- Cost segregation — accelerate federal depreciation deductions

- Bonus depreciation — maximize immediate write-offs on qualifying assets

Used together, these tools address your tax burden at every level — not just the assessed value on a single assessment notice.

Time property acquisitions relative to reassessment calendars

In jurisdictions where an Assessable Transfer of Interest triggers a reassessment, a purchase just before a cycle could result in an immediate jump in assessed value. California's Proposition 13 requires reassessment to current market value upon change in ownership. Michigan's taxable value "uncaps" in the calendar year following transfer. South Carolina applies the new market value for the year following the transfer.

Understanding this timing allows buyers to:

- Plan for the tax impact in year-one cash flow projections

- Explore partial exemptions available for newly acquired properties

- Never rely on the seller's current tax bill to estimate future liabilities

Conclusion

Lowering property taxes isn't about generically cutting spending—it requires identifying exactly where the overcharge originates. The source matters. Common culprits include:

- An error in the tax record (wrong square footage, incorrect property class)

- An assessor's subjective overvaluation unsupported by comparable sales

- An unclaimed exemption you qualify for but never applied

- A missed appeal window that reset your options for another year

Each of these requires a different fix. The right strategy depends entirely on which one is driving your excess cost.

For real estate investors, the most effective approach is layered. Property tax management targets the assessed value at the local level. Cost segregation, by contrast, accelerates depreciation deductions at the federal level — often generating six-figure first-year savings on qualifying properties.

Used together, these strategies reduce tax exposure from two directions simultaneously, freeing up capital that would otherwise sit with the IRS and putting it back into your next acquisition.

Frequently Asked Questions

How can I lower my property taxes?

Audit your property tax card for errors (incorrect square footage, phantom improvements), compare your assessment to neighboring properties, and apply for applicable exemptions (homestead, senior, veteran). If your assessed value exceeds recent comparable sales, file a formal appeal with documented evidence — most jurisdictions charge nothing to file.

Who qualifies for property tax relief in New Jersey?

New Jersey's Senior Freeze (Property Tax Reimbursement) reimburses eligible seniors (65+) and disabled persons for property tax increases, with 2025 income limits of $172,475. The ANCHOR Program offers relief to homeowners and renters. Both programs use the combined PAS-1 application, with the 2025 application deadline of November 2, 2026.

What property tax relief is available in Tennessee?

Tennessee offers a state-funded Property Tax Relief program for low-income elderly (65+), disabled homeowners, and disabled veterans. For 2025, the maximum income limit is $37,530 (based on 2024 income). Applications must be filed within 35 days after the delinquency date and are processed through the county trustee's office.

Who qualifies for property tax exemption in Michigan?

Michigan's Principal Residence Exemption (PRE) exempts primary residences from the local school operating millage (up to 18 mills) — file Form 2368 to claim it. Low-income homeowners who cannot afford their tax burden may also qualify for the Poverty Exemption (MCL 211.7u) by filing Form 5737 annually with the local Board of Review.

How can I lower property taxes in Minnesota?

Minnesota's Homestead classification lowers the effective tax rate on primary residences (apply by December 31 to your county assessor), and the Property Tax Refund (M1PR) offers refunds for households earning below $142,490 in 2025. You can also challenge your assessed value through the Local Board of Appeal and Equalization, the County Board, or Minnesota Tax Court.

Who qualifies for senior property tax exemptions in Alabama?

Alabama residents 65+ are automatically exempt from the state-levied portion of property taxes with no income limit. Seniors with net annual taxable income of $12,000 or less qualify for a full exemption — covering all state, county, and municipal taxes on their primary residence and up to 160 adjacent acres.