While rental properties can deliver steady cash flow, equity growth, and substantial tax advantages, the actual experience depends heavily on preparation, property selection, and financial strategy. Too many first-time investors underestimate the time commitment, overestimate returns, and miss critical tax optimization opportunities that separate profitable portfolios from break-even headaches.

This guide cuts through the hype to answer three core questions: How passive is rental income really? What returns can you realistically expect? And what strategies, including advanced tax planning, can make a meaningful difference?

TLDR

- Rental income is IRS-classified as passive, yet landlords average 4 hours/month per unit in routine operations, plus 47.5 hours per vacancy turnover

- Realistic cash-on-cash returns currently range from 5.5% to 8% for single-family rentals, down from historic highs

- Vacancy loss, maintenance reserves, property management fees, and insurance surges erode profits by 20–30% annually

- True passivity requires paying professionals, a tradeoff that preserves time but reduces net cash flow

- Cost segregation studies accelerate depreciation deductions, often generating $40,000 to $171,000+ in first-year tax savings

Is Rental Property Income Truly "Passive"? The Honest Answer

Passive income means money earned with minimal ongoing effort. The IRS classifies rental income as a passive activity under IRC §469, meaning losses typically offset only other passive income, not your W-2 salary or business income. But the IRS label and the lived reality diverge sharply.

Self-managing landlords spend roughly 4 hours per month per unit on routine operations: tenant communication, maintenance coordination, lease renewals, accounting, and compliance with local landlord-tenant laws. None of this feels passive when you're fielding emergency repair calls at midnight.

The time commitment spikes sharply during turnover. Landlords average 47.5 hours per vacancy on leasing, tenant screening, and property preparation. Annual turnover means committing nearly 96 hours (over two full work weeks) to a single "passive" investment.

The key variable determining how passive it feels: self-management versus hiring a property manager.

Investors who self-manage trade time for money. Those who hire property managers trade money for time. Neither approach makes rental income effort-free; it shifts where the effort goes. Property managers handle the operational load, but at a cost:

- Tenant screening, rent collection, and maintenance coordination

- Legal compliance and lease enforcement

- Monthly management fees of 8–12% of collected rent

- Leasing fees equal to 50–100% of one month's rent per turnover

The Real Estate Professional Exception

For high-income earners planning tax strategy, the IRS draws a meaningful line. To break out of passive classification, investors must qualify as Real Estate Professionals under IRS rules:

- More than 750 hours annually spent in real property trades or businesses

- Representing more than 50% of total working time

Meet these tests, and rental losses become non-passive; they can fully offset active W-2 or business income.

Investors who don't hit that 750-hour mark still have an option: the "active participation" exception. Owners who make significant management decisions (approving tenants, setting rental terms, authorizing expenditures) can deduct up to $25,000 of passive rental losses against non-passive income.

That deduction phases out completely for Modified Adjusted Gross Incomes between $100,000 and $150,000, meaning high-earning professionals lose it entirely.

In practice: Rental property sits on a spectrum from "semi-passive" to "genuinely passive" depending on how you structure ownership, management, and financial systems. How you structure the tax side of that equation (depreciation strategy, passive loss classification, cost recovery timing) often determines whether the investment performs or just breaks even.

What to Realistically Expect in Year 1 (and Beyond)

Current Market Returns: The Era of Single-Digit Yields

The era of double-digit cash-on-cash returns on turnkey properties has ended. In 2025-2026, single-family rentals are seeing cash flow yields tighten, with average returns hovering between 5.5% and 8%. To achieve the upper tier, investors increasingly turn to value-add small multifamily properties (2-4 units), currently yielding 8% to 11%.

Cap rates have stabilized after intense volatility. For small multifamily assets, cap rates averaged 6.0% in early 2025, while broader multifamily cap rates sat between 5.6% and 5.7%.

Key metrics for evaluating rental properties:

| Metric | Formula | Notes |

|---|---|---|

| Cash-on-cash return | Annual pre-tax cash flow divided by total cash invested (down payment plus closing costs and initial repairs) | — |

| Cap rate | Net Operating Income divided by purchase price | Useful for comparing markets and property types |

| Gross Rent Multiplier (GRM) | Purchase price divided by annual gross rent | Lower is better for cash-flow investors |

The Death of the 1% Rule

The "1% rule" (where monthly rent equals 1% of the purchase price) and the stricter "2% rule" were once gold standards for quickly screening rental properties. Today, these rules are virtually extinct in major markets. Record-high national median sales prices have severely compressed rental yields.

Nationally, the price-to-rent ratio sits at 14.3, meaning the average home price has increased 39% faster than the average rent price over the past five years.

Finding a property that meets the 1% rule in a stable, appreciating neighborhood is highly unlikely. Properties that do hit the 1% or 2% mark are typically older homes in weaker, distressed areas that require heavy repairs and suffer from high tenant turnover.

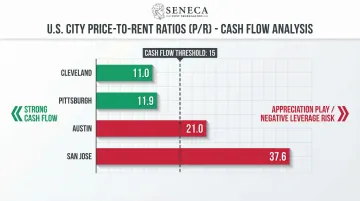

Alternative measures: Price-to-rent ratios and market-specific analysis. A price-to-rent ratio of 15 or less indicates a market where buying is relatively affordable compared to rent, making it favorable for cash-flow investors.

| City | Price-to-Rent Ratio | Market Characteristic |

|---|---|---|

| Cleveland | 11.0 | Strong cash flow potential |

| Pittsburgh | 11.9 | Strong cash flow potential |

| Austin | 21.0 | Pure appreciation play, negative leverage risk |

| San Jose | 37.6 | Pure appreciation play, negative leverage risk |

Long-Term Wealth Building: The 5-10 Year Picture

Year 1 cash flow is often modest or break-even, but rental income improves steadily as rents rise and fixed-rate mortgage payments stay flat. After the historic rent surges of 2021-2022, the market has cooled. Zillow forecasts single-family rents will rise by 1.8% in 2026, while multifamily rents will remain essentially flat at 0.6% growth due to historic construction booms and elevated vacancies.

Even with slower rent growth, equity builds on two fronts simultaneously:

- Mortgage amortization: As the loan progresses, more of each tenant-funded payment applies to principal, accelerating equity build-up in later years

- Rent growth outpacing fixed costs: A mortgage locked at today's rate costs the same in year 10, but rents won't

- Forced savings: Each month, your tenant is paying down your debt, regardless of market conditions

The $1,000/Month Passive Income Milestone

How many properties do you need to generate $1,000 per month in passive income? The answer depends entirely on net cash flow per property after all expenses.

Realistic scenario:

| Item | Amount | Frequency |

|---|---|---|

| Purchase price | $350,000 | One-time |

| Down payment (25%) | $87,500 | One-time |

| Monthly mortgage (6.5%, 30-year) | $1,660 | Monthly |

| Property taxes | $350 | Monthly |

| Insurance | $150 | Monthly |

| Property management (10%) | $180 | Monthly |

| Maintenance reserve (8%) | $144 | Monthly |

| Vacancy allowance (7%) | $126 | Monthly |

| Total monthly expenses | $2,610 | Monthly |

If monthly rent is $1,800, your net cash flow is negative $810. This property loses money monthly but may still build wealth through appreciation and equity build-up.

To achieve $1,000 monthly passive income in today's market typically requires:

| Requirement | Detail |

|---|---|

| Number of properties | 3–5 in strong cash-flow markets (Midwest, secondary Sunbelt cities) |

| Net cash flow per property | $200–$350 per month after all expenses |

| Portfolio building timeline | 5–7 years for most investors starting with one property |

The Hidden Costs That Quietly Drain Your Returns

Vacancy Loss: The 7.2% Reality

Failing to underwrite for vacancy is a primary reason new investors experience negative cash flow. According to the U.S. Census Bureau, the national rental vacancy rate stood at 7.2% in Q4 2025. A 7.2% vacancy rate effectively means a property will sit empty for nearly one month out of the year.

Impact on a $2,000/month rental:

| Item | Annual Amount |

|---|---|

| Gross annual rent | $24,000 |

| Vacancy loss (7.2%) | -$1,728 |

| Effective gross income | $22,272 |

Investors must deduct at least 7-8% of gross scheduled rent from their pro forma to account for this reality. Vacancy, though, is only one side of the equation; the expense side carries its own landmines.

Capital Expenditure Reserves: The $200-$300/Unit Standard

Routine maintenance (fixing a leaky faucet) is entirely separate from Capital Expenditures such as replacing a roof, HVAC system, or water heater. Institutional lenders mandate strict CapEx reserves to ensure properties remain viable. Freddie Mac's Small Balance Loan guidelines require $200 to $300 per unit annually for replacement reserves.

For a 4-unit small multifamily property, this means holding $800 to $1,200 annually in a dedicated account just to cover the eventual degradation of major structural elements and systems. Skip this reserve, and a single $8,000 HVAC replacement wipes out years of cash flow.

Common CapEx items and typical lifespans:

| Item | Typical Lifespan | Replacement Cost |

|---|---|---|

| Roof | 20-25 years | $8,000-$15,000 |

| HVAC system | 15-20 years | $5,000-$10,000 |

| Water heater | 10-12 years | $1,200-$2,000 |

| Appliances | 10-15 years | $500-$1,500 each |

| Flooring | 7-10 years | $3,000-$8,000 |

Property Management Fees: What Passivity Actually Costs

Hiring a property manager buys back your time, and the bill is higher than most investors anticipate. The national average property management fee is 8.49% of collected monthly rent, with a practical range of 8% to 12% for most residential properties. However, the monthly percentage is only the baseline.

| Fee Type | Typical Range | When Charged |

|---|---|---|

| Monthly Management Fee | 8% – 12% of rent collected | Monthly, ongoing |

| Leasing / Tenant Placement Fee | 50% – 100% of one month's rent | When a new tenant is placed |

| Lease Renewal Fee | $150 – $300 flat fee | When an existing tenant renews |

| Maintenance Markup | 5% – 15% of repair cost | On each maintenance job coordinated |

When a unit turns over, the combination of vacancy loss, turnover repairs, and a 100% leasing fee can easily consume 20% to 30% of that year's gross rental income.

Rising Operating Costs: Insurance and Property Taxes

Operating expenses are rising faster than rents on two fronts. The average homeowners insurance premium rose by 11.2%, driven by supply-chain inflation and severe weather events. In 2023, the homeowners insurance industry posted a net combined ratio of 110.9, meaning insurers paid out more in claims and expenses than they collected in premiums. Further rate hikes for landlords are essentially locked in.

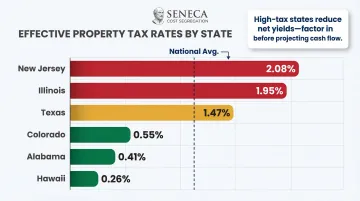

Property taxes compound the problem. Effective property tax rates range from 0.26% in Hawaii to 2.08% in New Jersey, and investors buying in high-tax states like Illinois (1.95%) or Texas (1.47%) must ensure their rental yields can absorb these annual liabilities before projecting cash flow.

How to Make Rental Income More Passive (and Keep More of It)

Step 1: Invest in Turnkey or Well-Maintained Properties

Buying a property that needs significant work before it can rent delays income and introduces project management demands. Paying a premium for a move-in-ready property in a high-demand area means income starts sooner and management burden stays lower.

What to look for:

- Recently updated kitchens and bathrooms

- New or recently serviced HVAC and water heater

- Solid roof with 10+ years remaining lifespan

- Quality flooring that can withstand tenant wear

- Neutral paint and finishes that appeal to broad tenant pool

Step 2: Hire a Vetted Property Manager from Day One

What a property manager handles:

- Tenant screening (credit checks, employment verification, rental history)

- Rent collection and late payment enforcement

- Maintenance coordination and vendor management

- Legal compliance (fair housing laws, local ordinances, eviction procedures)

- Lease renewals and tenant communication

Not all property managers are equal. When vetting candidates, prioritize:

| Criterion | Standard |

|---|---|

| Licensing | Licensed and insured in your state |

| Portfolio size | Manages at least 50-100 doors (lower per-unit costs benefit you) |

| Tenant retention | Average tenant retention rate above 70% |

| Fee structure | Transparent fee structure with no hidden charges |

| Technology | Technology platform for owner reporting and tenant communication |

| Vendor network | Strong local vendor network for cost-effective repairs |

The management fee is worth scrutinizing, but also worth paying. An 8–10% fee on a $2,000/month rental runs $160–$200. In return, you recover 4–6 hours of your time each month. If your earning potential exceeds $30–40/hour, the math favors delegation.

Step 3: Automate Financial Tracking and Rent Collection

Dedicated landlord software handles the administrative side of ownership so you're not chasing receipts or manually logging payments. Platforms like Stessa, Baselane, or Buildium automate:

- Rent collection with ACH transfers

- Expense categorization for tax reporting

- Document storage (leases, receipts, inspection reports)

- Owner and tenant portals for communication

Together, these three strategies (buying right, delegating management, and automating finances) compress the ongoing workload of rental ownership into something that genuinely runs in the background.

The Tax Angle: The Lever Most Landlords Overlook

Standard Tax Deductions Available to Rental Property Owners

Rental property owners can deduct:

- Mortgage interest

- Property taxes

- Insurance premiums

- Repairs and maintenance

- Property management fees

- Utilities (if landlord-paid)

- Legal and professional fees

- Travel to and from the property

- Depreciation

Depreciation, which the IRS allows residential properties to be depreciated over 27.5 years, can generate a significant paper loss that offsets rental income even when the property is cash-flow positive. This non-cash deduction is the single most powerful tax benefit of rental real estate.

Cost Segregation: Accelerating Depreciation for Massive First-Year Deductions

Under the IRS's Modified Accelerated Cost Recovery System (MACRS), residential rental property is depreciated using the straight-line method over 27.5 years. This provides a steady, predictable deduction, but it locks up the tax benefits of the building's purchase price for nearly three decades.

Cost segregation solves this by reclassifying specific assets within a property into shorter depreciation lifespans of 5, 7, or 15 years. A cost segregation study identifies eligible components such as carpet flooring, cabinetry, decorative moldings, landscaping, and fences, then pulls them out of the 27.5-year bucket. According to the American Society of Cost Segregation Professionals, a study can typically reclassify 20-40% of a residential property's total purchase price into these shorter categories, substantially increasing first-year depreciation expenses.

| Item | Without Cost Segregation | With Cost Segregation |

|---|---|---|

| Property purchase price | $500,000 | $500,000 |

| Land value (non-depreciable) | $100,000 | $100,000 |

| Depreciable basis | $400,000 | $400,000 |

| Reclassified to 5/7/15-year property | — | $120,000 (30%) |

| Remaining 27.5-year property | $400,000 | $280,000 |

| First-year depreciation | $14,545 (annual, 27.5 years) | $48,000 + $10,182 = $58,182 |

The difference: $43,637 in additional first-year deductions, which translates to over $15,000 in federal tax savings at a 35% tax rate.

Seneca Cost Segregation has helped investors achieve an average first-year deduction of $171,243. Their engineering-based studies identify qualifying building components and provide the detailed documentation required to withstand IRS scrutiny.

Navigating the 2025 Bonus Depreciation Phase-Down

The power of cost segregation is amplified by §168(k) bonus depreciation, which allows investors to immediately write off a percentage of reclassified 5-, 7-, and 15-year assets in the first year. However, the Tax Cuts and Jobs Act initiated a strict phase-down schedule:

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | |

| January 1, 2023 – December 31, 2023 | 80% | |

| January 1, 2024 – December 31, 2024 | 60% | |

| January 1, 2025 – January 18, 2025 | 40% | |

| January 19, 2025 – December 31, 2030 | 100% | Acquisition date is January 19, 2025 or later |

| 2025 (acquisition before January 19, 2025) | 40% | TCJA phase-down applies |

| 2026 (acquisition before January 19, 2025) | 20% | TCJA phase-down applies |

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Passive Activity Loss Rules and the Real Estate Professional Exception

When depreciation deductions (accelerated through cost segregation) offset rental income, investors may owe little or no federal tax on that income in the early years of ownership, dramatically improving the real after-tax return on the investment.

However, passive losses from rental properties can generally only offset other passive income, not W-2 wages or business income. For investors who qualify as Real Estate Professionals under IRS rules (more than 750 hours annually in real property trades representing more than 50% of total working time), these losses can offset ordinary income, making the tax benefit far more valuable.

Before/After Illustration:

Scenario: $600,000 rental property, $450,000 depreciable basis

| Item | Without Cost Segregation | With Cost Segregation |

|---|---|---|

| Gross rental income | $36,000 | $36,000 |

| Operating expenses | -$18,000 | -$18,000 |

| Mortgage interest | -$12,000 | -$12,000 |

| Depreciation | -$16,364 (standard) | -$72,000 (accelerated) |

| Taxable income | -$10,364 (passive loss, limited use) | -$66,000 (passive loss, limited use) |

For a Real Estate Professional, that $66,000 passive loss becomes an active loss that can offset $66,000 of W-2 income, saving $23,000+ in federal taxes at a 35% rate.

Frequently Asked Questions

How to make $1,000 a month in passive income?

Reaching $1,000 per month typically requires 3-5 rental properties each generating $200-$350 net monthly cash flow after all expenses, or one strong-performing property in a high-yield market. Building to this level generally takes 5-7 years, as current market conditions make finding a single property with $1,000+ monthly net cash flow increasingly rare.

Are rental properties good passive income?

Rental properties can be an excellent passive income source, but the quality of income depends on property selection, local market conditions, and how well you manage expenses and tenants. Success is not guaranteed; it requires thorough financial analysis, adequate reserves, and realistic expectations about both time commitment and returns.

What is the 2% rule in rental property?

The 2% rule states that monthly rent should equal 2% of purchase price, a quick-screen heuristic primarily used in lower-cost markets. In most markets today even the 1% rule is difficult to achieve, making thorough financial analysis using cap rates, cash-on-cash returns, and price-to-rent ratios essential for evaluating deals.

Does rental income affect SSDI?

Passive rental income generally does not count as "earned income" under Social Security rules and typically does not affect SSDI eligibility. However, if you provide substantial services to tenants (maid service, supplying linens, cleaning apartments), the income may be reclassified as self-employment earnings. A benefits counselor or attorney can provide guidance on specific situations, given that rules can be nuanced.

Is rental income truly passive or does it require active work?

Rental income is classified as passive by the IRS, but still demands owner involvement: roughly 4 hours per month per unit for routine operations, plus 47.5 hours per vacancy turnover. Self-management maximizes cash flow; hiring a property manager increases passivity but reduces net returns by 8-12%.

How much can a cost segregation study save on taxes for a rental property?

Cost segregation studies accelerate depreciation deductions that would otherwise be spread over 27.5 years, typically identifying $40,000 to $171,000+ in first-year deductions. At a 35% tax rate, that translates to $14,000–$60,000+ in Year 1 tax savings—well above the $5,000–$15,000 cost of the study.