Introduction

Many landlords spend decades building rental portfolios, yet leave their estates exposed to probate delays, tenant lawsuits, and steep tax burdens because they never built a proper estate plan.

Take a landlord who owns three single-family rentals and a duplex. A basic will seems sufficient, until heirs discover the portfolio frozen in probate for 18 months while rent goes uncollected and property values slide.

Standard estate plans built for primary residences simply don't account for what rental property ownership involves. Investment properties generate income, carry liability exposure, and often span multiple states, each adding a layer of complexity a generic will ignores.

This guide covers the legal structures that shield your portfolio from lawsuits, trust strategies that ensure seamless succession, tax optimization techniques that preserve maximum value for heirs, and the most common and costly planning mistakes landlords make.

TLDR

- LLCs separate personal wealth from rental property liabilities, preventing tenant lawsuits from reaching your other holdings

- Living trusts holding LLC interests bypass probate entirely, keeping rent flowing to heirs without court delays

- The step-up in basis benefit eliminates all capital gains taxes on lifetime appreciation when heirs inherit property

- Cost segregation front-loads tax deductions during ownership, freeing capital to grow your portfolio before it ever passes to heirs

- Skipping proper planning means probate, a 9-20 month process that can consume 3-8% of your estate's total value in court and attorney fees

Why Rental Properties Require More Than a Standard Estate Plan

Investment properties differ from primary residences in estate planning. They generate monthly income, expose owners to premises liability, require ongoing management decisions, and typically involve multiple assets rather than one home. A landlord with four rental properties manages:

- Four separate income streams to collect and report

- Four sets of tenant relationships to maintain

- Four insurance policies to manage

- Four distinct liability exposures under one name

Standard estate documents never address this complexity.

Two core risks destroy value when landlords use generic plans: personal liability exposure and probate paralysis. When rental properties sit in your personal name, a slip-and-fall lawsuit or tenant injury claim at one property can reach your entire net worth, including other properties, retirement accounts, and personal savings. Courts don't recognize invisible boundaries between properties when everything carries your name on the deed.

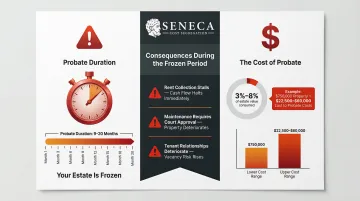

Probate court compounds the problem. Probate proceedings typically consume 9 to 20 months and drain 3% to 8% of an estate's gross value through executor fees, attorney costs, and mandatory appraisals. For a $750,000 rental property, that's $22,500 to $60,000 lost to administrative costs alone.

| Property Value | 3% Probate Cost | 8% Probate Cost |

|---|---|---|

| $750,000 | $22,500 | $60,000 |

During this frozen period, rent collection stalls, maintenance decisions wait for court approval, and tenant relationships deteriorate. Property value erodes rapidly when no one has legal authority to act.

Landlords with multiple properties face an additional challenge: income continuity. If rents aren't collected and bills aren't paid during estate administration, properties slide into disrepair, tenants leave, and the portfolio's value collapses before heirs ever take control.

Legal Structures That Shield Your Rental Portfolio from Liability

Holding rental properties in your personal name exposes your entire net worth to lawsuits arising from any single property. A tenant injury, lease dispute, or code violation fine can pierce through to your other holdings and personal savings because no legal barrier exists between the property and your wealth.

Forming an LLC for Each Property or Portfolio

The Limited Liability Company structure solves this problem by creating separation between business liabilities and personal assets. When you deed rental properties into an LLC, judgments against one property generally cannot reach other holdings or personal wealth. Creditors can pursue the LLC's assets, but your personal bank accounts, primary residence, and other properties remain protected.

Landlords face a strategic choice: single LLC for all properties versus separate LLCs per property. Each approach involves real tradeoffs:

| Structure | Description |

|---|---|

| Portfolio LLC | one set of annual filings, one operating agreement, one tax return, but a lawsuit against any single property exposes the equity in all holdings within it |

| Single-asset LLC | complete liability isolation between properties, but multiplies administrative burden and state filing fees |

| Hybrid grouping | one LLC per state or region, or risk-based clusters separating high-risk properties from stable long-term holdings |

A landlord with three properties in Portland and two in Seattle, for instance, might form two LLCs to balance protection with manageability.

Critical limitation: An LLC alone does not avoid probate. Your ownership interest in the LLC—your membership interest—still passes through your estate. When you die, the LLC membership becomes an estate asset subject to probate court unless you've transferred that interest to a trust. This is why the LLC-plus-trust combination represents the most complete structure for rental property protection.

Other Structures to Consider

Family Limited Partnerships (FLPs) allow landlords to transfer minority partnership interests to heirs at discounted valuations, potentially reducing estate tax exposure. However, the IRS aggressively scrutinizes FLPs under IRC §2036, requiring legitimate non-tax business purposes and actual operational substance beyond paper arrangements.

Corporations rarely make sense for rental property ownership due to double taxation and the inability to pass through losses to owners. They're occasionally used in complex commercial portfolios where public offerings or institutional investment is planned.

A landlord with two properties and one heir needs different protection than an investor with 15 properties across three states planning to transfer assets to four children. Portfolio size, number of heirs, state laws, and management goals all shape the right choice.

Using Trusts to Ensure Seamless Property Succession

A revocable living trust serves one critical function for rental properties: it allows you to transfer ownership of properties (or LLC membership interests) to the trust during your lifetime, designate a successor trustee, and ensure that upon death or incapacity, a trusted person takes control immediately—no probate court required.

You create the trust document, name yourself as initial trustee (maintaining full control), designate a successor trustee, then formally transfer property titles or LLC membership interests into the trust's name. When you die, the successor trustee steps into your role automatically, with immediate legal authority to manage properties, collect rent, pay bills, and maintain tenant relationships.

The LLC-Plus-Trust Structure

The layered approach combines both tools: properties are deeded into LLCs for liability protection, then LLC membership interests are assigned to the living trust for succession planning. This creates a structure that handles liability isolation and probate avoidance simultaneously.

How it works in practice: You form an LLC and deed your rental property into it. Then you execute a membership interest assignment transferring your ownership of the LLC from your personal name to your living trust. The trust now owns the LLC, and the LLC owns the property. When you die, your successor trustee immediately controls the LLC membership interest (no court approval needed) and can seamlessly manage the LLC's operations, which include collecting rent, paying mortgages, and handling tenant issues.

Because the successor trustee acts immediately using authority granted in the trust document, this structure preserves property income and value during a transition period when many estates lose significant income waiting on probate courts.

Choosing the Right Type of Trust

Revocable living trusts offer complete flexibility during your lifetime. You maintain full control, can amend or revoke the trust at any time, can buy and sell properties freely, and face no tax consequences from the trust's existence. The trust becomes irrevocable only at death, at which point it avoids probate and distributes assets according to your instructions.

Irrevocable trusts require giving up control but provide stronger asset protection and potential estate tax benefits. Once you transfer property into an irrevocable trust, you cannot reclaim it or modify the trust terms without beneficiary consent. This permanence creates a legal barrier that protects assets from future creditors and removes property value from your taxable estate.

That loss of control makes irrevocable trusts appropriate only for landlords with substantial estates exceeding federal estate tax exemptions (approximately $28 million for married couples under current 2026 projections) or those facing specific creditor threats.

Trust Type Comparison

| Feature | Revocable Living Trust | Irrevocable Trust |

|---|---|---|

| Control during lifetime | Full control maintained; can amend or revoke at any time | Requires giving up control; cannot reclaim or modify terms without beneficiary consent |

| Flexibility | Properties can be bought and sold freely | Permanence creates a legal barrier |

| Tax consequences | No tax consequences from the trust's existence | Removes property value from taxable estate |

| Asset protection | — | Protects assets from future creditors |

| Probate | Avoids probate at death | Avoids probate at death |

Specialized trust tools serve niche purposes. Qualified Personal Residence Trusts (QPRTs) apply only to personal residences, not rental properties. Charitable Remainder Trusts (CRTs) can defer capital gains but face complications when rental properties carry mortgage debt, which triggers 100% excise tax on unrelated business taxable income.

Planning for Property Management Continuity

The successor trustee needs clear, detailed instructions. Should they hold properties and distribute rental income to beneficiaries monthly? Sell properties for lump-sum distribution? Transition management to a professional property manager? The trust document must specify these directions.

Key decisions to document:

- Whether properties should be held long-term or sold

- How rental income should be distributed among beneficiaries

- Who pays property expenses, taxes, and maintenance costs

- When and how properties can be sold

- Whether professional property management should be hired

- How disputes between beneficiaries will be resolved

Without these instructions, successor trustees face paralysis, beneficiaries fight over strategy, and property value deteriorates while everyone argues.

Tax Planning Strategies to Maximize What You Pass On

Estate planning isn't just about transferring properties—it's about transferring maximum value. Tax planning during ownership and at the point of transfer dramatically affects how much heirs actually receive.

The Step-Up in Basis Advantage

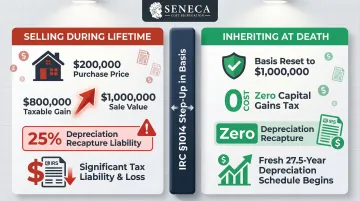

Under IRC §1014, when heirs inherit rental property, their tax basis resets to fair market value at the date of death. All capital gains accumulated during the original owner's lifetime are permanently eliminated.

Example: You bought a rental property for $200,000 twenty years ago. It's now worth $1,000,000 at your death. Your heir's basis becomes $1,000,000. If they sell immediately, they pay zero capital gains tax on the $800,000 appreciation you enjoyed during your lifetime.

This benefit is extraordinary: it wipes out decades of appreciation with no tax consequence. However, gifting properties during your lifetime destroys this advantage. Under IRC §1015, gifts carry "carryover basis": the recipient inherits your original low basis. If you gift that same $1,000,000 property, your heir receives your $200,000 basis and owes capital gains tax on $800,000 when they sell.

| Transfer Method | Original Purchase Price | Property Value | Heir's Tax Basis | Taxable Gain on Immediate Sale |

|---|---|---|---|---|

| Inherited at death (step-up in basis) | $200,000 | $1,000,000 | $1,000,000 | $0 |

| Gifted during lifetime (carryover basis) | $200,000 | $1,000,000 | $200,000 | $800,000 |

Critical planning note: Highly appreciated rental properties held until death secure the step-up in basis. Gifting them early eliminates this advantage unless the estate genuinely exceeds exemption thresholds.

Depreciation Recapture Considerations

Rental property owners claim depreciation deductions during ownership—residential properties depreciate over 27.5 years. When you sell, you normally pay 25% "unrecaptured Section 1250 gain" tax on all claimed depreciation.

The estate planning advantage: The step-up in basis at death eliminates the decedent's accumulated depreciation liability entirely. Your heirs inherit the property free of your recapture obligation and begin a brand-new 27.5-year depreciation schedule based on the new fair market value. This double benefit (erasing capital gains and depreciation recapture) makes holding rental properties until death extraordinarily tax-efficient.

Maximizing Estate Value Through Tax-Efficient Ownership

Cost segregation, an engineering-based IRS strategy, accelerates depreciation on rental properties by identifying building components that qualify for 5-, 7-, or 15-year depreciation instead of 27.5 years. This generates substantial first-year tax deductions that reduce federal tax burden during ownership, freeing capital to reinvest, grow the portfolio, and ultimately pass on a larger estate.

The July 2025 passage of the One Big Beautiful Bill Act (OBBBA) restored 100% bonus depreciation for property acquired on or after January 19, 2025, making cost segregation even more powerful. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | |

| January 1, 2023 – December 31, 2023 | 80% | |

| January 1, 2024 – December 31, 2024 | 60% | |

| January 1, 2025 – January 18, 2025 | 40% | |

| January 19, 2025 – December 31, 2030 | 100% | Applies if acquisition date is January 19, 2025 or later |

| 2025 (acquired before January 19, 2025) | 40% | TCJA phase-down applies |

| 2026 (acquired before January 19, 2025) | 20% | TCJA phase-down applies |

According to the American Society of Cost Segregation Professionals (ASCSP), quality studies on apartment buildings typically reallocate 20% to 40% of building basis to shorter recovery periods.

Seneca Cost Segregation specializes in engineering-based cost segregation studies for rental property owners, from single-family homes to multi-family complexes. With over 12 years of experience and more than 10,200 properties assessed, the firm's engineering team has identified an average first-year deduction of $171,243 for clients nationwide.

These immediate tax savings increase cash flow and investment capacity, directly building the estate value you'll eventually transfer to heirs.

Federal Estate Tax Planning

The OBBBA permanently increased the federal estate tax exemption to $15 million per individual for 2026, averting the scheduled sunset. For married couples, this creates a $30 million combined exemption. Landlords with portfolios below these thresholds face zero federal estate tax and planning focuses entirely on income tax optimisation, asset protection, and state-level estate taxes.

For portfolios exceeding $15 million, proactive strategies become essential: gifting programmes using the annual gift exclusion ($19,000 per recipient in 2025), irrevocable trusts that remove assets from the taxable estate, and Family Limited Partnerships that transfer discounted minority interests to heirs while retaining control.

Common Estate Planning Mistakes Landlords Make

| Mistake | Why It's Problematic |

|---|---|

| Holding all properties in personal name, with no entity structure (most frequent error) | Every asset you own is exposed to liability from any single property, and the entire portfolio passes through probate. One tenant lawsuit can reach everything. |

| Unfunded trust (second most damaging; far more common than most landlords expect) | The trust document itself does nothing. Properties must be formally transferred into the trust's name through recorded deeds or LLC membership assignments. Unfunded trusts are a primary cause of estate litigation; assets left outside the trust pass through probate exactly as if no trust existed. |

| Relying on a generic will to manage a multi-property portfolio | Creates a public, court-supervised process that stalls rental income, triggers heir disputes, and incurs steep legal fees calculated against gross property value. Wills guarantee probate: they're instructions to the probate court, not tools to avoid it. |

Additional common mistakes include:

- Owning properties across multiple states without planning for ancillary probate in each jurisdiction

- Forming single-member LLCs in states without charging order exclusivity, leaving assets open to creditor foreclosure

- Gifting appreciated properties during lifetime, eliminating the step-up in basis benefit

- Failing to coordinate LLC operating agreements with trust provisions

- Naming minor children as direct beneficiaries instead of creating trusts for their benefit

- Not updating plans after acquiring new properties or experiencing major life events

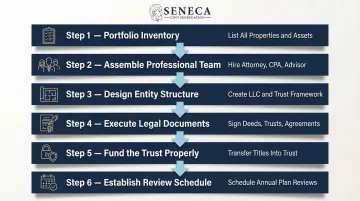

Steps to Build a Rental Property Estate Plan

| Step | Description |

|---|---|

| 1 | Complete portfolio inventory |

| 2 | Assemble a professional team |

| 3 | Design the structure |

| 4 | Execute legal documents |

| 5 | Fund the trust properly |

| 6 | Establish review schedule |

Step 1: Complete portfolio inventory. This step involves documenting every rental property's ownership structure, outstanding mortgages, estimated market value, existing entity structures, and current basis. Property addresses, acquisition dates, purchase prices, capital improvements, and accumulated depreciation are included. This baseline shapes every decision that follows.

Step 2: Assemble a professional team. Three specialists are involved:

- Estate planning attorney to structure trusts and LLCs, draft operating agreements, and ensure documents comply with state laws

- CPA or tax advisor to address depreciation strategy, estate tax exposure, capital gains planning, and step-up in basis optimization

- Cost segregation specialist (optional but valuable) to maximize tax position of properties still in the portfolio through accelerated depreciation strategies

Seneca Cost Segregation partners with CPAs and tax advisors to deliver engineering-based cost segregation studies averaging $171,243 in first-year deductions, and provides audit defense if the IRS questions the findings.

Step 3: Design the structure. Based on portfolio size, liability exposure, and succession goals, the appropriate structure—whether single-asset LLCs, portfolio LLCs, or a tiered structure—is identified. The choice between revocable and irrevocable trusts is informed by estate size and asset protection needs.

Step 4: Execute legal documents. LLCs are formed, trust documents are created, deeds are executed transferring properties into LLCs, and LLC membership interests are assigned to trusts. All deeds are recorded in appropriate county registries. LLC membership ledgers are updated to reflect trust ownership.

Step 5: Fund the trust properly. This step separates successful estate plans from expensive failures. Every asset—LLC membership interests, bank accounts holding security deposits, property management agreements—is transferred into the trust's name. Transfers are verified as recorded and documented.

Step 6: Establish review schedule. Estate plans are not one-time documents. Rental portfolios grow, tax laws shift, and family circumstances evolve. Plans are reviewed and updated every 3 to 5 years, whenever new properties are acquired, and following major life events like marriage, divorce, birth of children, or significant tax law changes.

Frequently Asked Questions

What is the 5 by 5 rule in estate planning?

The 5 by 5 rule (IRC §2041(b)(2)) is a trust provision allowing beneficiaries to withdraw the greater of $5,000 or 5% of the trust's principal each year without triggering gift or estate tax implications. For landlords, it provides beneficiaries controlled access to accumulated rental income without requiring full trust distribution.

What are common mistakes to avoid in estate planning?

The top mistakes include failing to fund a trust after creating it, using only a will for investment properties, holding properties in personal name without an LLC, not updating the plan after acquiring new properties or following major tax law changes, and gifting appreciated properties during lifetime instead of holding them for the step-up in basis benefit.

Should I put my rental properties in an LLC or a trust?

The ideal approach is typically both: an LLC for liability protection and a living trust to hold the LLC interest for probate-free succession. Each tool solves a different problem: LLCs shield you from lawsuits and trusts bypass probate, and they work best in combination, creating comprehensive protection for your rental portfolio.

What happens to depreciation deductions when rental property is inherited?

The heir receives a new stepped-up basis at fair market value, which resets the depreciation schedule. The step-up eliminates accumulated depreciation recapture obligations entirely, letting heirs start a fresh 27.5-year depreciation schedule based on the inherited value.

Can I avoid probate for my rental properties without a trust?

Some states allow transfer-on-death deeds for real property, which bypass probate for individual properties by designating beneficiaries who automatically receive title at death. However, a living trust combined with an LLC remains the most comprehensive and flexible solution for multi-property rental portfolios, providing both probate avoidance and incapacity protection.

Do I need a separate estate plan for each rental property I own?

No. A single well-structured estate plan using a master living trust and appropriately organized LLCs can cover an entire portfolio. Larger or geographically diverse portfolios may benefit from tiered structures, such as separate LLCs per state or property cluster, to maximize liability protection while keeping succession planning centralized in one trust.