Introduction

Most commercial property owners approach tax strategy with an either-or mindset: either claim accelerated depreciation through cost segregation, or pursue the Section 179D energy-efficient buildings deduction. The assumption is that you have to choose. You don't.

Both strategies are designed to work together and can be applied to the same building in the same tax year. They work because they target fundamentally different assets: cost segregation reclassifies shorter-lived components like specialty electrical and flooring into 5, 7, and 15-year property, while 179D directly deducts energy systems — HVAC, lighting, and building envelope — that cost segregation doesn't touch.

When properly stacked, these two strategies generate deductions that neither approach could achieve alone. The result: maximum first-year write-offs and capital freed up for your next investment. This article breaks down how each strategy works, where they overlap, and how to sequence them for the greatest tax impact.

TLDR

- Cost segregation accelerates depreciation on reclassifiable components (flooring, specialty wiring, land improvements) out of the 27.5/39-year schedule

- 179D adds up to $5.94/sq ft for energy-efficient HVAC, lighting, and envelope systems — assets cost segregation can't touch

- The two strategies target non-overlapping categories, so combining them on one property maximizes first-year deductions

- Together, they free up capital faster for reinvestment in your next acquisition

What Is 179D and What Is Cost Segregation?

Defining Section 179D

Section 179D (the Energy-Efficient Commercial Buildings Deduction) is a federal incentive that allows building owners to deduct a set dollar amount per square foot for qualifying energy-efficient improvements.

For tax years beginning in 2026, maximum deduction rates are $5.94/sq ft for Prevailing Wage and Apprenticeship (PWA)-compliant projects and $1.19/sq ft for non-PWA projects. The deduction applies to three building systems:

- HVAC and hot water systems

- Interior lighting systems

- Building envelope (insulation, windows, roof assemblies)

Qualification requires meeting minimum energy savings thresholds—25% reduction in total annual energy and power costs compared to the applicable ASHRAE 90.1 reference standard. A certified energy engineer must perform a third-party energy study to verify eligibility and certify which systems qualify.

Eligible properties include commercial buildings and residential rental buildings of four or more stories. Architects, engineers, and designers working on government-owned buildings may claim the deduction via "allocation," making 179D one of the only tax incentives available to non-owners in those specific cases.

Defining Cost Segregation

Where 179D targets energy performance, cost segregation works at the asset level. A cost segregation study is an engineering-based analysis that reclassifies building components from 27.5-year (residential) or 39-year (commercial) property into 5, 7, or 15-year asset classes. Common reclassifications include:

- Specialty electrical systems (security wiring, data cabling)

- Plumbing fixtures and decorative elements

- Flooring, carpet, and cabinetry

- Parking lots, landscaping, and site improvements

These reclassified assets then qualify for bonus depreciation, generating front-loaded deductions in year one. With the One Big Beautiful Bill Act (OBBBA) permanently reinstating 100% bonus depreciation for qualifying property placed in service after January 19, 2025, investors can now deduct the full cost of qualifying short-life assets in the year placed in service rather than spreading them over decades.

Properties typically see 20–40% of their depreciable basis reclassified into shorter class lives — translating directly into cash back at tax time.

Why 179D and Cost Segregation Are Built to Work Together

The Core Complementary Logic

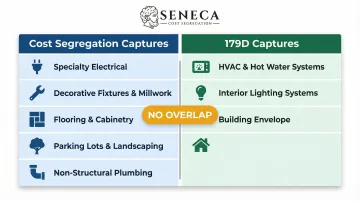

Cost segregation and 179D do not overlap. Cost segregation reclassifies shorter-lived personal property and land improvements—items that are not integral structural components. But HVAC systems, lighting installations, and building envelope components are structural components defined under Treasury Regulation §1.48-1(e)(2) that cannot be reclassified into shorter class lives through cost segregation. This is precisely where 179D steps in, delivering immediate deductions on the exact assets that cost segregation leaves behind.

Asset Coverage by Strategy:

| Cost Segregation Captures | 179D Captures |

|---|---|

| Specialty electrical (security, data) | HVAC and hot water systems |

| Decorative fixtures and millwork | Interior lighting systems |

| Flooring, carpet, cabinetry | Building envelope (insulation, windows, roof) |

| Parking lots and landscaping | — |

| Non-structural plumbing | — |

Because the asset categories are mutually exclusive, there is no double-counting risk. The IRS Cost Segregation Audit Techniques Guide explicitly requires that 179D deductions reduce the depreciable basis of qualifying energy systems before calculating bonus depreciation, ensuring proper basis ordering without overlap.

The Compounding Deduction Effect

When both strategies are applied to a single property, the total deductible pool expands in a measurable way. Cost segregation typically reclassifies 20-40% of a building's depreciable basis into accelerated schedules. 179D adds a separate per-square-foot deduction for energy systems. Together, first-year deductions can exceed what either strategy would achieve alone by 30-50%, depending on property type and energy efficiency levels.

Cash Flow Amplification

Larger first-year deductions mean more capital freed up immediately. That cash can be redirected into:

- Property improvements and upgrades

- Debt paydown to improve loan ratios

- Acquisition of additional properties

- Working capital for operations

This accelerates reinvestment velocity. In competitive acquisition markets, getting capital back faster is often the difference between closing on the next deal or watching it go to someone else.

Strategic Sequencing

The cost segregation study should be performed first (or in tandem with 179D planning). The detailed asset-by-asset breakdown it produces:

- Identifies which building systems may qualify for 179D energy study

- Provides the cost allocation baseline needed for proper basis calculations

- Ensures both studies use consistent property data and documentation

Engineering-based studies that deliver this asset-level documentation — completed within 2-4 weeks — give tax advisors the clean, consistent data needed to coordinate both strategies before filing deadlines. Seneca Cost Segregation's studies are structured specifically to support that coordinated workflow.

How to Stack 179D and Cost Segregation: A Practical Approach

Step 1 — Determine Eligibility Before You Start

Confirm property type qualifies:

- 179D: Commercial building or residential 4+ stories

- Cost segregation: Any commercial or residential rental property

Identify project status:

- New construction

- Renovation or retrofit

- Existing building (acquired or refinanced)

All three categories can qualify for both strategies, but documentation requirements differ slightly. Note that 179D retrofits (qualifying retrofit projects on existing buildings) have their own deduction pathway with specific Energy Use Intensity (EUI) certification requirements.

Step 2 — Commission an Engineering-Based Cost Segregation Study

An IRS-compliant, engineering-based study—not a software-only estimate—is essential. The study must:

- Identify and document every reclassifiable asset

- Provide cost allocation data by asset class

- Follow IRS Cost Segregation Audit Techniques Guide standards

- Support 179D energy certification with detailed system-level data

The study output becomes the foundation for both strategies. Seneca Cost Segregation's engineering team delivers this documentation within 2-4 weeks, backed by AuditDefense and a money-back guarantee.

Step 3 — Engage a Qualified Energy Engineer for 179D Certification

A separate third-party energy analysis is required to certify 179D eligibility. The energy engineer:

- Models energy performance against ASHRAE reference standards

- Certifies which systems (HVAC, lighting, envelope) qualify

- Calculates the per-square-foot deduction rate based on energy savings percentage

- Issues IRS-compliant certification documentation

This is a distinct study from cost segregation, but it draws on overlapping property data. The cost segregation report's asset-level detail gives the energy engineer ready-made cost allocations for qualifying systems, reducing the time and effort needed to complete certification — which carries directly into Step 4.

Step 4 — Coordinate with Your CPA for Proper Tax Reporting

With both studies in hand, your CPA can file each deduction correctly:

- Cost segregation: Report on the depreciation schedule (Form 4562), with reclassified assets listed by MACRS class life

- 179D: Report separately using Form 7205 as a standalone deduction on the return

Key coordination points:

- Have both the cost segregation report and 179D certification ready before filing

- Reduce the depreciable basis of qualifying 179D systems before calculating bonus depreciation

- Flag state-level conformity issues—most states conform to federal 179D treatment, but bonus depreciation conformity varies significantly by state

California, Connecticut, Delaware, Michigan, and the District of Columbia have all decoupled from federal 100% bonus depreciation, requiring add-backs on state returns.

Step 5 — Plan for Recapture Before Selling

Section 1245 recapture: Accelerated depreciation through cost segregation creates ordinary income recapture upon sale. The gain is treated as ordinary income to the extent of depreciation allowed or allowable.

179D basis reduction: Reduces depreciable basis, which factors into gain calculations at disposition.

Exit planning strategies:

- 1031 exchange to defer recognition of gain

- Hold period analysis to time disposition for favorable tax years

- Partial asset disposition elections to manage recapture exposure

The upfront benefit rarely disappears at exit. Recapture is taxed at a maximum 25% rate for real property depreciation — well below the cash-on-cash returns most investors generate by deploying those front-loaded deductions in years 1-5. Exit planning doesn't eliminate the strategy; it just accounts for the math at the back end.

A Real-World Example: Stacking Both Strategies on a Commercial Property

Here's how the numbers play out when both strategies are applied to the same property.

Scenario: A commercial property owner acquires a 50,000-square-foot office/retail building with a total depreciable basis of $5,000,000.

Cost Segregation Result

An engineering-based study identifies 25% of the depreciable basis as 5, 7, or 15-year property. With 100% bonus depreciation:

- Reclassified assets: $5,000,000 × 25% = $1,250,000

- First-year bonus depreciation deduction: $1,250,000

179D Result

The building includes qualifying LED lighting, a high-efficiency HVAC system, and enhanced insulation meeting the 25% energy savings threshold. Using the 2026 PWA-compliant maximum rate:

- 179D deduction: 50,000 sq ft × $5.94/sq ft = $297,000

Combined First-Year Deductions

Total first-year deductions:

- Cost segregation bonus depreciation: $1,250,000

- 179D deduction: $297,000

- Combined total: $1,547,000

Comparison to straight-line depreciation:

- 39-year straight-line annual deduction: $5,000,000 ÷ 39 = $128,205

- First-year advantage: $1,547,000 – $128,205 = $1,418,795 additional deduction

Tax savings (assuming 37% marginal rate):

- $1,547,000 × 37% = $572,390 first-year tax savings

That $572,390 in preserved capital can go directly toward the next acquisition, a renovation draw, or paying down debt — well before straight-line depreciation would have returned a fraction of that amount.

Who Qualifies and What to Watch Out For

Who Benefits Most

Primary candidates for stacking both strategies:

- Commercial property owners (office, retail, warehouse, hospitality)

- Multifamily building owners with 4+ stories

- Developers of new construction or major renovations

- Real estate investors making energy-efficiency upgrades

- Architects and engineers on government-owned projects (179D allocation pathway)

Key Limitations and Thresholds

179D requirements:

- Must meet 25% energy savings threshold (below-threshold buildings may qualify for reduced $/sq ft rate)

- Requires certified energy engineer study and IRS-compliant documentation

- Deduction (not credit)—dollar value depends on taxpayer's marginal tax rate

Cost segregation requirements:

- Sufficient depreciable basis to justify study costs, generally $500,000+ property value

- Engineering-based study required (software-only estimates increase audit risk)

- Properties under minimum threshold may not generate enough savings to offset study fees

Documentation and Compliance

Both strategies require professional third-party studies:

- 179D: IRS-compliant energy certification by qualified engineer using Form 7205

- Cost segregation: Studies following IRS Audit Techniques Guide standards

Cutting corners on either increases audit risk. Seneca's engineering-based studies include AuditDefense with a money-back guarantee—if the IRS challenges the study methodology or asset classifications, Seneca covers the defense costs.

Frequently Asked Questions

Can you take bonus depreciation and Section 179 in the same year?

Yes, both can be used in the same tax year. Section 179 is applied first to elected assets, and bonus depreciation then applies automatically to remaining qualified property. Section 179 cannot create a net operating loss, while bonus depreciation can.

What is cost segregation 179?

"Cost segregation 179" refers to combining cost segregation with either Section 179 (equipment expensing) or Section 179D (energy-efficient buildings deduction). Cost segregation identifies the assets; Section 179 or 179D provides the mechanism for accelerated or immediate deductions.

Does the 179D deduction reduce the depreciable basis for cost segregation?

179D deductions are taken separately and reduce the depreciable basis of the qualifying energy systems. However, because 179D covers HVAC, lighting, and envelope—assets cost segregation cannot reclassify anyway—taking 179D does not reduce the pool of assets available for cost segregation reclassification.

Who qualifies for the 179D deduction?

Owners of commercial buildings and residential buildings 4+ stories qualify, as well as architects, engineers, and designers on qualifying government-owned projects who receive an allocation from the building owner.

What building systems qualify for the 179D deduction?

Three qualifying system categories: HVAC and hot water systems, interior lighting systems, and the building envelope (insulation, windows, roof). A certified energy engineer must verify that each system meets specific energy savings thresholds.

Can I still claim 179D if my property already had a cost segregation study done?

Yes—a prior cost segregation study does not disqualify a property from 179D. In fact, existing cost segregation documentation can accelerate the 179D certification process by providing detailed asset cost allocations.

Ready to maximize your first-year deductions? Seneca Cost Segregation has helped investors across all 50 states capture an average of $171,243 in first-year deductions. Engineering-based studies are completed in 2-4 weeks. Contact us today at 503-383-1158 or info@senecacostseg.com to schedule your complimentary property analysis and discover how stacking 179D and cost segregation can accelerate your portfolio growth.