Introduction

The average engineering-based cost segregation study generates over $171,000 in first-year deductions — yet most real estate investors are still using standard depreciation schedules that spread those savings across 27.5 to 39 years. The type of study you choose significantly changes how much you save, and engineering-based studies consistently outperform alternatives in both accuracy and IRS defensibility.

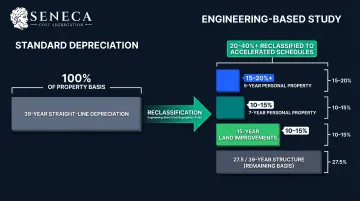

Standard depreciation schedules spread property costs over 27.5 or 39 years. Engineering-based cost segregation studies legally reclassify building components to accelerate deductions to 5, 7, or 15 years, which generates significantly more cash flow in the early years of ownership.

This post covers what an engineering-based cost segregation study is, how it works step-by-step, what makes it different from other study types, and how real estate investors use it to generate outsized first-year tax savings.

TL;DR

- Licensed engineers inspect and reclassify property components into 5-, 7-, or 15-year depreciation schedules instead of the standard 27.5/39-year timeline

- Identifies 20–40%+ more qualifying property than accounting-based or DIY studies, with full IRS-compliant documentation

- Generates an average first-year deduction of $171,243, accelerating cash flow for reinvestment

- Serves commercial, multi-family, rental, and owner-occupied properties typically valued at $300,000+

- Reduces audit risk through engineering-grade documentation and defensible study methodology

What Is an Engineering-Based Cost Segregation Study?

An engineering-based cost segregation study is a formal tax analysis conducted by licensed engineers. They review construction documents, inspect the property, and systematically reclassify building components from long-life real property (27.5/39-year) into shorter-life personal property (5/7-year) or land improvements (15-year), all in accordance with IRS guidelines, including the Cost Segregation Audit Techniques Guide.

What a Cost Segregation Engineer Actually Does

Cost segregation engineers go well beyond a desk review. Their work involves:

- Conducting site inspections or reviewing detailed construction records

- Analyzing mechanical, electrical, and plumbing (MEP) systems

- Identifying specialty components like dedicated electrical circuits, security systems, or process-specific HVAC

- Allocating costs to each asset class using construction-based methodologies, not statistical averages or assumptions

The IRS Cost Segregation Audit Techniques Guide explicitly recognizes the "detailed engineering approach from actual cost records" as the "most methodical and accurate approach, relying on solid documentation and minimal estimation."

Engineering-Based vs. Other Study Types

Not all cost segregation studies carry the same weight with the IRS. Engineering-based studies rely on licensed engineers, site inspections, and component-level analysis. Accounting-based or DIY studies, by contrast, use rule-of-thumb estimates, statistical averages, and limited documentation.

The IRS specifically recognizes engineering-based studies as more reliable and defensible, cautioning that rule-of-thumb approaches can be "less accurate" and lack sufficient documentation.

Why Engineering-Based Studies Maximize Your Tax Savings

Precision Uncovers Hidden Deductions

The core advantage is precision. Engineering analysis breaks down lumped-sum costs into individual components, uncovering qualifying personal property that accounting methods routinely miss:

- Specialty electrical circuits

- Dedicated HVAC systems

- Removable interior walls

- Flooring and carpeting

- Security and telecom systems

- Built-in cabinetry and fixtures

Reclassification Impact on Depreciation

Instead of depreciating 100% of the property over 39 years, an engineering study typically reclassifies 20–40%+ of the depreciable basis into shorter-lived property categories: 5-year, 7-year, or 15-year classes. That shift front-loads deductions and frees up cash in the years it matters most for reinvestment.

IRS Defensibility

Engineering-based reports include direct references to IRS authority (Revenue Procedure 87-56, Asset Class guidelines, the Whiteco permanency factors), detailed construction drawings, and annotated asset-level documentation—giving property owners a defensible audit trail that DIY or abbreviated studies cannot provide.

Bonus Depreciation Amplifies Savings

The One, Big, Beautiful Bill Act (OBBBA) of 2025 permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. Reclassified short-life property identified in an engineering study can often be fully expensed in year one—meaning a more precise study directly translates to a larger first-year deduction.

Benefits Snapshot

- Increased first-year cash flow

- Legally reduced taxable income

- Reduced audit risk

- Ability to reinvest tax savings faster

- Written study your CPA can rely on at filing or under IRS review

How an Engineering-Based Cost Segregation Study Works

An engineering-based cost segregation study follows a structured, property-specific process — not a one-size-fits-all template. Each step is designed to capture every reclassifiable component so your CPA receives accurate depreciation schedules, not generic estimates. Here's how it works.

Step 1 – Initial Property Assessment and Feasibility Review

The engineer reviews basic property details—purchase price, property type, construction costs, acquisition date—to determine whether a study will generate enough tax benefit to justify the cost. Typically, properties with a depreciable basis of $300,000+ yield meaningful results.

Step 2 – Document Collection and Construction Review

Engineers gather all available documentation:

- Architectural plans and blueprints

- Contractor invoices and AIA payment applications (Forms G-702, G-703)

- Change orders and specifications

- Purchase agreements and closing statements

This enables accurate cost allocation at the component level rather than relying on estimates. The IRS expects studies to be based on reliable published sources such as R.S. Means or Marshall Valuation Service.

Step 3 – Site Inspection and Component Identification

A licensed engineer inspects the property to:

- Document actual installed conditions

- Photograph assets

- Verify construction details

- Identify specialty components that drawings may not fully capture—such as process-specific electrical systems, specialized MEP (mechanical, electrical, and plumbing) installations, or land improvements

Step 4 – Asset Classification and Cost Allocation

Each identified component is classified using IRS recovery periods (5-year, 7-year, 15-year, 27.5/39-year). Classification draws on Revenue Procedure 87-56, the Whiteco permanency factors, and IRS Audit Technique Guide standards.

The IRS applies the Whiteco Permanency Test to determine whether an asset qualifies as personal property or a structural component. The six factors it evaluates:

- Movability and portability

- Design intent of the asset

- Circumstances of installation

- Effort required for removal

- Potential damage upon removal

- Manner of affixation to the structure

Costs are allocated using construction cost data, published pricing sources (R.S. Means, Marshall Valuation Service), or direct invoice tracing.

Step 5 – Report Preparation and CPA Delivery

A formal engineering report is produced with full documentation:

- Asset schedules

- Classification rationale

- Supporting references to IRS authority

- Depreciation schedule your CPA needs to file correctly

Quality engineering studies also include audit defense documentation so the methodology can be explained and defended if the IRS inquires.

Engineering-Based Cost Segregation: A Simplified Example

The Scenario

A real estate investor purchases a $1.2M multi-family apartment complex. Land value is $200,000, leaving a depreciable basis of approximately $1,000,000. Under standard depreciation, the entire basis would be spread over 27.5 years—yielding roughly $36,000 per year in depreciation deductions.

What the Engineering Study Uncovers

The engineer inspects the property and identifies qualifying components:

| Asset Class | Examples | % of Depreciable Basis |

|---|---|---|

| 5-year personal property | Appliances, flooring, specialty lighting, window treatments | ~15% |

| 7-year property | Carpeting, cabinetry, specialized electrical | ~10% |

| 15-year land improvements | Parking lot, landscaping, site utilities | ~10% |

Total reclassified: approximately 35% of the depreciable basis, or $350,000.

First-Year Impact with 100% Bonus Depreciation

With 100% bonus depreciation restored in 2025, the reclassified components can be fully expensed in year one:

- Reclassified assets: $350,000

- Standard 27.5-year depreciation on remaining $650,000: ~$23,600

- Total first-year depreciation: $373,600

Compared to the baseline $36,000 annual deduction, the engineering-based study generated an additional $337,600 in first-year deductions.

This substantial deduction reduces taxable income, potentially creating a paper loss that offsets other income (subject to passive activity rules and Real Estate Professional status). Those cash savings go directly back to work: paying down debt, funding reserves, or accelerating the purchase of the next property.

How Seneca Cost Segregation Can Help

For real estate investors who want an engineering-based study done right, Seneca Cost Segregation brings the credentials to back it up. With licensed professional engineers on staff, the CCSP designation from the American Society of Cost Segregation Professionals (ASCSP), and over 10,200 completed studies nationwide, Seneca delivers an average first-year deduction of $171,243—with a 95% client referral rate.

What Sets Seneca Apart

- Proprietary in-house technology built and tested for IRS compliance

- Studies completed in 2-4 weeks

- AuditDefense with a money-back guarantee—if an audit occurs and Seneca is found to be the cause of an issue resulting in a greater than 5% adjustment to depreciation, Seneca refunds 100% of the study fee

- Complimentary tax assessments beyond the cost segregation study itself

- Veteran-owned firm founded by real estate investors who use cost segregation in their own portfolios

Request a Free Assessment

Real estate investors across all 50 states can request a complimentary assessment to see exactly how much their property could generate in first-year deductions. There's no obligation—just a clear, transparent process from initial review to CPA-ready report delivery.

Contact Seneca Cost Segregation:

- Phone: +1 530-797-6539 or 503-383-1158

- Email: info@senecacostseg.com

- Address: 1210 Jackson St SE - Suite 2, Albany, OR 97322

Frequently Asked Questions

What is an engineering-based depreciation (engineered cost segregation) study and what does a cost segregation engineer do?

An engineering-based depreciation study is a formal property analysis conducted by licensed engineers who inspect the property, review construction documents, and reclassify building components into shorter IRS depreciation categories. This accelerates tax deductions in ways that accounting-based or template studies typically cannot match.

How does an engineering-based depreciation (cost segregation) study affect taxes?

The study accelerates depreciation deductions by reclassifying assets from 27.5/39-year schedules to 5, 7, or 15-year recovery periods—reducing taxable income in the early years of ownership. When combined with 100% bonus depreciation, this can generate large first-year deductions that significantly lower or eliminate federal tax liability.

How much does an engineering-based depreciation (cost segregation) study cost?

Fees vary based on property type, size, and complexity—typically a few thousand dollars for smaller residential properties and $15,000 or more for large commercial assets. Tax savings generally exceed the fee many times over, often within the first year.

Is an engineering-based depreciation (cost segregation) study worth it?

For most property owners with depreciable real estate valued at $300,000 or more, yes. An engineering-based study identifies more qualifying property than standard approaches and produces the IRS documentation needed to defend those deductions—converting decades of spread-out depreciation into front-loaded savings.

What types of properties qualify for an engineering-based cost segregation study?

Engineering-based cost segregation studies apply to multi-family apartments, commercial buildings, single-family rentals, short-term rentals, industrial facilities, and owner-occupied business properties—generally any depreciable real property used in a trade or business or held for investment.

How is an engineering-based study different from an accounting-based or DIY cost segregation study?

Engineering-based studies use licensed engineers, site inspections, and construction-level cost analysis—identifying specific qualifying components with precision. Accounting-based and DIY approaches rely on statistical averages and limited documentation, which typically produces fewer deductions and weaker audit defensibility.