Introduction

Manufacturers who own their facilities are sitting on one of the most powerful tax strategies in the tax code—yet many are still depreciating their buildings over 39 years as if no alternatives exist. This default approach leaves enormous deductions on the table at a time when legislative changes have dramatically expanded real estate tax incentives specifically for manufacturers.

The challenge is familiar: traditional 39-year depreciation does little to free up capital in the early years when reinvestment opportunities are greatest. Cash flow pressure during facility expansions or equipment upgrades is exactly where these strategies make a measurable difference.

Between the newly enacted Qualified Production Property (QPP) deduction, permanently restored 100% bonus depreciation, cost segregation, Section 179D energy deductions, and federal credits, manufacturers can now front-load hundreds of thousands of dollars in deductions in year one.

This guide breaks down each strategy manufacturers need to coordinate: cost segregation studies, QPP elections, stacked depreciation methods, energy efficiency deductions, and layered federal and state credits. Used together, they can cut taxable income on manufacturing real estate by six figures or more in a single tax year.

TLDR

- Cost segregation reclassifies 25-60% of manufacturing facility costs into 5-year and 15-year categories, unlocking 100% bonus depreciation

- The new QPP deduction allows 100% first-year expensing of production-area real property for construction starting after January 19, 2025

- Stack bonus depreciation, Section 179, and 179D energy deductions to maximize first-year tax savings

- Federal credits (R&D, WOTC, 45X, 48C) and state incentives layer on top of depreciation strategies

- Engineering-based studies protect your deductions with IRS-compliant documentation and accurate cost allocation

Why Manufacturers Miss Out on Real Estate Tax Savings

Most manufacturers default to straight-line 39-year depreciation on their facilities—technically correct, but it leaves massive deductions unclaimed. The focus typically falls on equipment and inventory tax planning, while the building itself becomes an afterthought. This oversight costs manufacturers hundreds of thousands in accelerated deductions.

Recent legislative changes have created an urgent planning window. The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, permanently restored 100% bonus depreciation for property acquired after January 19, 2025 and created the entirely new QPP deduction category. These provisions dramatically expand real estate tax incentives specifically for manufacturers—but only for those who act proactively.

Unlike equipment credits that apply automatically, real estate tax incentives require engineering-based analysis and formal elections to claim. Most manufacturers miss these savings for predictable reasons:

- No engineering study commissioned to identify reclassifiable components

- IRS documentation requirements for specialized manufacturing systems go unmet

- Formal elections are never filed because no one flags the opportunity

- CPA focus stays on equipment and inventory, not building subcomponents

Without a proactive cost segregation study, these deductions quietly expire—often representing six figures in missed first-year savings.

Cost Segregation: The Foundation of Manufacturing Facility Tax Strategy

What Cost Segregation Does

A cost segregation study is an engineering-based analysis that reclassifies components of a manufacturing building from 39-year real property into 5-year personal property and 15-year land improvements—dramatically accelerating depreciation. Instead of recovering costs over four decades, manufacturers can front-load deductions into years one through seven.

The IRS Cost Segregation Audit Techniques Guide establishes the legal framework and methodology requirements. The IRS explicitly warns against using "rule of thumb" percentages without corroborating engineering documentation—making professional studies essential for audit defense.

Components That Qualify for Reclassification

Manufacturing facilities contain substantially more reclassifiable components than standard commercial buildings. Typical manufacturing facility components that qualify include:

- Specialized electrical systems serving production equipment (5-year)

- Process piping for water, air, gas, or chemical distribution (5-year)

- Manufacturing-specific HVAC serving production areas (5-year)

- Floor drains and trench drains in production zones (15-year)

- Dock equipment including levelers and doors (5-year)

- Dedicated task lighting over assembly lines (5-year)

- Compressed air systems and distribution (5-year)

- Specialized flooring for production areas (15-year)

These components are often buried in the building's total cost basis. Industry benchmarks indicate that manufacturing facilities typically reclassify 25-60% of depreciable basis into shorter-life categories, with highly specialized production facilities—those with extensive process piping, custom electrical, or climate-controlled zones—reaching the upper end of that range.

Unlocking Bonus Depreciation

When combined with bonus depreciation, cost segregation produces substantially larger first-year deductions. Assets reclassified to 5-year or 15-year lives become eligible for 100% bonus depreciation (permanently restored by OBBBA), converting what would be slow 39-year write-offs into immediate deductions.

Example: $5M Manufacturing Facility

- Original basis: $5,000,000 (39-year depreciation = $128,205/year)

- Cost segregation reclassifies 40%: $2,000,000

- With 100% bonus depreciation on reclassified assets: $2,000,000 first-year deduction

- Remaining $3,000,000 depreciates over 39 years: $76,923/year

- Total first-year deduction: $2,076,923 (vs. $128,205 without cost segregation)

Seneca Cost Segregation's engineering-based studies are built around this methodology, with studies completed in 2-4 weeks and an average first-year deduction of $171,243 across 10,200+ properties assessed nationwide. That result holds for new acquisitions — but the same opportunity applies to facilities manufacturers already own.

Catch-Up Depreciation for Existing Facilities

Cost segregation isn't limited to new purchases. Manufacturers can use IRS Form 3115 to claim missed depreciation from prior years without amending past returns. The Section 481(a) adjustment allows the entire catch-up amount as a single-year deduction, applying the rules in effect when the property was placed in service.

This means a manufacturer who purchased their facility five years ago can conduct a cost segregation study today and claim all five years of missed accelerated depreciation in the current tax year.

The New Qualified Production Property (QPP) Deduction

100% Immediate Deduction for Production Buildings

The OBBBA introduced a new category — IRC Section 168(n) Qualified Production Property — allowing 100% first-year expensing for nonresidential real property used as an integral part of a qualified production activity. Instead of depreciating production buildings over 39 years, manufacturers can expense the qualifying portion in year one.

What Qualifies as Production Activity

QPP applies to strict categories of substantial transformation:

Qualifying activities:

- Manufacturing tangible personal property

- Chemical production requiring material transformation

- Agricultural production and processing

- Petroleum refining

Non-qualifying activities:

- Packaging and labeling without material alteration

- Minor assembly operations

- Warehousing and distribution

- Software development

The key test: does the activity materially convert raw materials into a distinct final product? Activities that merely prepare, package, or distribute existing products don't meet the substantial transformation threshold.

Building Areas That Qualify

QPP covers real property components in production areas:

- Structural walls and foundations

- General lighting systems

- HVAC serving production spaces

- Plumbing and utilities in manufacturing zones

- Insulation and roofing over production areas

- Concrete slabs in production zones

Excluded areas that must be isolated:

- Office and administrative spaces

- Sales and showroom areas

- Research and development labs

- Finished-goods storage warehouses

- Employee parking and break areas

Without proper basis allocation, any IRS challenge to space usage becomes difficult to defend. Cost segregation studies provide the documentation framework to separate qualifying production space from excluded areas, establishing audit-defensible square footage allocations.

Timing Requirements and Ownership Rules

Construction timeline:

- Construction must begin after January 19, 2025 and before January 1, 2029

- Property must be placed in service before January 1, 2031

The taxpayer claiming QPP must be the entity conducting the qualified production activity — not a separate landlord or lessor. Leasing arrangements generally disqualify the deduction, though IRS Notice 2026-16 provides exceptions for related-party leases where both parties share 50% or more common ownership.

10-Year Recapture Risk

QPP carries a significant compliance requirement: if the property ceases to be used for qualifying production within 10 years of being placed in service, the entire depreciation claimed is recaptured as ordinary income under IRC Section 1245.

This makes QPP elections best suited for manufacturers with stable, long-term operational plans. Because recapture exposure extends a full decade, thorough documentation from the start matters — cost segregation studies play a key role in establishing basis allocation and providing audit defensibility if the IRS questions space usage or activity qualification.

Stacking Tax Strategies: Bonus Depreciation, Section 179, and 179D

100% Bonus Depreciation—Permanently Restored

The OBBBA permanently restored 100% bonus depreciation for qualified property acquired after January 19, 2025, replacing the TCJA phase-down schedule that would have reduced it to 40% in 2025.

When combined with cost segregation, manufacturers can take 100% first-year deductions on all assets reclassified to 5-year or 15-year lives. This applies to:

- Personal property integral to manufacturing

- Land improvements (Asset Class 00.3)

- Qualified improvement property

Section 179 Expensing

Section 179 allows immediate expensing of qualifying equipment, machinery, and certain building improvements in the year placed in service. For 2025, the maximum deduction is $2,500,000, with a phase-out threshold beginning at $4,000,000. For 2026, the limit increases to $2,560,000 with a $4,090,000 phase-out.

Section 179 works particularly well for:

- Manufacturing equipment and machinery

- Office furniture and computers

- Vehicles used in the business

- Qualified improvement property

Unlike bonus depreciation, Section 179 requires active business income to offset—it cannot create a loss. Manufacturers with substantial equipment purchases often use Section 179 first, then apply bonus depreciation to remaining assets.

Once equipment costs are handled through Section 179, the focus shifts to the building itself—where 179D adds another layer of deductions.

Section 179D Energy-Efficiency Deduction

The 179D deduction rewards manufacturing buildings that meet energy efficiency standards for HVAC, interior lighting, and building envelope. The Inflation Reduction Act significantly increased the maximum deduction:

2025 rates:

- Base rate: $1.16 per square foot

- With prevailing wage and apprenticeship (PWA): $5.81 per square foot

2026 rates:

- Base rate: $1.19 per square foot

- With PWA: $5.95 per square foot

OBBBA terminated the 179D deduction for property where construction begins after June 30, 2026. Manufacturers planning facility expansions or energy upgrades should accelerate projects to capture this benefit. The Inflation Reduction Act also allows recurring claims for phased projects—manufacturers can claim 179D for each distinct improvement meeting the energy efficiency threshold, making it worth revisiting after each project phase.

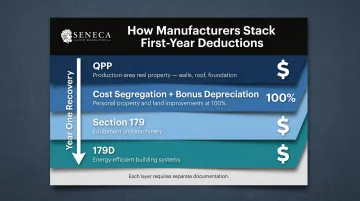

How the Strategies Stack

Combined, these four strategies can cover nearly every dollar spent on a new facility:

- QPP covers production-area real property (walls, roof, foundation)

- Cost segregation separates personal property and land improvements for bonus depreciation

- Section 179 covers equipment and machinery

- 179D covers energy-efficient building systems

Together, these strategies let manufacturers recover most of a new facility's cost in year one. Each requires its own documentation—cost segregation studies, energy certifications, and proper basis allocation—so coordination between your engineer and CPA matters as much as the strategies themselves.

Federal and State Credits to Layer on Top

Federal Manufacturing Credits

Beyond depreciation strategies, manufacturers should evaluate these federal tax credits:

R&D Tax Credit (Section 41): The R&D credit rewards qualified research expenses including wages and supplies for discovering technological information. For manufacturers, this includes:

- Process improvements and efficiency testing

- Prototype development and material testing

- Laboratory analysis and quality control innovation

- Manufacturing automation development

Activities like quality control testing or automation development often qualify — even when manufacturers don't label them as "research."

Work Opportunity Tax Credit (WOTC): Extended through December 31, 2025, WOTC covers 40% of first-year wages — up to $2,400 per employee for most targeted groups. Manufacturers hiring qualified veterans can claim up to $9,600 per hire. This credit stacks with other federal incentives, making it particularly valuable when layered into a broader tax strategy.

Section 45X Advanced Manufacturing Production Credit: For manufacturers producing clean energy components, Section 45X provides production tax credits:

- Solar modules: $0.07 per Wdc capacity

- Battery cells: $35 per kWh capacity

- Electrode active materials: 10% of production costs

- Applicable critical minerals: 10% of production costs

Section 48C Advanced Energy Project Investment Credit: The IRS allocated $10 billion for Section 48C, with projects meeting prevailing wage and apprenticeship standards receiving 30% investment tax credits. This applies to manufacturing facilities producing renewable energy equipment or significantly improving energy efficiency.

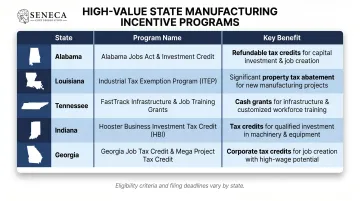

State-Level Manufacturing Incentives

Federal credits cover a lot of ground, but state programs add another layer — often targeting job creation, capital investment, or property tax relief specific to your location. Combined with federal credits, the right state program can meaningfully shift a project's total tax liability:

High-value state programs:

| State | Program | Benefit |

|---|---|---|

| Alabama | Investment Credit | Up to 1.5% annually of qualified capital investment for up to 10 years |

| Louisiana | Industrial Tax Exemption | 80% property tax abatement for up to 10 years on new manufacturing investments |

| Tennessee | Job Tax Credit | $4,500 per job; requires $500,000 investment and 10-25 jobs |

| Indiana | EDGE Credits | Refundable payroll credit up to 20 years |

| Georgia | Manufacturing Exemptions | Sales/use tax exemptions for machinery and energy |

Each credit listed above has its own eligibility criteria, documentation requirements, and filing deadlines. Coordinating state claims with federal elections — particularly bonus depreciation — prevents conflicts that can limit the value of either benefit. A tax advisor familiar with both levels of incentives is essential to capturing the full stack without leaving credits on the table.

How to Build a Complete Manufacturing Tax Plan

The Coordinated Approach

Maximizing manufacturer tax incentives requires orchestrating multiple strategies in the correct sequence:

Step 1: Start with cost segregation Establish proper basis allocation between real property, personal property, and land improvements. This creates the foundation for all subsequent elections and separates qualifying production areas from excluded spaces.

Step 2: Evaluate QPP eligibility For facilities where construction began after January 19, 2025, determine which building areas qualify as integral to qualified production activities. Document the basis allocation between production and non-production spaces.

Step 3: Apply bonus depreciation and Section 179 Layer 100% bonus depreciation on reclassified 5-year and 15-year property from the cost segregation study. Use Section 179 for equipment and machinery purchases, staying within annual limits.

Step 4: Claim 179D for energy efficiency If facility improvements meet energy efficiency thresholds, claim the 179D deduction—but remember construction must begin before June 30, 2026.

Step 5: Stack applicable credits Evaluate R&D, WOTC, 45X, 48C, and state-level incentives. Coordinate filing to ensure credits don't conflict with depreciation elections.

Timing Is Critical

Each strategy has specific timing requirements:

- QPP elections are made on a timely filed return and are generally irrevocable

- Bonus depreciation must be elected in the year assets are placed in service

- 179D requires energy analysis documentation completed before filing

- State incentive applications often have pre-project filing requirements

Missing deadlines or filing out of sequence can disqualify otherwise valuable deductions. Professional coordination between cost segregation engineers, CPAs, and tax advisors keeps each strategy on track and compliant.

Getting a Full Incentive Assessment

Given how many moving parts are involved, a coordinated review of your facility's tax position is often the clearest starting point. Seneca Cost Segregation offers complimentary tax assessments that go beyond cost segregation—helping manufacturing facility owners identify which incentives apply, in what order, and how they interact. Seneca's engineering-based team works directly with your CPA across all 50 states, with studies typically completed in 2-4 weeks and backed by AuditDefense and a money-back guarantee.

Frequently Asked Questions

Frequently Asked Questions

Can you deduct 100% for construction of manufacturing buildings?

Yes. Under the OBBBA's QPP deduction, manufacturers may deduct 100% of qualifying production-related real property costs in the year placed in service, provided requirements around property use, ownership, and timing are satisfied. Cost segregation properly allocates basis between qualifying production areas and excluded spaces like offices.

What is the new $6,000 tax credit?

The most commonly referenced $6,000 figure relates to the Work Opportunity Tax Credit (WOTC), where the maximum wage base is $6,000 per employee. The actual credit is 40% of those wages, yielding a maximum $2,400 per qualifying employee hired from targeted groups, not $6,000.

Does cost segregation still make sense if I qualify for the QPP deduction?

Yes—cost segregation is more important with QPP, not less. It separates personal property (eligible for bonus depreciation) from real property (eligible for QPP), allocates basis correctly between production areas and excluded spaces, and creates the documentation required for audit defense.

What qualifies as a "substantial transformation" under QPP rules?

Substantial transformation means the manufacturing activity must materially convert raw materials into a distinct final product. Full manufacturing, chemical production, refining, and agricultural processing typically qualify. Packaging, labeling, or minor assembly that doesn't materially alter inputs does not qualify.

Can I claim the QPP deduction on a property I lease rather than own?

Generally no. The OBBBA requires the taxpayer claiming QPP to be the one conducting the qualified production activity, and the law explicitly excludes lessors. Limited exceptions apply to certain related-party lease arrangements with 50% or more common ownership.

How far back can I apply cost segregation on an existing manufacturing facility?

There is no time limit. Using IRS Form 3115, manufacturers can claim a catch-up deduction in the current year for all missed depreciation from prior years, without amending prior returns. The Section 481(a) adjustment governs how those corrections are calculated.