Introduction

Commercial property owners significantly overpay on property taxes each year. According to the National Taxpayers Union Foundation, between 30 and 60 percent of taxable property in the United States is over-assessed. Yet fewer than 5 percent of taxpayers challenge their assessments, even though most who appeal win at least partial relief.

This overpayment directly erodes net operating income, compresses margins, strains cash flow, and delays reinvestment into additional properties. That's capital sitting with the county instead of working for you.

None of this is inevitable. Taxes become excessive primarily due to unchallenged assessments, missed exemptions, and lack of strategic planning. This article covers a three-pronged reduction framework: decisions made during assessment, ongoing management and documentation practices, and structural changes around how properties are owned and financed.

TL;DR

- Property tax bills grow through reassessments, rising market values, and construction cost inflation — often faster than owners realize

- The biggest cost drivers are inaccurate mass appraisals, missed appeal deadlines, and poor income documentation

- Three core strategies cut exposure: pre-assessment planning, consistent documentation, and ownership structure

- Federal tax strategies like cost segregation accelerate depreciation deductions and offset total ownership costs

- Reviewing your assessment every cycle — not just when bills spike — produces the most durable savings

How Commercial Property Tax Bills Accumulate Over Time

Commercial property taxes compound over reassessment cycles as market values rise, replacement costs increase, and assessors apply updated income assumptions. According to Mortenson's Cost Index, construction costs increased 7.35% year-over-year in Q4 2025, while Turner's Building Cost Index showed a 4.72% annual increase. These rising replacement costs directly increase assessed values through the cost approach.

Those rising cost benchmarks feed directly into assessments — yet the exposure builds quietly between cycles. Most property owners don't realize how much their tax liability has grown until a reassessment notice lands. Several factors make accumulation easy to miss:

- Multi-year reassessment schedules delay the impact, then deliver it all at once

- Market value increases compound on top of prior assessed values

- Income assumptions used by assessors often lag actual market conditions

- Owners without recent appraisals lack a benchmark to challenge the new figure

Because assessors use mass appraisal methodology rather than individual property appraisals, errors and inflated values stay locked in for years unless owners challenge them. The International Association of Assessing Officers notes that valuation accuracy depends first on completeness and accuracy of property data—when this data is wrong, systematic overassessment follows.

Key Drivers Behind High Commercial Property Tax Assessments

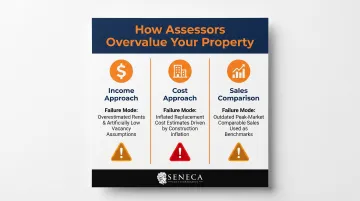

The Three Valuation Approaches

Assessors use three primary methods, each prone to producing inflated results:

- Income approach - Overestimates market rents or assumes unrealistically low vacancy rates

- Cost approach - Relies on inflated replacement cost estimates driven by construction inflation

- Sales comparison approach - Uses peak-market comparable sales that no longer reflect current conditions

Structural Factors Driving Assessments Higher

Post-pandemic corrections have reshaped commercial real estate values unevenly. Cushman & Wakefield reported office vacancy at 20.2% in Q1 2026, while CoStar projects industrial vacancy rising to 7.8% by year-end 2026. These fundamentals often lag behind assessor assumptions by months or years.

Meanwhile, construction cost inflation keeps pushing replacement value estimates higher regardless of actual income performance. Local tax levy requirements compound the problem — effective tax rates can rise even when property values stay flat.

Property Type Variations

These macro pressures don't hit all property types equally — cost drivers vary significantly by asset class and jurisdiction. The Lincoln Institute of Land Policy found the effective tax rate on commercial properties worth $1 million averaged 1.836% across major cities in 2022. Detroit and Chicago posted the highest rates. Knowing which valuation method produced your assessment — and where its assumptions broke down — tells you exactly where to focus your appeal.

Strategies to Reduce Commercial Property Taxes

Tax reduction strategies vary depending on whether the problem originates in assessment calculation, property management and documentation, or ownership structure and tax environment.

Strategies That Reduce Costs by Changing Decisions

These approaches lower your tax burden by altering decisions at or before assessment.

Challenge the assessment through formal appeal

The IAAO explains that appeal processes follow hierarchical steps: local assessor or review board first, then higher-level tribunals, and finally courts. Deadlines are short and unforgiving—often 30 days from notice. Most owners miss the window entirely by failing to track proactively.

Typical deadlines include:

- Texas: May 15 or 30 days from notice delivery

- Florida: 25 days from mailing date

- Arizona: 60 days from notice mail date

- Ohio: March 31 in most counties (some extend to May 31)

Review assessor records for factual errors

Assessor records frequently contain errors — wrong square footage, misclassified property use, inaccurate condition ratings, or incorrect occupancy assumptions. Property-Tax.com identifies these as among the most common sources of inflated assessments, and correcting them is often the fastest path to reduction.

Many jurisdictions provide free online access to assessment data. Review your property card annually and request corrections immediately when errors appear.

Build a data-driven income-approach challenge

Commercial assessments often rely on idealized rent and occupancy assumptions. Property-Tax.com explains that owners can counter with actual rent rolls, lease agreements, documented vacancy rates, and real operating expenses showing true income generation. This approach works best when your property underperforms market assumptions due to tenant mix, deferred maintenance, or location factors.

Commission a professional appraisal before appealing

A USPAP-compliant third-party appraisal using accurate comparables and actual income data significantly strengthens appeals and shifts the burden of proof toward the assessor. While appraisals cost $3,000-$10,000, they often deliver multiples of that value in annual tax savings.

Strategies That Reduce Costs by Changing How the Property Is Managed

These approaches reduce tax burden by improving visibility, documentation, and ongoing compliance.

Track and document property performance data continuously

Owners who maintain up-to-date records of actual income, vacancy, operating expenses, and deferred maintenance challenge assessments quickly and effectively. Those who reconstruct records at appeal time face credibility challenges and tight deadlines.

Maintain organized files for:

- Monthly rent rolls and collections

- Lease agreements with escalation clauses

- Operating expense statements

- Capital improvement records

- Vacancy and tenant turnover data

Monitor reassessment cycles and calendar all deadlines proactively

Each jurisdiction has its own reassessment schedule and appeal window. Missing a single deadline locks in inflated values for years. The IAAO Standard notes that while annual assessment is common, individual property data is typically reviewed every 4-6 years — making proactive tracking essential.

Create a master calendar tracking reassessment dates and appeal deadlines across your entire portfolio.

Apply for all eligible exemptions, abatements, and incentive programs

Many jurisdictions offer exemptions or temporary abatements for specific uses:

- Agricultural exemptions

- Nonprofit qualifications

- Green building incentives

- Historic preservation benefits

- Enterprise zone abatements

- Opportunity zone benefits

These programs are rarely applied automatically—you must file separately and meet ongoing compliance requirements.

Deduct commercial property taxes as a business expense

Per IRS Publication 535, property taxes on commercial real estate used for business purposes are generally deductible in the year paid. This reduces federal taxable income even when the local assessment cannot be reduced. The deduction applies to state, local, and foreign taxes directly attributable to your trade or business.

Strategies That Reduce Costs by Changing the Context Around the Property

These approaches reduce total tax cost by addressing external structure, use, and financing environment.

Structure leases to pass property tax obligations to tenants

Triple-net (NNN) leases require tenants to pay property taxes directly or as part of operating expenses, shifting the burden away from the owner and making net returns more predictable. CBRE reported that NNN investment volume reached $16.0 billion in Q4 2025, up 38% quarter-over-quarter, with industrial and logistics accounting for 55% of activity.

NNN leases transfer reassessment risk to tenants while stabilizing ownership cash flows.

Evaluate property disposition or use changes if tax burden is structurally unsustainable

When assessed value consistently outpaces actual income potential, evaluate whether converting, repositioning, or divesting makes more financial sense than continuing to pay inflated taxes. This is especially relevant for office properties facing structural vacancy challenges in post-pandemic markets.

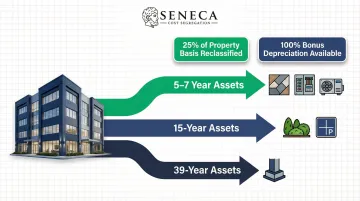

Use cost segregation to reduce federal income tax burden

Cost segregation doesn't reduce local property tax assessments, but it significantly cuts federal income taxes by front-loading depreciation deductions. The IRS Cost Segregation Audit Techniques Guide explains that reclassifying building components from 39-year schedules to 5-, 7-, or 15-year schedules can turn 20-40% or more of property costs into immediate deductions. Eligible components include HVAC systems, electrical, flooring, and landscaping.

According to the American Society of Cost Segregation Professionals, typical studies reclassify approximately 25% of property basis into shorter-lived asset categories. With 100% bonus depreciation restored under the One Big Beautiful Bill Act for property placed in service after January 19, 2025, this creates substantial first-year deductions.

Firms like Seneca Cost Segregation complete engineering-based studies across all 50 states, with an average first-year deduction of $171,243 and a 2-4 week turnaround. Used alongside local tax appeals and lease structuring, cost segregation compounds total tax savings across both federal and local obligations.

Explore tax incentive zones and local economic development programs

Certain jurisdictions offer long-term property tax abatements or reduced assessments for properties in designated zones:

- Texas: Tax abatements exempt increases in property value from taxation for up to 10 years

- Ohio: Enterprise Zone Program provides real and personal property tax exemptions

- New York: PILOT agreements replace property taxes with negotiated payments

IRS Qualified Opportunity Zones provide federal income tax deferrals and exclusions when combined with local municipal abatements. These programs can provide multi-year relief that far exceeds what a single appeal achieves.

Conclusion

Reducing commercial property taxes starts with identifying where you're overpaying—whether that's in the assessor's assumptions, your documentation habits, or the broader tax structure around your property.

The most effective approach is proactive and layered. Stack these strategies together for the greatest impact:

- File annual appeals with current market data and accurate property records

- Claim all eligible business deductions tied to your property

- Structure leases to shift appropriate tax burdens to tenants

- Use cost segregation to accelerate federal depreciation and reduce taxable income

Start with the area where you have the clearest evidence of overpayment, then build from there. A cost segregation study, in particular, often delivers the largest first-year savings—and the findings can inform your depreciation strategy for years to come.

Frequently Asked Questions

How can I reduce commercial property taxes?

Challenge the assessment through formal appeal, correct factual errors in assessor records, apply for available exemptions, and use business deductions. The most effective approach combines multiple strategies across the same ownership cycle.

Can I write off commercial property taxes as a business expense?

Yes. Per IRS Publication 535, property taxes on commercial real estate used for business purposes are generally deductible in the year paid, reducing federal taxable income. Specifics depend on how the property is used and owned.

How do I appeal a commercial property tax assessment?

- Review the assessment notice immediately upon receipt.

- File an appeal with the local assessor or Board of Review before the deadline — often 30 days.

- Support your case with comparable sales data, income and expense records, and a professional appraisal if needed.

What is cost segregation and how does it reduce taxes?

Cost segregation is an engineering-based, IRS-compliant study that reclassifies property components into shorter depreciation schedules, generating large front-loaded deductions that reduce federal income taxes owed on commercial property.

How often are commercial properties reassessed for property taxes?

Reassessment cycles vary by jurisdiction—some counties assess annually, others every 2-4 years. Track your local cycle to ensure you review each new assessment promptly and never miss the appeal window.

What exemptions can reduce commercial property taxes?

Available exemptions vary by state and municipality. Common options include:

- Enterprise zone abatements

- Historic preservation exemptions

- Green building incentives

- Opportunity zone benefits

- Nonprofit or agricultural use exemptions

None are applied automatically. You must actively apply for each one.