Introduction

American property owners collectively paid $729 billion in state and local property taxes in FY2023, and businesses alone shouldered $394.3 billion of that, or 54.1% of all collections. If you own investment or commercial real estate, that bill rises automatically as property values climb, often without any action on your part to justify the increase.

The mechanism is straightforward: when nearby properties sell at higher prices, assessors raise valuations across entire neighborhoods. Multi-family and commercial properties face even steeper climbs. Effective tax rates in some markets run nearly 4 times higher than residential homesteads.

Many owners overpay for years simply because they accept the assessment without question.

This guide covers the most effective ways to reduce your property tax burden, from challenging your assessment to structuring acquisitions with tax exposure in mind.

TL;DR

- Property taxes recalculate using assessed value and local mill rate; errors in either cause overpayment

- Target assessed value directly through error correction, exemptions, comparable sales analysis, and formal appeals

- Proactive decisions before assessment (exemption applications, improvement timing) outperform reactive measures

- Commercial and income-producing properties often carry disproportionate tax burdens, but income-based valuation arguments can push assessments lower

- Property tax reduction can be paired with cost segregation to address both assessed value and federal tax liability simultaneously

How Property Tax Costs Typically Build Up

Property taxes are not fixed; they recalculate as assessed values change, typically tied to market appreciation cycles. In many jurisdictions, your bill rises automatically as nearby property values climb, even when you've made no improvements to your own property.

This cost build-up is gradual and easy to miss. Most owners rarely scrutinize annual bills until a large reassessment arrives, by which point multiple years of overpayment may have already occurred.

Several mechanics drive the accumulation:

- Small annual percentage increases compound quietly over time

- Property taxes are paid in arrears, meaning you're often paying on last year's inflated assessment

- Reassessment cycles can trigger sudden spikes after years of understated values

Commercial and investment property owners feel this pressure most acutely. Multi-family and commercial properties are assessed at higher effective rates than primary residences. Nationwide, businesses pay 56% of property tax revenue despite representing a smaller share of assessed valuation. Municipalities rely disproportionately on commercial tax revenue to fund local services, creating a structural penalty that shifts the burden away from homeowners.

What Drives Your Property Tax Bill

Your annual property tax bill follows a simple formula: assessed value × mill rate = tax bill. While the mill rate is outside your control (set by local governments to fund budgets), the assessed value is the primary lever available to property owners.

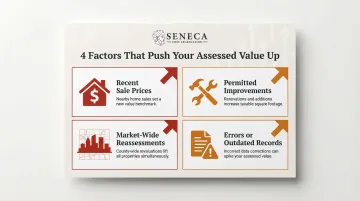

Four factors push assessed values up:

| Factor | How It Increases Assessed Value |

|---|---|

| Recent sale prices in your area | Assessors use comparable sales to estimate your property's market value |

| Permitted improvements and additions | Structural additions, new fixtures, and permitted construction trigger reassessment |

| Market-wide reassessments | Scheduled mass revaluations can create sudden spikes across entire jurisdictions |

| Errors or outdated records | Incorrect square footage, room counts, or property classifications that inflate value |

Not all of these factors reflect your property's true current condition or income performance. IAAO mass appraisal standards tolerate up to 5% error rates in property data, and real-world failures are costly. A 2024 audit of Cook County, Illinois revealed 620 misclassified properties missing $444 million in value in a single year.

Those error risks aren't evenly distributed. Residential owners are primarily affected by market comps and permitted improvements. Commercial and investment property owners face additional complexity: income performance records, capitalization rate assumptions, and classification errors that can dramatically change taxable value.

Property Tax Reduction Strategies

Effective strategies vary depending on whether you focus on the information the assessor starts with, how the assessment is conducted and reviewed, or the broader ownership and tax planning context around your property.

Strategies That Lower Property Taxes by Changing Decisions

These approaches reduce property taxes by altering what information enters the assessment process and when, including decisions you make before or around an assessment that have the greatest long-term impact.

Request and Audit Your Property Tax Card

Most assessors maintain a property record card documenting lot size, room counts, dimensions, fixtures, and improvements. Errors in this document are common and go uncorrected unless you identify and challenge them.

How to obtain and review your property card:

- Visit your local assessor's website (most jurisdictions provide online access)

- Request a copy in person or by phone if online access isn't available

- Review every detail: square footage, year built, room counts, bathroom counts, garage size, basement finish

What to look for:

| Error Type | Details |

|---|---|

| Square footage errors | Measure your property and compare to the record |

| Incorrect room counts | Verify bedrooms, bathrooms, and finished spaces |

| Outdated improvements | Old renovations recorded as current features |

| Classification errors | Residential property coded as commercial (or vice versa) |

Even small errors compound over years. A 200-square-foot discrepancy on a $200-per-square-foot property inflates your assessed value by $40,000.

Apply for Every Applicable Exemption Before Assessment Season

Homestead exemptions, senior citizen exemptions, veteran exemptions, disability exemptions, and agricultural exemptions can reduce your taxable value or direct tax bill significantly. Many eligible owners fail to apply simply because they don't know they qualify.

Common exemption categories:

| Exemption Type | Description |

|---|---|

| Homestead exemptions | Reduce assessed value for primary residences |

| Senior citizen exemptions | Age-based reductions (typically 65+) |

| Veteran exemptions | Service-based reductions or full exemptions |

| Disability exemptions | Reductions for qualifying disabilities |

| Agricultural exemptions | Reduced rates for working farmland |

Check your local assessor's office website for specific eligibility requirements and application deadlines. Most exemptions require annual renewal, and missing a deadline means paying full freight for another year.

Time Property Improvements with Assessment Cycles in Mind

Structural additions, new fixtures, and permitted improvements trigger reassessment and raise taxable value. Understanding your local assessment calendar helps you schedule visible work strategically.

Practical timing strategies:

- Contact local building and tax departments before construction to understand assessed value impact

- Schedule visible cosmetic work (exterior painting, landscaping) after the assessor's annual visit

- Complete major renovations early in the assessment cycle (if your jurisdiction reassesses every 5-10 years)

- Understand which improvements require permits and which don't

This doesn't mean avoiding improvements; it means making informed decisions about timing and understanding the tax implications before you commit.

Strategies That Lower Property Taxes Through Active Management

These approaches reduce property taxes by improving how the assessment itself is conducted or challenged, through oversight and process controls available during and after the assessment.

Compare Your Assessment to Comparable Properties

Local governments often make assessment data publicly available. Pull comps for similar properties in your area and look for discrepancies where your assessed value is higher than comparable homes or buildings with more features.

How to conduct a comparable analysis:

- Access your county's property assessment database online

- Identify 3-5 properties similar in size, age, condition, and location

- Compare assessed values per square foot

- Document properties with higher values but fewer features (smaller lot, no garage, older construction)

- Compile this evidence for a conversation with the assessor

If your property is assessed at $350,000 but three comparable properties down the street are assessed at $310,000-$320,000, you have grounds for a reduction request.

Guide the Assessor Through the Property Personally

Assessors who walk a property alone may record only upgraded elements (new counters, fireplace, renovated bathroom) while missing deficiencies like aging HVAC, cracked foundation, or outdated appliances.

Why personal walkthroughs matter:

- You control which features the assessor sees and documents

- You can point out deferred maintenance and functional obsolescence

- You provide context about problems not visible from the exterior

- You establish a professional relationship that may lead to informal adjustments

Walking through with the assessor and clearly pointing out problems can result in a materially lower valuation. IAAO standards recommend physical property reviews every 4-6 years, but many assessors rely on exterior-only inspections.

File a Formal Appeal if the Assessment is Inaccurate

If informal conversations don't resolve discrepancies, formal appeals are highly viable. Cook County, Illinois reported a 50.45% reduction rate for taxpayer-filed appeals in 2023, and Iowa's Property Assessment Appeal Board achieved roughly 35% success rates from 2019-2023.

| Jurisdiction | Success/Reduction Rate | Period |

|---|---|---|

| Cook County, Illinois | 50.45% reduction rate | 2023 |

| Iowa Property Assessment Appeal Board | Roughly 35% success rate | 2019–2023 |

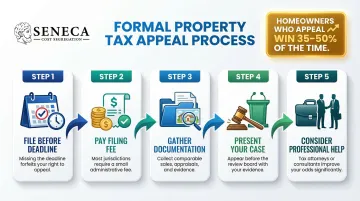

The appeal process at a high level:

- File before the deadline - Most jurisdictions have strict annual deadlines (often 30-60 days after assessment notices)

- Pay the filing fee - Typically $25-$100 depending on jurisdiction

- Gather documentation - Photos showing condition issues, comparable sales data, income/expense statements for commercial properties

- Present your case - Appear before the local appeal board or submit written evidence

- Consider professional help - Attorneys or tax consultants can strengthen complex appeals

A successful appeal lowers the assessed value, which reduces your bill. Note that appeals could result in no change or, rarely, an increase if the assessor discovers unreported improvements.

Strategies That Lower Property Taxes by Changing the Context

These approaches reduce property taxes by addressing how the property is positioned within the broader valuation system, including ownership structure, property classification, income documentation, and how property tax strategies fit within a larger tax plan.

Use Income-Based Valuation Evidence for Commercial Properties

Many jurisdictions allow commercial property values to be assessed using income capitalization methods rather than purely market comparables. The IAAO explicitly endorses the income approach as the preferred valuation method for commercial and multifamily properties when reliable income and expense data are available.

How to leverage income-based valuation:

- Document actual rental income with signed leases and rent rolls

- Track vacancy rates and operating expenses meticulously

- Prepare normalized operating statements showing true economic performance

- Challenge cost-approach or sales-comparison valuations that overstate market value

Owners who document that actual income performance is lower than the assessor's assumptions can argue for reduced assessed values that reflect true economic performance rather than inflated market estimates.

Monitor Local Reassessment Schedules and Mill Rate Changes

Municipal budgets drive mill rates, and scheduled mass reassessments can create sudden spikes. Jurisdictions conduct mass reassessments on varying statutory cycles:

| State | Reassessment Cycle |

|---|---|

| Connecticut | Every 10 years |

| North Carolina | Every 8 years |

| Oregon | Every 6 years |

| New Jersey | Every 5 years |

Property owners who track their jurisdiction's reassessment calendar, appeal filing deadlines, and recent tentative roll publications can act before bills are finalized rather than reacting after. Acquiring a property in year 1 of a 10-year cycle carries vastly different tax risk than acquiring in year 9.

Layer Property Tax Reduction with Federal Income Tax Strategies

Reducing your assessed value lowers the local bill, but the federal side of the equation offers equally significant leverage. Real estate investors can stack additional savings at the federal level by pairing assessment management with accelerated depreciation strategies.

A cost segregation study reclassifies components of a property to shorter depreciation schedules, generating front-loaded deductions that can reduce or eliminate federal income tax liability in the first year. That freed-up cash can offset property tax payments or fund the next acquisition.

Seneca Cost Segregation has completed over 10,200 engineering-based studies, with an average first-year deduction of $171,243. For commercial and investment property owners carrying disproportionate tax burdens, addressing both local assessments and federal depreciation in the same year produces the most immediate financial impact.

Conclusion

Reducing property tax costs depends on identifying where the cost originates. Most owners overpay not because property taxes are unavoidable, but because they accept assessed values, miss exemptions, or never challenge inaccuracies that are well within their right to dispute.

The best outcomes come from owners who treat their property tax bill as a managed expense, one that responds to documentation, proactive filing, timely appeals, and a broader strategy covering both local and federal obligations. Property tax savings rarely happen by accident; they happen because someone reviewed the assessment and acted on what they found.

Auditing the property card, applying for exemptions, and comparing the assessment to nearby sales are three steps that alone routinely surface significant annual savings, and for investment property owners, pairing that effort with a federal depreciation strategy can compound the impact further.

Frequently Asked Questions

What is the best way to lower property taxes?

The most impactful first step is reviewing your property tax card for errors in assessed value, followed by checking exemption eligibility and comparing your assessment to similar nearby properties. If discrepancies exist, file a formal appeal with supporting documentation before the jurisdiction's annual deadline.

How does the new $6,000 tax deduction work?

The "$6,000 deduction" is an additional standard deduction for seniors aged 65 and older under the One, Big, Beautiful Bill Act (P.L. 119-21), effective for tax years 2025-2028. This is an age-based income reduction, not a property tax deduction. It does not alter SALT deduction limits or property tax deductibility rules.

Can you appeal your property tax assessment, and how does it work?

Yes. File an appeal with your local tax authority before the annual deadline, supported by comparable sales data, property condition photos, and income data for commercial properties. Success rates in documented jurisdictions often exceed 35-50%.

What exemptions can lower my property tax bill?

Common categories include homestead, senior citizen (65+), veteran, disability, and agricultural exemptions. Eligibility and savings amounts vary by state and municipality — check with your local assessor's office to confirm what applies to you.

Do investment and commercial property owners pay higher property taxes than homeowners?

Yes. Commercial and multi-family properties are typically assessed at higher effective rates and receive fewer protective exemptions than primary residences. In some markets, commercial rates reach nearly 4 times higher than homestead rates, making proactive assessment reviews and appeals especially important for investors.

How often are property tax assessments updated?

Reassessment frequency varies by jurisdiction; some reassess annually, others every 5-10 years depending on state law. Market-wide reassessments often create sudden spikes in assessed values, making it important for property owners to monitor their local reassessment calendar and act before filing deadlines close.