Introduction

Many residential rental property owners assume cost segregation is strictly a commercial real estate tool. That assumption is costing them real money. Investors who skip it often leave $50,000 or more in first-year deductions on the table.

Under standard IRS rules, residential rental properties depreciate over 27.5 years, spreading deductions thin across decades when cash flow matters most. Cost segregation changes that by accelerating depreciation on specific components.

This guide covers:

- What cost segregation means for residential rentals

- How the study process works, step by step

- Which components typically qualify

- What factors shape your results

- When it may not be the right move

TLDR

- Cost segregation applies to single-family rentals, multi-family units, and short-term rentals, not just commercial buildings

- Reclassifies property components from 27.5-year schedules to accelerated 5-, 7-, or 15-year schedules

- Front-loaded deductions improve cash flow and free up capital for reinvestment sooner

- Look-back studies let you claim catch-up deductions on properties acquired as far back as 1987

- A formal engineering study ensures IRS-defensible results and audit protection

What Is Cost Segregation for Residential Rental Property?

Cost segregation is a tax strategy that breaks a residential rental property into its individual components and assigns each component to the depreciation schedule that legally applies to it, often much shorter than 27.5 years.

By default, the IRS treats a residential rental property as a single asset depreciating over 27.5 years (39 years for commercial). That approach ignores components that legally qualify for faster write-offs.

Under the Modified Accelerated Cost Recovery System (MACRS), cost segregation reallocates building costs into shorter-lived asset categories:

| Asset Category | Depreciation Period | Examples |

|---|---|---|

| Personal Property | 5 years | Carpeting, appliances, and certain fixtures |

| Personal Property | 7 years | Office furniture and select equipment |

| Land Improvements | 15 years | Parking lots, sidewalks, and landscaping |

| Structural Components | 27.5 years | The structural shell and core building components |

Important boundary: Cost segregation applies exclusively to income-producing investment properties. It cannot be used on a personal primary residence. Any residential rental, including single-family, multi-family, or short-term rental properties, qualifies as long as it generates rental income.

Why Residential Rental Property Owners Use Cost Segregation

Front-Loading Tax Deductions When You Need Them Most

By accelerating depreciation into the early years of ownership, investors reduce their taxable income precisely when operating costs (repairs, mortgage interest, management fees) are typically highest. This compresses the tax burden at the most financially demanding time.

Lower tax liability in early ownership years frees up capital that can be deployed into property improvements, debt reduction, or acquisition of additional properties.

According to the IRS Cost Segregation Audit Techniques Guide, properly conducted studies identify components that legally qualify for 5-, 7-, or 15-year depreciation schedules, generating much larger deductions than straight-line 27.5-year depreciation.

Bonus Depreciation as a Multiplier

Components reclassified to 5- or 7-year schedules may also qualify for bonus depreciation, which allows an immediate percentage write-off in the year the study is completed. The One Big Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively. For rental property owners, that matters because the 27.5-year building structure itself is ineligible for bonus depreciation, but the shorter-life components identified during a study are fully eligible.

Bonus Depreciation Timeline:

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | TCJA full bonus depreciation |

| January 1, 2023 – December 31, 2023 | 80% | TCJA phase-down |

| January 1, 2024 – December 31, 2024 | 60% | TCJA phase-down |

| January 1, 2025 – January 18, 2025 | 40% | TCJA phase-down |

| January 19, 2025 – December 31, 2030 (acquisition date January 19, 2025 or later) | 100% | OBBBA restoration |

| 2025 (acquisition date before January 19, 2025) | 40% | TCJA phase-down still in effect |

| 2026 (acquisition date before January 19, 2025) | 20% | TCJA phase-down still in effect |

Look-Back Studies: Recovering Missed Deductions

Investors who did not conduct a study at the time of acquisition are not permanently locked out. A look-back study allows them to claim all previously uncaptured depreciation as a catch-up deduction in a single tax year, without amending prior returns.

The IRS permits taxpayers to change their accounting method by filing Form 3115 under automatic change procedures. This process generates an IRC §481(a) adjustment, representing the difference between depreciation actually taken and what should have been deducted had the property been properly segregated from the start.

Under IRS rules, this applies to properties acquired or remodeled as far back as January 1, 1987.

How a Residential Cost Segregation Study Works

A cost segregation study is a formal engineering and tax analysis that identifies and documents every property component eligible for accelerated depreciation. It requires professionals with expertise across engineering, construction methodology, and tax law, not a spreadsheet exercise.

Step 1: Feasibility Analysis

The study begins with an assessment of whether the property is a strong candidate for cost segregation. The team evaluates:

- Property purchase price and improvement value (excluding non-depreciable land)

- Property type and characteristics

- Investor's tax situation and bracket

- Intended holding period

Properties with higher improvement values and owners in higher tax brackets tend to generate the most significant returns from the study. Industry benchmarks indicate properties with a depreciable basis exceeding $300,000 typically justify the study investment.

Step 2: Document and Data Collection

The study team collects all relevant documentation:

- Purchase or closing records (HUD-1 settlement statement)

- Construction contracts if applicable

- Blueprints or floor plans

- Property appraisals separating land from building value

- Inspection reports and site surveys

- Certificate of occupancy establishing placed-in-service date

Documentation quality shapes how precise the reclassification will be. Properties with itemized construction records, showing labor and materials by component, produce more defensible results than those with lump-sum invoices.

Step 3: Engineering-Based Property Analysis

Engineers and tax professionals walk through the property component by component, physically inspecting when necessary, and allocate costs to the correct depreciation categories. This step demands working knowledge of both construction costs and IRS classification rules, since assigning each element wrong creates audit exposure.

The IRS Cost Segregation Audit Techniques Guide explicitly prefers "engineering-based" methodologies over "rule of thumb" approaches, which lack sufficient documentation to support the allocation of project costs.

Step 4: Report Delivery and Tax Application

The completed study produces a formal report documenting:

- All reclassifications with supporting analysis

- Depreciation schedule for each component

- Total deductions available by year

- Legal citations to IRS authority supporting classifications

This report goes directly to your CPA or tax preparer to apply on your return. Seneca Cost Segregation typically delivers completed studies within 2–4 weeks, well ahead of the 30–60 day industry norm, and the AuditDefense guarantee covers you if the IRS ever questions the findings.

What Property Components of a Residential Rental Qualify for Accelerated Depreciation

The IRS distinguishes between structural components of the building (27.5-year life) and personal property or land improvements that are separate from the core structure. Cost segregation identifies which components fall into the shorter-life categories.

5- and 7-Year Personal Property Components

These are treated as personal property because they can be removed without materially damaging the building:

| Component | Depreciation Life |

|---|---|

| Built-in cabinetry and millwork | 5–7 years |

| Carpeting and specialty flooring | 5–7 years |

| Window treatments and blinds | 5–7 years |

| Appliances (refrigerators, ranges, dishwashers) | 5–7 years |

| Dedicated electrical outlets serving equipment rather than general building lighting | 5–7 years |

| Decorative fixtures and non-structural elements | 5–7 years |

According to IRS Publication 946, these components are classified under Asset Class 00.11 (Office Furniture, Fixtures, and Equipment) or treated as 5-year personal property under Rev. Proc. 87-56. Asset Class 57.0 applies when the property is used in a trade or business context; your tax advisor can confirm the correct classification for your specific rental structure.

15-Year Land Improvement Components

Revenue Procedure 87-56 covers Asset Class 00.3, which explicitly includes depreciable improvements directly added to land:

| Component | Depreciation Life |

|---|---|

| Driveways and parking areas | 15 years |

| Sidewalks and pathways | 15 years |

| Landscaping and grading | 15 years |

| Fencing | 15 years |

| Outdoor lighting | 15 years |

| Retaining walls | 15 years |

These sit outside the building structure and depreciate over 15 years.

Once you understand which components qualify, it's useful to see how the reclassification actually changes your first-year deduction in dollar terms.

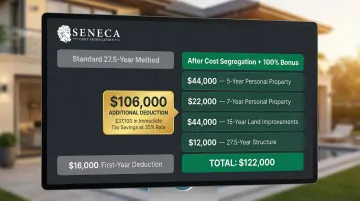

Simplified Example: First-Year Depreciation Comparison

Property Details:

- Purchase price: $550,000

- Land value: $110,000 (20%)

- Depreciable building basis: $440,000

Standard 27.5-Year Straight-Line Method:

- Annual depreciation: $440,000 ÷ 27.5 = $16,000

After Cost Segregation with 100% Bonus Depreciation:

- 5-year property (appliances, carpeting): $44,000 (10% of basis)

- 7-year property (cabinetry, fixtures): $22,000 (5% of basis)

- 15-year property (landscaping, driveway): $44,000 (10% of basis)

- Remaining 27.5-year property: $330,000 (75% of basis)

First-Year Deduction Calculation:

- 100% bonus on 5-year property: $44,000

- 100% bonus on 7-year property: $22,000

- 100% bonus on 15-year property: $44,000

- 27.5-year straight-line: $330,000 ÷ 27.5 = $12,000

- Total first-year deduction: $122,000

Difference: $122,000 vs. $16,000 = $106,000 additional first-year deduction

| Method | First-Year Deduction |

|---|---|

| Standard 27.5-Year Straight-Line | $16,000 |

| Cost Segregation + 100% Bonus Depreciation | $122,000 |

| Additional First-Year Deduction | $106,000 |

At a 35% combined federal and state tax rate, that translates to approximately $37,100 in immediate tax savings. Your actual result depends on your effective tax bracket, and investors in the 24%–37% federal range will see proportionally different outcomes. Bonus depreciation phased down from 100% under TCJA (80% in 2023, 60% in 2024, and 40% from January 1 through January 18, 2025). For qualified property with an acquisition date of January 19, 2025 or later, the OBBBA restored 100% bonus depreciation. The TCJA phase-down is still in effect for properties acquired before January 19, 2025, with 40% bonus depreciation in 2025 and 20% in 2026, so the property's acquisition date and the allocation percentages in the study will affect total first-year deductions.

Common Misconceptions and When Cost Segregation May Not Apply

Misconception: Cost Segregation Is Only for Commercial Properties

Many residential rental investors believe cost segregation is only for commercial properties or large apartment complexes. This is incorrect. Single-family rentals, duplexes, triplexes, and short-term rentals all qualify as long as they are income-producing. The study scales to match the property, so smaller properties generate smaller but still meaningful benefits.

According to IRS Publication 527, to qualify as "residential rental property," 80% or more of the building's gross rental income for the tax year must be derived from dwelling units. This explicitly includes single-family homes, duplexes, and small multi-family properties.

Misconception: You'll "Pay It All Back" Through Depreciation Recapture

Some investors avoid cost segregation assuming they will "pay it all back" when they sell. The math actually favors investors in most scenarios:

- Unrecaptured §1250 gain is taxed at a maximum 25% rate, which is typically lower than the investor's ordinary income tax rate during high-earning years

- The time value of money means dollars saved today are worth more than future recapture obligations

- Investors who hold through a §1031 like-kind exchange can defer recapture entirely

One important caveat: §1245 property — the 5- and 7-year personal property reclassified during the study — faces ordinary income tax rates upon recapture. Careful §1031 exchange structuring is required to avoid triggering taxable "boot."

Passive Activity Loss Limitations

For most residential rental investors, depreciation deductions generated by cost segregation are classified as passive losses under IRC §469, which can only offset passive income. Investors without sufficient passive income may find the deductions suspended until the property is sold or they generate offsetting passive income.

Real Estate Professional Exception

Taxpayers who qualify as real estate professionals under IRC §469(c)(7) can apply these deductions against ordinary income. To qualify, you must meet both tests during the tax year:

- More than 50% of personal services performed in all trades or businesses must be in real property trades or businesses in which you materially participate

- You must perform more than 750 hours of services during the tax year in real property trades or businesses in which you materially participate

Meeting both tests, along with material participation in the specific rental activity, removes the passive classification entirely.

When Cost Segregation May Not Generate Strong Returns

Cost segregation may not be optimal for:

| Scenario | Consideration |

|---|---|

| Properties with very low improvement value relative to land value | If land represents 40%+ of the purchase price, the depreciable basis may be too small to justify the study |

| Investors in low income tax brackets | The tax savings are minimal when marginal rates are 12-22% |

| Short intended holding periods | Properties planned for sale within 2-3 years face early recapture that could reduce net benefit |

Study Cost vs. Expected Return

Professional residential cost segregation studies typically range from $2,500 to $8,000, depending on property size, type, and documentation availability. For qualifying properties with a depreciable basis above $300,000, first-year tax savings almost always exceed the study fee.

Frequently Asked Questions

Can you do a cost segregation study on a residential rental property?

Yes, residential rental properties fully qualify for cost segregation studies, including single-family rentals, multi-family units, duplexes, and short-term rentals. The only exclusion is a personal primary residence that does not generate rental income.

Who qualifies for cost segregation?

Any owner of an income-producing property qualifies, whether residential or commercial. The most benefit goes to investors in higher tax brackets who have properties with substantial improvement values and intend to hold the property long-term or use §1031 exchanges.

How much does a residential cost segregation study cost?

Study costs vary based on property size, type, and documentation availability. Professional residential studies typically range from $2,500 to $8,000. The first-year tax savings typically exceed the study fee for qualifying properties with a depreciable basis above $300,000.

What is a look-back study and can I claim missed depreciation from past years?

A look-back study lets investors retroactively apply cost segregation to a property they already own, capturing all missed depreciation as a single deduction in the current tax year via Form 3115. No amended returns are needed, and it covers properties acquired as far back as January 1, 1987.

Does a cost segregation study increase my risk of an IRS audit?

Cost segregation is an IRS-recognized strategy with a clear legal foundation in the IRS Cost Segregation Audit Techniques Guide. Studies prepared by qualified engineers with full documentation are audit-defensible and do not inherently increase audit risk.

When is the best time to get a cost segregation study for a rental property?

The ideal time is in the same tax year the property is acquired, constructed, or significantly renovated. This timing matters especially now that 100% bonus depreciation applies to qualified property with an acquisition date of January 19, 2025 or later. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively. That said, a look-back study can be ordered at any time for properties already owned.