Introduction

The IRS requires multi-tenant office buildings to depreciate over 39 years—but the assets inside them don't all belong on that timeline. Tenant-specific finishes, shared building systems, parking lots, landscaping, and specialty electrical installations each qualify for accelerated schedules of 5, 7, or 15 years. Industry data shows 20% to 40% of a commercial building's components can be reclassified into shorter tax categories. Most owners never capture these deductions because no one has performed a proper cost breakdown.

This guide explains how cost segregation works for multi-tenant office buildings—which assets qualify, what drives study outcomes, and how to assess whether a study makes financial sense for your property. It also covers how the restored 100% bonus depreciation under the One Big Beautiful Bill Act creates immediate cash flow benefits for properties acquired after January 19, 2025.

TL;DR

- Cost segregation reclassifies building components from 39-year schedules into 5-, 7-, or 15-year categories, accelerating tax deductions and improving cash flow

- Multi-tenant office buildings are strong candidates due to layered asset mixes: shared systems, tenant improvements, and land improvements follow different depreciation timelines

- Quality studies require licensed engineers who physically inspect the property and document every component to IRS standards

- Renovations and tenant buildouts are high-yield opportunities: over 80% of costs often qualify for accelerated depreciation categories

- Order a study at acquisition or retroactively for properties owned since 1987 via Form 3115 catch-up procedures

What Is Cost Segregation for Multi-Tenant Office Buildings?

Cost segregation is the IRS-recognized process of identifying and reclassifying components of a commercial property into shorter depreciable asset classes so owners can take larger tax deductions earlier in the property's life.

Multi-tenant office buildings present unique opportunities because they contain both shared infrastructure—lobbies, elevators, rooftop HVAC—and highly customized tenant suites, each with different expected useful lives. This complexity creates more reclassification opportunities than single-use properties, but also demands more precise engineering analysis.

The Default vs. Accelerated Depreciation

Without a cost segregation study, the IRS defaults every dollar spent on nonresidential real property to a 39-year MACRS recovery period. That spreads your entire tax benefit over nearly four decades—instead of concentrating deductions in the early years when reinvestment opportunities are highest.

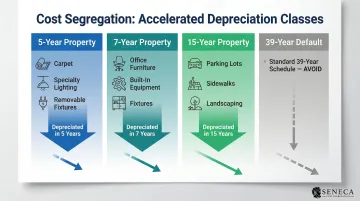

A proper study identifies which components legally qualify for accelerated schedules, including:

- 5-year property: Carpeting, specialty lighting, removable fixtures, and tenant improvement components

- 7-year property: Office furniture and equipment fixtures built into the structure

- 15-year property: Parking lots, sidewalks, landscaping, and site utilities

Each reclassified dollar moves from a 39-year schedule into one of these shorter classes, front-loading deductions into the years when they have the most impact on cash flow.

Why Multi-Tenant Office Buildings Are Ideal Candidates for Cost Segregation

Commercial office properties carry a wide range of asset classes under one roof. Site improvements, interior buildouts, mechanical systems, and tenant-specific fixtures all depreciate at different rates. Research confirms that 20% to 40% of depreciable basis is eligible for acceleration in Class A office buildings, creating substantial near-term tax savings.

Tenant Improvement Allowances: The Hidden Opportunity

Tenant improvement allowances (TIAs) represent one of the most commonly missed opportunities in multi-tenant properties. When a landlord funds improvements for a tenant's specific suite, those costs often qualify for 5- or 7-year depreciation rather than 39 years. Qualifying assets typically include:

- Specialty electrical panels and wiring

- Flooring and finish materials

- Custom cabinetry and millwork

- Dedicated HVAC units

Each lease renewal or new tenant buildout creates fresh reclassification potential.

To put numbers behind it: a $6 million multi-tenant office acquisition with 25% of basis eligible for reclassification yields $1.5 million in accelerated deductions. With 100% bonus depreciation, that entire amount becomes a year-one write-off instead of being spread over 39 years—reducing taxable income precisely when the investment is most capital-intensive.

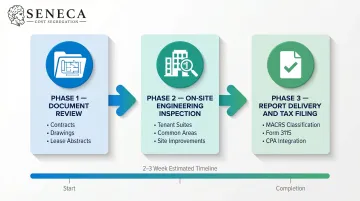

How a Cost Segregation Study Works: Step-by-Step for Office Buildings

A cost segregation study is an engineering-led analysis covering three phases: document review, physical site inspection, and a written report classifying every asset into its appropriate MACRS class life. The IRS Cost Segregation Audit Techniques Guide requires that studies be prepared by individuals with engineering or construction expertise — not accounting staff alone.

Here's how each phase works for a multi-tenant office building.

Step 1: Property Review and Document Analysis

The process begins before a site visit. The engineering team collects and analyzes:

- Construction contracts and contractor invoices

- Architectural drawings and blueprints

- Existing depreciation schedules

- Lease abstracts and tenant improvement schedules

- Tenant improvement allowance documentation

For multi-tenant buildings, the team must determine what costs were landlord-funded versus tenant-funded, as this affects who claims the deductions.

Step 2: On-Site Engineering Inspection

Engineers walk the property systematically, documenting every component—from carpet and specialty lighting in tenant suites to parking lot surfaces, monument signage, and exterior landscaping. For multi-tenant buildings, the inspection accounts for both shared common areas and individual tenant spaces, since these asset mixes are evaluated separately. Engineers use IRS-approved pricing guides to assign costs to each component.

Step 3: Report Delivery and Tax Filing Integration

The final deliverable is a detailed written report that:

- Categorizes each identified asset by component type

- Justifies its assigned class life

- Reconciles total allocated costs with total actual costs

- Provides documentation designed to be defensible under IRS audit

Your CPA uses this report to update depreciation schedules or, for prior-year properties, to file Form 3115 (Change in Accounting Method) to claim catch-up deductions without amending prior returns. Firms like Seneca Cost Segregation typically deliver completed studies within 2-4 weeks, making it straightforward to integrate into your tax filing timeline.

What Gets Reclassified in a Multi-Tenant Office Building

Multi-tenant office buildings can spread depreciation across four asset classes — 5-year, 7-year, 15-year, and 39-year — and knowing which components fall where helps you estimate potential savings before commissioning a study.

5-Year Personal Property

These are items expected to be replaced or removed within a normal tenant cycle:

- Carpet and specialty flooring (vinyl, tile installed with strippable adhesive)

- Built-in cabinetry and decorative millwork

- Electrical outlets and data cabling dedicated to specific tenant equipment

- Breakroom fixtures and appliances

- Decorative lighting (not primary building illumination)

- Fire extinguishers and safety equipment

7-Year Assets

- Built-in office furniture

- Specialized interior fixtures tied to a specific tenant's use, not the building structure

15-Year Land Improvements

These are frequently significant in multi-tenant office parks. A real-world study of a $6.7 million multi-tenant office complex identified 10% ($670,000) as 15-year land improvements:

- Parking lots and paved driveways

- Outdoor landscaping (depreciable types)

- Monument signs and pylons

- Drainage infrastructure

- Protective bollards

- Exterior lighting (pole-mounted, not building-mounted)

What Stays at 39 Years

The building "shell" or base structure remains at 39 years:

- Structural steel and concrete foundation

- Exterior walls and roof structure

- Elevators and escalators

- Core HVAC systems serving the building as a whole

Important: Reclassification doesn't reduce the total amount you depreciate. It determines how quickly those deductions are taken, shifting value from later years into the early years when it matters most.

Key Factors That Affect Cost Segregation Results in Multi-Tenant Office Buildings

Tenant Mix and Customization Level

A building with multiple professional-service tenants who each required custom buildouts will typically yield more reclassifiable costs than a single-tenant NNN property with minimal landlord-funded improvements. The more complex and customized the interior, the more assets can be moved into shorter class lives.

Acquisition Date and Holding Period

Studies deliver the greatest benefit when ordered at or shortly after acquisition, since the full accelerated deduction is captured from year one. For owners who acquired a property years ago without a study, a retroactive look-back analysis via Form 3115 allows them to catch up on missed depreciation in the current tax year, with no need to file amended returns.

Look-back studies apply to properties acquired, constructed, or renovated since 1987.

Qualified Improvement Property (QIP) for Renovations

Improvements made to the interior of a nonresidential building after it was originally placed in service may qualify as QIP, which carries a 15-year recovery period and is bonus-eligible. For multi-tenant office buildings undergoing renovation, this can mean that over 80% of renovation costs are eligible for accelerated or immediate write-off.

Key QIP eligibility rules to know:

- Qualifies: Most interior tenant improvements, partitions, finishes, and lighting

- Excluded: Enlargements, elevators, escalators, and internal structural framework

Common Misconceptions — and When Cost Segregation May Not Apply

Three Common Misconceptions

1. "Cost segregation is only for very large properties"

Reality: Any commercial property valued at approximately $500,000 or more can benefit meaningfully, especially with 100% bonus depreciation. The tax savings typically far exceed the study cost.

2. "A study increases audit risk"

Reality: A properly documented, engineering-based study actually strengthens the taxpayer's position. The IRS expects these studies to be performed by qualified engineers, and a professional report provides the documentation needed to defend your position.

3. "Cost segregation creates new deductions"

Reality: It accelerates existing deductions forward in time. The same total depreciation is taken—just sooner, when cash flow matters most.

When a Study May Not Be Cost-Effective

A cost segregation study isn't the right fit for every property or situation. Watch for these scenarios:

- Land-heavy acquisitions where most of the purchase price reflects land value rather than improvements — reclassification potential is limited when there's little to reclassify.

- No near-term tax liability — owners with no federal tax bill cannot benefit from additional deductions unless they can carry losses forward.

- Short-term holds — depreciation recapture taxes prior depreciation at ordinary income rates (up to 25% for unrecaptured Section 1250 gain), which erodes the net benefit unless a 1031 exchange is planned.

Passive Activity Loss (PAL) Rules

Owners who are not classified as real estate professionals under IRS rules can generally only use accelerated depreciation losses to offset passive income — not active W-2 or business income.

To qualify as a real estate professional, you must meet two strict tests:

- More than 50% of personal services performed in all trades or businesses must be in real property trades

- You must perform more than 750 hours of services in real property trades in which you materially participate

Consult your CPA before commissioning a study to confirm your ability to use the deductions.

Frequently Asked Questions

What is cost segregation for multi-tenant office buildings?

Cost segregation is an engineering-led tax process that reclassifies components of a multi-tenant office building (such as tenant finishes, land improvements, and specialty systems) from the default 39-year depreciation schedule into 5-, 7-, or 15-year categories, accelerating deductions and improving cash flow.

What types of properties qualify for cost segregation?

Cost segregation applies to virtually any commercial or residential income-producing property, including office buildings, retail centers, industrial facilities, multifamily complexes, hotels, medical offices, and self-storage facilities. Generally, properties placed in service after 1987 with a cost basis of $1 million or more yield the strongest results.