Introduction

Many real estate investors assume cost segregation is reserved for skyscrapers, hotel chains, or large industrial complexes. In reality, nearly every income-producing property qualifies — the real question is whether the tax savings justify the study's cost.

This article covers IRS eligibility criteria, the main categories of qualifying properties, which property types yield the strongest results, and how to evaluate whether a study makes financial sense for your situation. With 100% bonus depreciation permanently restored for property placed in service after January 19, 2025, the potential first-year tax savings are significant — making it worth understanding exactly where you stand.

TL;DR

- Nearly all income-producing real estate placed in service after 1986 qualifies for cost segregation

- Properties must be used for business or investment, have meaningful depreciable basis, and were built or acquired after January 1, 1987

- Reclassification percentages vary by property type; specialty properties like gas stations often outperform standard commercial buildings

- The One Big Beautiful Bill (signed July 4, 2025) permanently restored 100% bonus depreciation for qualifying assets placed in service after January 19, 2025

- A complimentary benefit estimate shows whether projected savings justify study costs before you engage

What Makes a Property Eligible for Cost Segregation?

The IRS sets three practical eligibility criteria for cost segregation:

1. Business or Investment Use

The property must be income-producing or used in a trade or business. Primary residences do not qualify. Rental properties, commercial buildings, and owner-occupied business properties all meet this requirement.

2. Placed in Service After 1986

Properties must have been built, purchased, or significantly renovated after January 1, 1987. This is when the Modified Accelerated Cost Recovery System (MACRS) became the standard depreciation method for real estate.

3. Sufficient Depreciable Basis

While the IRS does not set a minimum depreciable basis, properties with basis under $250,000 rarely generate enough savings to justify study costs. Seneca Cost Segregation typically recommends a minimum depreciable basis of $300,000 (excluding land value) for a strong return on investment.

Qualifying vs. Being a Good Candidate

Virtually all investment properties "qualify" for cost segregation from a technical standpoint. The real question is whether the property contains enough short-life components—appliances, fixtures, specialized systems, site improvements—to make accelerated depreciation meaningful. Properties with minimal personal property or site improvements may qualify but deliver modest results.

Current Bonus Depreciation Landscape

Whether a property is a good candidate matters more right now than it has in years. The One Big Beautiful Bill (Public Law 119-21) permanently restored 100% bonus depreciation for qualifying property acquired and placed in service after January 19, 2025, eliminating the phase-down schedule that had been reducing the benefit annually under prior law.

Any property purchased or construction completed after that date can now claim an immediate 100% first-year deduction on all components reclassified to 5-, 7-, or 15-year depreciation schedules. Deductions that previously spread across several years now hit entirely in year one—making strong candidacy the difference between a modest tax benefit and a transformative one.

Types of Properties That Qualify for Cost Segregation

There is no IRS restriction on property type. Residential rentals, commercial buildings, industrial facilities, short-term rentals, and specialty properties all qualify. What matters is how the property is used (investment or business purpose) and its depreciable basis.

Residential Rental Properties

What qualifies:

- Single-family rental homes

- Duplexes, triplexes, and fourplexes

- Apartment buildings and complexes

- Condos and townhouses held as investment properties

Residential rental properties are depreciated over 27.5 years under standard MACRS rules, so reclassifying shorter-life components front-loads deductions that would otherwise stretch across nearly three decades.

Commonly reclassified components:

- Carpeting and vinyl flooring (5-year property)

- Appliances—refrigerators, dishwashers, stovetops (5-year property)

- Window coverings—blinds, shades, drapes (7-year property)

- Cabinetry and countertops (5-year property)

- Landscaping, sidewalks, and driveways (15-year property)

Research from industry practitioners shows that multifamily and apartment properties typically see 20%–50% of depreciable costs reclassified into shorter depreciation schedules through cost segregation.

Commercial Properties

What qualifies:

- Low-rise and high-rise office buildings

- Medical and dental offices

- Hospitals and outpatient clinics

- Hotels and motels

- Mixed-use developments

- Retail spaces and shopping centers

Commercial properties are depreciated over 39 years, which widens the gap between standard depreciation and what cost segregation can unlock—more basis to reclassify means larger early-year deductions.

High-value reclassification components:

- Specialized lighting systems (5-year property)

- Tenant improvements—partitions, counters, built-in fixtures (5- or 7-year property)

- HVAC components serving specific tenant spaces (5-year property)

- Decorative finishes and millwork (7-year property)

- Parking lots, curbs, and asphalt paving (15-year property)

Parking lot improvements alone can represent a substantial portion of reclassifiable basis, as asphalt, striping, and site lighting typically qualify for 15-year treatment.

Industrial and Warehouse Properties

What qualifies:

- Distribution warehouses

- Manufacturing plants

- Self-storage facilities

- Research and development facilities

- Industrial distribution centers

Industrial properties look simple on paper, but the specialized systems inside—electrical, mechanical, and site infrastructure—routinely generate substantial reclassifiable basis.

Key reclassifiable components:

- Specialized electrical systems supporting equipment (5-year property)

- Machinery foundations and equipment anchoring (5-year property)

- Heavy-duty industrial lighting (5-year property)

- Dock equipment—levelers, seals, bumpers (7-year property)

- HVAC systems designed for industrial use (5-year property)

Self-storage facilities in particular benefit from high site improvement values—fencing, security systems, paving, and lighting—that qualify for 15-year schedules. Industry benchmarks indicate self-storage properties typically see 22%–32% of costs reclassified, with minimal structural components relative to site improvements.

Short-Term Rentals (STRs)

What qualifies:

- Airbnb properties

- VRBO rentals

- Vacation homes rented short-term

- Corporate housing units

Short-term rentals are classified as non-residential property and depreciated over 39 years rather than the 27.5-year residential schedule. This actually increases the benefit of reclassifying shorter-life components through cost segregation, since the gap between 39-year building life and 5-year personal property is even wider.

Material participation and passive loss rules:

Under IRS passive activity loss rules, an activity is not a "rental activity" if the average customer stay is seven days or less. If your STR qualifies as non-rental under this test and you materially participate (typically 500+ hours per year), you can use passive losses to offset ordinary income—making cost segregation especially powerful for active STR owners.

Common reclassifiable components:

- Furnishings—beds, sofas, tables, décor (7-year property)

- Kitchen appliances and cookware (5-year property)

- Electronics—TVs, sound systems (5-year property)

- Property improvements—flooring, fixtures, cabinetry (5- or 7-year property)

- Landscaping and outdoor amenities (15-year property)

Special-Purpose and Niche Properties

What qualifies:

- Restaurants (casual and fast-food)

- Gas stations and convenience stores

- Car washes (automatic and self-service)

- Auto dealerships

- Drug stores and pharmacies

- Medical clinics with specialized equipment

These properties are purpose-built around specialized equipment and systems, which means a higher share of total cost shifts into 5- and 15-year schedules—often far more than standard commercial or residential properties.

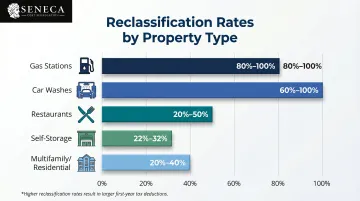

- Gas stations: Underground storage tanks, fuel dispensers, pump canopies, and specialized lighting drive extremely high reclassification. Industry data shows gas stations can achieve 80%–100% reclassification rates due to the high ratio of personal property to structural shell.

- Car washes: Conveyors, dryers, pumps, and control systems qualify as 5- or 7-year property. Studies show car washes can see 60%–100% of costs reclassified into accelerated schedules.

- Restaurants: Kitchen hood systems, appliance plumbing and electrical hook-ups, refrigeration equipment, POS systems, and decorative finishes add up fast. The IRS Cost Segregation Audit Techniques Guide explicitly classifies many restaurant components as 5-year property under Asset Class 57.0 (Distributive Trades and Services).

Which Property Types Generate the Highest Tax Savings?

Not all properties are created equal when it comes to cost segregation. The higher the ratio of personal property and site improvements to structural shell, the larger the accelerated deductions — and some property types dramatically outperform others.

Top-Performing Standard Property Types

Apartment complexes and multifamily properties:

Appliances, flooring, cabinetry, and common-area amenities drive strong reclassification. Typical rates range from 20%–50% of depreciable basis, depending on property age and unit count.

Hotels and resorts:

Guest room furniture, window treatments, and flooring — multiplied across every room — add up quickly. Common areas (lobbies, restaurants, conference rooms) layer on additional personal property content. Reclassification benchmarks: 25%–45%.

Medical offices:

Specialized plumbing, dedicated HVAC, electrical infrastructure for equipment, and patient-area finishes all qualify for shorter depreciable lives. High tenant improvement density means medical facilities routinely outperform standard office buildings.

Restaurants:

Kitchen systems (hoods, refrigeration, cooking equipment), POS systems, decorative millwork, and signage typically qualify for 5- or 7-year treatment. Reclassification rates of 20%–50% are common.

Highest-Performing Niche Property Types

Self-storage facilities:

Minimal structural shell relative to site improvements — paving, fencing, security systems, lighting — pushes reclassification higher than most. Baseline rates of 22%–32% are typical, with well-designed facilities achieving more.

Car washes:

Conveyors, dryers, pumps, and control systems all qualify as §1245 personal property. Because nearly the entire operation is equipment-driven, reclassification of 60%–100% is achievable.

Gas stations:

Underground storage tanks, fuel dispensers, pump islands, canopies, and petroleum marketing land improvements qualify for accelerated treatment. Industry data shows 80%–100% reclassification potential — among the highest of any property type.

Mobile home parks:

Roads, water and sewer systems, electrical distribution, and site lighting qualify for 15-year land improvement treatment. Community buildings and amenities add personal property eligible for 5- or 7-year schedules.

The Site Improvement Advantage

Exterior site improvements benefit properties across every category — not just niche types. Common qualifying improvements include:

- Parking lots and paved surfaces

- Landscaping and grading

- Curbs, sidewalks, and drainage

- Outdoor lighting and fencing

All of these qualify for 15-year MACRS depreciation rather than the standard 39-year building schedule. A commercial property with a $500,000 parking lot, for instance, cuts the depreciation timeline on that component by more than half — a straightforward win that often gets overlooked.

What About Renovations, Recent Acquisitions, and Properties You Already Own?

Look-Back Studies for Properties You Already Own

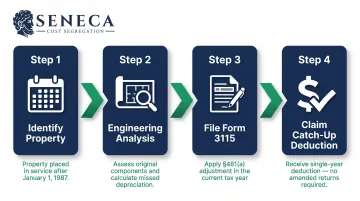

Property owners who did not perform a cost segregation study at purchase or construction can still capture missed depreciation for prior years through a look-back study. The IRS allows this for properties placed in service as far back as January 1, 1987, and the catch-up deduction can be claimed in a single tax year without amending prior returns.

How it works: Look-back studies use Form 3115 (Application for Change in Accounting Method) to claim a §481(a) adjustment in the current tax year. This adjustment represents all the depreciation you should have claimed in prior years but didn't. The IRS treats this as an automatic accounting method change, filed with your current-year return — no penalties, no amended filings required.

Seneca Cost Segregation's engineering team conducts a detailed engineering analysis of the property as it existed when originally placed in service, identifying which components qualify for accelerated depreciation and calculating the cumulative missed deductions.

Renovated and Rehabilitated Properties

Significant renovations or capital improvements create a separate cost segregation opportunity. The improvement costs are analyzed independently from the building's original basis, allowing you to reclassify components installed during the renovation.

Timing matters: Conducting a cost segregation study before a major renovation establishes a clear baseline that simplifies identifying what was replaced versus what is new. This documentation supports the partial disposition election opportunity.

Partial disposition election: When old components are replaced during renovation, Treas. Reg. §1.168(i)-8 allows taxpayers to elect a partial disposition to recognize a loss on the unrecovered basis of the disposed component. A cost segregation study provides the necessary cost breakdown to support this election, potentially generating immediate tax benefits from the retirement of old assets.

Recently Acquired Properties

If you're in the year of acquisition: The ideal time to conduct a cost segregation study is before filing the tax return for the year of acquisition or completion. This allows you to claim the maximum first-year benefit without any catch-up adjustments.

If you've owned the property for years: The look-back option often produces substantial savings. Many property owners discover cost segregation years into ownership and still recover substantial missed deductions through Form 3115.

How to Determine Whether a Cost Segregation Study Is Worth It for Your Property

The Basic ROI Framework

Cost segregation studies typically cost between $3,000 and $15,000 depending on property size, type, and complexity. Industry data shows that studies typically deliver savings of 25x–35x the cost of the study, meaning a $5,000 study might generate $125,000 to $175,000 in first-year tax deductions.

The study pays for itself when projected first-year tax savings substantially exceed the cost. As a practical benchmark, properties with a depreciable basis of $300,000 or more generally produce strong ROI. Seneca Cost Segregation offers a complimentary benefit estimate to model your potential savings before you commit to a study.

How Tax Bracket Affects Value

The higher your effective tax rate, the more valuable each dollar of accelerated depreciation becomes. The math is straightforward:

At the top federal rate of 37%: An additional $100,000 in first-year depreciation represents $37,000 in federal tax savings. When you add state income taxes (which can be 5%–13% depending on your location), the total savings on that $100,000 deduction could reach $40,000–$50,000.

At a 24% federal rate: The same $100,000 deduction generates $24,000 in federal savings, plus state taxes.

The pattern is clear: the higher your tax bracket and the more taxable income you're carrying, the more immediate the benefit from accelerated depreciation.

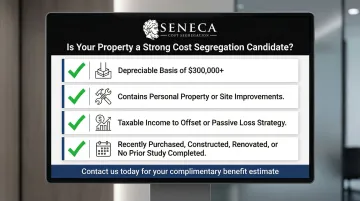

Key Indicators of a Strong Candidate

Your property is likely a strong candidate if it meets these criteria:

- Depreciable basis of $300,000 or more (excluding land value)

- Contains personal property or site improvements—not just bare structural shell

- You have taxable income to offset or a tax strategy that leverages passive losses

- Recently purchased, constructed, or significantly renovated, or acquired in prior years without a prior study

Properties meeting all four criteria almost always deliver substantial ROI. Even properties meeting only two or three criteria may be viable—contact Seneca Cost Segregation for a complimentary analysis to determine your specific potential.

Frequently Asked Questions

What property is not eligible for bonus depreciation?

Primary residences, land (which is never depreciable), and property with a useful life of 20 years or more under the Alternative Depreciation System (ADS) generally do not qualify for bonus depreciation. Listed property used 50% or less for business purposes is also excluded.

Do short-term rentals like Airbnb qualify for cost segregation?

Yes, short-term rentals qualify for cost segregation. Because a higher proportion of components can be reclassified into shorter depreciation schedules, the benefit is often greater than with long-term residential rentals.

Is there a minimum property value required to qualify for cost segregation?

The IRS does not set a minimum depreciable basis for cost segregation eligibility. Properties with a depreciable basis under $250,000–$300,000 may not generate enough savings to justify study costs. A benefit estimate can clarify this for any specific property.

Can I apply cost segregation to a property I purchased several years ago?

Yes, look-back studies allow property owners to retroactively capture missed depreciation on properties purchased, constructed, or renovated as far back as January 1, 1987. The catch-up deduction is claimed in a single year via an IRS accounting method change using Form 3115.

What percentage of a property's cost is typically reclassified through cost segregation?

Reclassification percentages vary by property type. Residential rentals and commercial properties often see 20%–40% of depreciable costs reclassified into shorter-life categories, while niche properties like car washes or self-storage facilities can reach 60%–100% of total depreciable basis.

Can cost segregation be applied to a property that has undergone major renovations?

Yes, renovation costs can be included in a cost segregation study. Improvements are analyzed separately from the building's original basis, and conducting the study before or immediately after renovation maximizes reclassification opportunities. This approach also supports partial disposition elections when old components are replaced.

Ready to find out how much your property could save? Seneca Cost Segregation offers a complimentary benefit estimate at no obligation — with over 10,200 studies completed nationwide and an average first-year deduction of $171,243. Call 503-383-1158 or visit senecacostseg.com to get started.