Introduction

Nail salon owners routinely invest $200,000 to $500,000 or more in specialized buildouts — pedicure plumbing systems, chemical ventilation exhaust, custom cabinetry, and decorative millwork. Yet most never realize that 30–40% or more of those costs can be reclassified to generate substantial accelerated tax deductions through cost segregation.

Without this strategy, that entire investment depreciates slowly over 39 years under standard commercial real estate rules. Cost segregation works by identifying specialized components that legally qualify for 5-year, 7-year, or 15-year depreciation schedules instead.

With the 2025 reinstatement of 100% bonus depreciation, many of those reclassified assets can now be fully deducted in year one — turning a slow 39-year write-off into immediate cash flow.

This guide breaks down which nail salon assets qualify for accelerated depreciation, what realistic savings look like, and how to know whether a study makes financial sense for your situation.

TLDR: Key Takeaways for Nail Salon Owners

- Cost segregation reclassifies buildout costs to 5, 7, or 15-year schedules instead of the default 39-year depreciation timeline

- Nail salons qualify due to specialized assets — pedicure plumbing, ventilation systems, salon furniture, and trade fixtures

- Owners can often reclassify 20–40% or more of buildout costs to accelerated schedules

- The 2025 reinstatement of 100% bonus depreciation means qualifying assets can frequently be fully deducted in the first year

What Is Cost Segregation and How Does It Apply to Nail Salons?

The Standard Depreciation Problem for Salon Owners

Commercial real estate depreciates over 39 years under the Modified Accelerated Cost Recovery System (MACRS). A nail salon owner with a $500,000 buildout would deduct only $12,820 per year without cost segregation — locking the majority of that investment into slow deductions for nearly four decades.

Cost segregation is an engineering-based tax analysis that identifies individual property components — equipment hookups, specialized fixtures, land improvements — that legally qualify for 5-year, 7-year, or 15-year depreciation instead of 39 years. This accelerates the same total deduction into the early years of ownership, freeing up cash flow in the first few years of ownership, when reinvestment opportunities are greatest.

IRS Classification Framework for Nail Salons

Nail salons fall under Asset Class 57.0 – Distributive Trades and Services in the IRS classification system. This designation explicitly covers retail and personal service businesses, establishing 5-year recovery periods for qualifying personal property within them.

The IRS Cost Segregation Audit Techniques Guide (Publication 5653) provides explicit guidance for these reclassifications, including industry-specific asset classification matrices for retail and personal service businesses. Under this framework, qualifying salon assets commonly include:

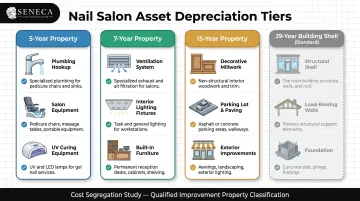

- Pedicure chair plumbing and electrical hookups (5-year property)

- Ventilation systems specific to chemical fume management (7-year property)

- Decorative millwork and specialized lighting (5-year property)

- Parking lot surfaces and exterior signage (15-year property)

Each of these components can be separated from the 39-year building shell — often converting 20% to 40% of total buildout costs into accelerated deductions.

Which Nail Salon Assets Qualify for Accelerated Depreciation?

5-Year Property: Specialized Service Equipment and Dedicated Systems

Specialized plumbing hookups to service stations

Dedicated water supply lines, drain lines, and gas connections running directly to pedicure basins, nail washing sinks, and footbath stations qualify as §1245 personal property with a 5-year recovery period. The IRS explicitly states: "a hair salon in a retail outlet would require special hair washing sinks and water hook-up for the sinks" — this logic applies equally to nail salon pedicure stations. Standard building plumbing serving general functions remains 39-year §1250 property.

Dedicated electrical connections to nail equipment

Special electrical outlets, conduit, and circuit breakers wired directly to specific nail equipment qualify as §1245 property at a 5-year recovery period. Qualifying equipment includes:

- UV/LED curing lamps

- Electric nail drills

- Pedicure massage chairs

- Sterilization units

General building electrical infrastructure remains 39-year property.

Specialized chemical ventilation systems

Nail salons require dedicated exhaust and ventilation systems to remove acrylic, gel, and acetone fumes, a need unique to nail service operations.

The IRS applies a "sole justification" test: ventilation installed solely because nail operations require it — not for general occupant comfort — may qualify as §1245 personal property. Document the system's dedicated purpose carefully; this distinction is what makes or breaks the classification.

Pedicure chairs, massage units, and salon-specific equipment

Pedicure massage chairs with built-in jets and basins, free-standing manicure tables, rolling nail tech carts, and UV lamps are personal property classified under the distributive trades asset class (the IRS classification for retail and service businesses) with 5-year recovery periods.

5-Year Property: Fixtures, Finishes, and Furnishings

Salon-specific fixtures and decorative millwork

- Reception counters and nail technician workstations

- Retail product display shelving

- Decorative wall paneling not integral to the structural shell

- Salon-specific cabinetry that enhances décor rather than serving a building function

Restroom cabinets or structural millwork do not qualify — they remain 39-year building components.

Strippable flooring, signage, sound systems, and POS equipment

- Vinyl or carpet flooring installed with strippable (non-permanent) adhesives

- Interior and exterior trade name signage

- Background music and sound systems

- Point-of-sale/payment terminal systems

- Readily removable privacy partitions or room dividers

All qualify as 5-year personal property under the distributive trades classification.

15-Year Land Improvements

If the nail salon owner owns the building and land, these qualify as 15-year land improvements — still a significant acceleration compared to 39-year treatment:

- Parking lot surfaces

- Pole-mounted outdoor lighting systems

- Pylon signs

- Landscaping (where depreciable)

How Much Could Your Nail Salon Actually Save?

The Financial Impact of Reclassification

Typical reclassification percentages

Research shows that 20–50% of total property costs are typically reclassified in salon, restaurant, and retail settings. Nail salons, with their high concentration of specialized plumbing, ventilation, and service equipment, often fall toward the higher end of this range.

Illustrative savings scenario

Consider a nail salon owner who purchases or builds out a $400,000 commercial space:

- Without cost segregation: First-year depreciation = $10,256 (39-year standard rate)

- With cost segregation: 30% ($120,000) reclassified to 5-year assets eligible for 100% bonus depreciation

- First-year deduction on reclassified assets: $120,000

- Difference: Roughly $109,000 in additional first-year deductions

At a 35% effective tax rate, that translates to approximately $38,000 in immediate tax savings.

The 100% Bonus Depreciation Multiplier in 2025

The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, permanently reinstated 100% bonus depreciation for eligible assets placed in service after January 19, 2025. For nail salon owners with qualifying 5-year and 15-year personal property identified through a cost segregation study, salon owners can now fully expense these assets in the year they put them in service, moving substantial cash savings into year one.

Qualified Improvement Property (QIP) (interior leasehold improvements to nonresidential buildings) carries a 15-year recovery period under IRC §168(e)(6), making it fully eligible for 100% bonus depreciation.

ROI on a Cost Segregation Study

Those bonus depreciation benefits translate directly into study ROI. Seneca Cost Segregation reports an average first-year deduction of $171,243 across their portfolio of studies, and industry-wide returns commonly hit 10:1 or higher — meaning every dollar spent on the study typically yields ten or more in tax savings.

The actual benefit for your salon depends on three factors:

- Property value — higher acquisition or build-out costs create more reclassification opportunity

- Reclassification percentage — nail salons with specialized plumbing and ventilation often hit 30–50%

- Effective tax rate — the higher your rate, the greater the cash impact of each additional deduction

When Should a Nail Salon Owner Get a Cost Segregation Study?

Timing Scenarios That Trigger Maximum Benefit

New purchase or construction

The ideal time is immediately after purchasing or completing construction — in the same tax year the property is placed in service. This lets reclassified assets capture bonus depreciation from day one and keeps your depreciation method clean from the start.

Existing properties — the look-back opportunity

Nail salon owners who purchased or built out their space in prior years without a study are not locked out. A look-back study recaptures all the accelerated depreciation that should have been taken, applied in the current tax year via IRS Form 3115 (Change in Accounting Method, no amended returns required). There is no statute of limitations that cuts off this option.

Pre-renovation or equipment replacement

If planning to replace pedicure stations, redo plumbing, or expand service areas, commission a cost segregation study before renovation. This enables a partial asset disposition (PAD) election, which unlocks three key advantages:

- Write off the remaining depreciable basis of old components being discarded

- Accelerate deductions before new assets are placed in service

- Avoid carrying dead basis on assets no longer in use

How the Cost Segregation Process Works for Nail Salon Owners

From Initial Review to Your CPA's Return

Step 1 – Complimentary savings estimate

A qualified provider reviews key details about the nail salon property — purchase price or buildout cost, square footage, property type, year placed in service — and provides a no-cost estimate of potential tax savings before any commitment. This lets owners decide whether a study is worth pursuing before spending a dollar.

Step 2 – Engineering-based study and asset identification

A quality cost segregation study requires a credentialed engineering professional, ideally one holding the Certified Cost Segregation Professional (CCSP) designation from the American Society of Cost Segregation Professionals (ASCSP). The work involves reviewing construction documents and lease agreements, often paired with a site inspection to identify and value individual assets.

Seneca Cost Segregation handles this with CCSP-certified engineers and delivers completed studies in 2–4 weeks. Every study includes AuditDefense and a money-back guarantee, so nail salon owners have both a defensible result and full protection if the IRS ever questions the findings.

Step 3 – Delivery to your CPA and ongoing tax filing

The completed cost segregation report is delivered to your CPA or tax advisor, who applies the reclassified depreciation schedules to your federal return. For look-back studies, the catch-up depreciation is claimed through a Form 3115 filed with the current year's return.

Frequently Asked Questions

What items qualify for cost segregation?

In a nail salon, qualifying assets are reclassified based on their function and permanence. Common examples include:

- Pedicure station plumbing hookups and chemical ventilation systems

- Electrical connections to salon equipment

- Pedicure chairs, manicure tables, and reception counters

- Strippable flooring, decorative millwork, and signage

- Sound systems, POS terminals, and parking lot improvements

How much does cost segregation cost?

Study fees vary based on property size and complexity, but reputable providers offer a complimentary savings estimate before any commitment. Fees are typically a small fraction of the first-year savings achieved, and the study cost itself is a deductible business expense.

How much can you write off for cost segregation?

Cost segregation doesn't change the total deductions available; it accelerates the timeline for taking them. Nail salons commonly shift 20–40% of buildout costs to shorter depreciation schedules, and with 100% bonus depreciation in 2025, many of those assets can be deducted entirely in year one.

Who performs a cost segregation study?

The IRS notes that engineering-based studies are more reliable and IRS-defensible than those prepared without construction expertise. Look for providers with the CCSP designation from ASCSP and a documented engineering-based methodology; these signal audit-ready quality.

What is the cost segregation process?

The process involves three main steps: a complimentary savings estimate based on property details, an engineering analysis that identifies and values qualifying assets, and delivery of the final report to your CPA for application on your tax return.

What is the IRS stance on cost segregation?

Cost segregation is a fully legal, IRS-recognized strategy outlined in the agency's own Cost Segregation Audit Techniques Guide and backed by decades of court precedent. The IRS has published asset classification matrices for retail and service businesses, including nail salons, to standardize which assets qualify and at what recovery periods.