Multifamily investors face a common but costly oversight: depreciating entire apartment buildings over 27.5 years by default. This standard approach leaves substantial tax deductions on the table every year. Cost segregation studies let you reclassify 20% to 40% (sometimes more) of an apartment building's depreciable basis into 5-, 7-, and 15-year property categories, generating front-loaded deductions without changing your total depreciation over time.

This strategy works especially well for multifamily properties because apartment buildings contain abundant short-lived components (appliances, flooring, cabinetry, parking lots, and amenity spaces) that qualify for accelerated depreciation. With 100% bonus depreciation restored under the One Big Beautiful Bill (OBBBA) for property with an acquisition date of January 19, 2025 or later, qualifying investors are seeing average first-year deductions exceeding $171,000. The TCJA phase-down is still in effect for property acquired before January 19, 2025.

Understanding how to capture that benefit starts with knowing what qualifies. This article covers the reclassification percentages multifamily investors can realistically expect, which building components qualify for shorter depreciation lives, and what factors drive those percentages higher or lower on your specific property.

TLDR

- Cost segregation reclassifies components from 27.5-year schedules into 5-, 7-, or 15-year depreciation, accelerating tax deductions

- Apartment buildings typically see 20–40% of depreciable building basis reclassified; luxury properties can reach 40–50%

- Common reclassified items: appliances, flooring, cabinets, parking lots, landscaping, and dedicated electrical systems

- Reclassification percentage depends on property class, amenity density, finish level, and documentation quality

- 100% bonus depreciation allows full first-year deductions on reclassified assets, compressing years of tax savings into year one

What Is Cost Segregation for Multifamily Properties?

Cost segregation is an engineering-based tax strategy that breaks down a multifamily building's components and reclassifies those with shorter useful lives into faster depreciation schedules: personal property (5- or 7-year) and land improvements (15-year), rather than the standard 27.5-year residential schedule. The IRS explicitly sanctions this strategy, established through case law in Hospital Corporation of America v. Commissioner (1997) and guided by IRS Audit Technique Guide 3.20.

The reclassification percentage applies to the building's depreciable basis (purchase price minus land value), not the total purchase price. Land is non-depreciable under IRS rules.

This distinction matters in practice. If 20% of a purchase price is allocated to land, the reclassification math applies only to the remaining 80% allocated to improvements.

Who Benefits Most

Multifamily investors see the greatest impact when they have recently purchased, constructed, or substantially renovated a property valued at $500,000 or more. That said, the strategy isn't limited to new acquisitions:

- Recent purchases or new construction: Maximum reclassification benefit from day one

- Substantial renovations: Newly added components qualify for accelerated schedules

- Properties held multiple years: Look-back studies are available to capture missed deductions in the current tax year via IRS Form 3115, with no amended returns required

What Reclassification Percentages Can Multifamily Investors Expect?

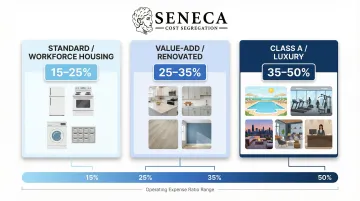

For most apartment buildings, plan on 20–40% of the depreciable building basis being reclassified to shorter depreciation schedules. Amenity-rich, luxury, or heavily renovated properties can push that to 40–50%. Data from Porto Leone Consulting cited by HCVT supports this range, while more conservative estimates for standard multifamily properties place the floor at 15–30%.

Reclassification by Multifamily Subtype

| Property Subtype | Reclassification Range | Key Drivers |

|---|---|---|

| Standard/Workforce Housing | 15–25% | Basic appliances, standard flooring, and minimal common areas produce fewer reclassifiable components, putting these properties at the lower end. |

| Value-Add/Renovated Properties | 25–35% | Recent renovations with detailed invoices push reclassification higher. Kitchen remodels, flooring replacements, and site improvements all create additional opportunities. |

| Class A/Luxury Multifamily | 35–50% | Pools, fitness centers, structured parking, rooftop amenities, and premium unit finishes drive the highest percentages, largely through 15-year land improvement allocations. |

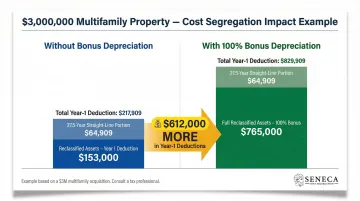

Real-World Example: $3 Million Acquisition

Consider a $3 million multifamily acquisition with 15% allocated to land (building basis = $2.55 million):

| Standard 27.5-Year | 30% Reclassification + Bonus | |

|---|---|---|

| Reclassified basis | — | $765,000 (30% of $2.55M) |

| Remaining 27.5-year basis | $2,550,000 | $1,785,000 |

| First-year deduction | $92,727 | $829,909 |

| Additional deduction | — | +$737,182 |

Across 10,200+ studies, Seneca Cost Segregation clients average a $171,243 first-year deduction, a figure that scales significantly for larger acquisitions.

Critical Mistake to Avoid

The example above illustrates exactly why the calculation basis matters. Investors often apply the reclassification percentage to the full purchase price rather than the building basis after excluding land, which consistently overstates expected deductions. Calculating from the depreciable building basis, rather than the full purchase price, produces accurate deduction estimates.

What Gets Reclassified in a Multifamily Building?

A cost segregation study creates three depreciation "buckets" that contrast against the baseline 27.5-year structural building shell:

- 5-year personal property

- 7-year personal property (less common in multifamily)

- 15-year land improvements

For multifamily properties, most reclassified value lands in the 5-year and 15-year categories.

5-Year Personal Property

These are components that can be removed without damaging the building structure:

- Appliances: Refrigerators, dishwashers, ranges, microwaves, disposals

- Specialty Flooring: Carpet, vinyl plank, removable floor coverings (not ceramic tile or hardwood)

- Cabinetry & Millwork: Kitchen cabinets, bathroom vanities, decorative millwork serving functional purposes

- Window Treatments: Blinds, curtains, decorative tinting

- Dedicated Electrical/Plumbing: Branch circuits serving specific appliances (e.g., 220-volt dryer outlets)

- Common Area Equipment: Fitness equipment, pool furniture, leasing office furnishings

Note: General building lighting does not qualify. Only specialty or decorative lighting fixtures are eligible.

15-Year Land Improvements

These improvements exist outside the building's structural shell:

- Parking lots, driveways, curbs

- Sidewalks and pathways

- Exterior site lighting

- Landscaping and irrigation systems

- Fencing and gates

- Outdoor amenity areas (pool surrounds, outdoor kitchens, dog parks)

- Site drainage systems

Not every component qualifies for accelerated depreciation. The structural building shell stays at 27.5 years regardless of study quality.

What Does NOT Get Reclassified (27.5-Year Property)

- Foundation and load-bearing walls

- Roof systems

- Core HVAC serving the building generally

- Main electrical distribution panels

- Core plumbing risers

- Exterior cladding/siding

Accurate reclassification depends on IRS-compliant engineering analysis, not maximizing the volume of components moved into shorter-life categories.

Existing buildings aren't the only source of reclassifiable basis — renovations open a second window.

Renovation Projects Create Additional Opportunities

Major renovations create a separate segregable basis even on older properties. Kitchen remodels, flooring replacements, and site improvements can be analyzed separately from the original building. Under Treas. Reg. §1.168(i)-8, replaced assets with remaining basis can be written off through partial asset disposition, preventing "ghost depreciation" on replaced components.

What Drives Your Reclassification Percentage Higher or Lower?

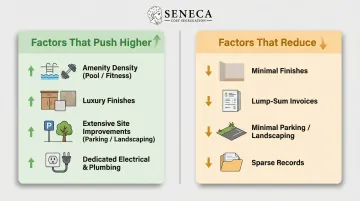

Factors That Push Percentages Higher

| Factor | Impact |

|---|---|

| Amenity-Rich Common Areas | Pools, fitness centers, clubhouses, dog parks, and rooftop areas generate substantial 15-year land improvement allocations. A Class A property with extensive amenities can see 10–15% of basis in land improvements alone. |

| Luxury Unit Finishes | Luxury unit finishes (custom cabinetry, specialty tile, decorative flooring, high-end lighting) push personal property allocations higher. Premium finishes often represent 25–30% of unit costs. |

| Extensive Site Improvements | Large parking lots, extensive landscaping, exterior lighting networks, and perimeter fencing create meaningful 15-year buckets. Structured or underground parking amplifies this further. |

| Dedicated Systems | Electrical or plumbing serving individual unit appliances or amenity spaces (rather than general building power) qualifies for shorter depreciation schedules. |

Factors That Reduce Percentages

| Factor | Impact |

|---|---|

| Basic Finishes and Minimal Amenities | Workforce or affordable housing with basic finishes and minimal amenities typically falls to the 15–20% range, as fewer components means fewer reclassifiable assets. |

| Poor Documentation | Lump-sum invoices or missing records prevent detailed cost attribution. Without itemized contractor invoices, engineers rely on reconstruction methods that produce more conservative estimates. |

| Minimal Site Improvements | Properties with minimal parking or landscaping miss substantial 15-year land improvement opportunities. |

| Sparse Records | Older acquisitions with sparse records require estimation techniques that reduce both precision and reclassification confidence. |

Documentation Quality Matters

Of those four factors, documentation is the one you can control. Engineering-based studies can be completed even with thin records, but detailed documentation produces tighter reclassification estimates that hold up under audit scrutiny. Essential records include:

- Contractor pay applications (AIA Schedule of Values)

- Construction drawings and blueprints

- Itemized invoices showing labor and materials by component

- Change orders and project modifications

- Site surveys identifying land improvements

Documentation files assembled during acquisition and renovation planning, rather than after the fact, yield more complete records.

Timing and Bonus Depreciation

A property acquired when 100% bonus depreciation applies generates far more first-year benefit than the same property in a reduced-rate year. With 100% bonus depreciation restored under the One Big Beautiful Bill for property with an acquisition date of January 19, 2025 or later, completing a cost segregation study in the acquisition year captures the full accelerated deduction for eligible properties, rather than recovering it gradually over the study's life. The TCJA phase-down is still in effect for property acquired before January 19, 2025.

How 100% Bonus Depreciation Amplifies Your Tax Savings

Bonus depreciation is a separate mechanism layered on top of cost segregation. Once assets are reclassified into 5-year or 15-year property, bonus depreciation allows investors to deduct the full value of those assets in the first year rather than over their recovery period.

The Legislative Context

Under the Tax Cuts and Jobs Act (TCJA) of 2017, 100% bonus depreciation was established and then scheduled to phase down. The One Big Beautiful Bill (H.R.1, 119th Congress) restored 100% bonus depreciation for property with an acquisition date of January 19, 2025 or later. The complete bonus depreciation timeline is as follows:

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | TCJA original provision |

| January 1, 2023 – December 31, 2023 | 80% | TCJA phase-down |

| January 1, 2024 – December 31, 2024 | 60% | TCJA phase-down |

| January 1, 2025 – January 18, 2025 | 40% | TCJA phase-down |

| January 19, 2025 – December 31, 2030 (acquisition date January 19, 2025 or later) | 100% | OBBBA restoration |

| 2025 (acquisition date before January 19, 2025) | 40% | TCJA phase-down still applies |

| 2026 (acquisition date before January 19, 2025) | 20% | TCJA phase-down still applies |

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

The Amplification Effect

Using the same $3M multifamily example with a 30% reclassification producing $765,000 in shorter-life assets:

| Without Bonus Depreciation | With 100% Bonus Depreciation | |

|---|---|---|

| Year 1 depreciation on reclassified assets | ~$153,000 (using 5-year 200% declining balance) | $765,000 (full amount) |

| 27.5-year depreciation on remaining basis | $64,909 | $64,909 |

| Total Year 1 | ~$217,909 | $829,909 |

| Difference | — | $612,000 additional first-year deduction |

That $612,000 difference only translates to real savings if you can actually use the deduction, which is where passive activity rules come in.

Passive Activity Loss Limitations

Investors who are not classified as Real Estate Professionals under IRC §469(c)(7) may not be able to apply large depreciation deductions against non-rental income in the same year. Those losses carry forward and can offset future rental income or gains at disposition.

Real Estate Professional (REP) status removes this limitation entirely. To qualify, you must meet all three tests:

- Perform more than 50% of personal services in real property trades or businesses

- Log more than 750 hours of service in those activities annually

- Materially participate in the specific rental activity

When these tests are met, cost segregation deductions can offset active W-2 or business income with no passive loss cap.

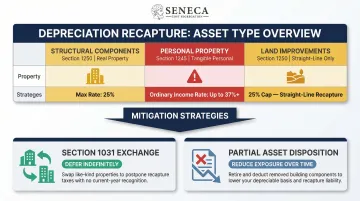

Understanding Depreciation Recapture on Multifamily Properties

Depreciation recapture is the IRS mechanism that "takes back" a portion of the tax benefit when a depreciated property is sold. Understanding the rates and strategies for mitigation is essential for long-term planning.

Recapture Rates by Asset Type

| Asset Type | IRC Section | Recapture Tax Rate |

|---|---|---|

| Structural Components | Section 1250 | Maximum 25% (Unrecaptured Section 1250 Gain) |

| Personal Property | Section 1245 | Ordinary Income at marginal rates (up to 37%) |

| Land Improvements | Section 1250 | Excess over straight-line taxed as ordinary income; straight-line portion capped at 25% |

Critical Point: Recapture is not always 25%. The 25% cap applies to Section 1250 real property, but personal property (5- and 7-year assets) recaptures at ordinary income rates, which can exceed 25% for high-income investors.

Why Recapture Doesn't Eliminate the Benefit

The time value of money means that having additional cash from tax savings today—for years 1 through 10+ of the holding period—is typically more valuable than the increased recapture tax due at sale. Cash saved today can be reinvested into new properties, renovations, or other investments that generate additional returns.

Two strategies can reduce or defer that recapture liability entirely:

- Section 1031 like-kind exchange: defer recapture indefinitely by rolling proceeds into a replacement property

- Partial asset disposition: write off replaced assets during renovations to reduce recapture exposure over time

Strategic Recapture Planning

A well-structured cost segregation study doesn't stop at identifying reclassifiable assets; it models what recapture will look like at exit. Seneca Cost Segregation includes free tax strategy assessments with every study, so investors can weigh recapture exposure against accelerated depreciation benefits before committing to a timeline or exit strategy.

Frequently Asked Questions

What percentage of a multifamily property can be reclassified through cost segregation?

Apartment buildings typically see 20–40% of their depreciable building basis reclassified, with amenity-rich or luxury properties potentially reaching 40–50%. This applies to the building basis (excluding land), not the total purchase price.

What is the typical cost of a cost segregation study?

Study fees vary based on property size and complexity, but the cost is typically a fraction of the first-year tax savings generated. Most investors recover the fee within the first year. A free preliminary analysis from Seneca provides an estimate specific to your property.

Can I write off the cost of a cost segregation study?

Yes, the cost of a cost segregation study is deductible as an ordinary and necessary business expense for existing properties. CPA guidance on the applicable treatment is advisable, as capitalization rules may apply during active construction.

What is 100 percent cost segregation?

"100 percent cost segregation" typically refers to 100% bonus depreciation, a provision reinstated under the One Big Beautiful Bill. It allows investors to deduct the full cost of qualifying 5-year and 15-year reclassified assets in the year those assets are placed in service.

Is depreciation recapture always 25%?

No. The 25% rate is the maximum for Section 1250 (real property) recapture, but personal property reclassified into 5- or 7-year categories (Section 1245) recaptures as ordinary income at your marginal tax rate, which can exceed 25%.

When does a cost segregation study make sense for a multifamily property?

A study typically makes financial sense when the property's depreciable basis is $500,000 or more. The best time is the acquisition year to maximize deductions going forward, but look-back studies on properties held for years can still generate significant catch-up deductions in the current tax year without amending prior returns.

Want to know what your multifamily property qualifies for? Seneca Cost Segregation has completed over 10,200 studies nationwide, with an average first-year deduction of $171,243. Every study uses an engineering-based methodology and comes backed by AuditDefense with a money-back guarantee. A free preliminary analysis is available from Seneca.