Introduction

Data center construction represents one of the most capital-intensive investments in commercial real estate. Between 2020 and 2025, the average global data center construction cost increased from $7.7M to $10.7M per megawatt, with costs projected to reach $11.3M per MW by 2026. These facilities require specialized cooling infrastructure, redundant power systems, precision environmental controls, and dedicated IT equipment. Yet most owners depreciate everything at the default 39-year rate, forfeiting substantial tax savings.

Cost segregation is particularly powerful for data centers because of the extraordinary concentration of qualifying personal property. While a typical office building might yield 20–40% of costs eligible for accelerated depreciation, data centers routinely qualify 40–60% of total construction or acquisition costs for shorter recovery periods.

The restoration of 100% bonus depreciation under the One Big Beautiful Bill Act (OBBBA) makes the timing urgent. Qualifying assets can now be fully deducted in the first year, turning a multi-million-dollar construction cost into immediate tax relief.

What follows covers how cost segregation works specifically for data centers, which assets qualify for accelerated depreciation, and what the study process looks like from start to finish.

TL;DR

- Cost segregation reclassifies data center assets from 39-year life to 5-, 7-, or 15-year recovery periods, sharply accelerating deductions

- Data centers typically qualify 40–60% of total costs for accelerated depreciation — more than almost any other commercial property type

- 100% bonus depreciation means qualifying assets can be fully expensed in year one under current federal law

- Studies should be engaged at acquisition or completion, but existing owners can still benefit through look-back studies

- Skip the engineering-based study and all assets default to 39-year schedules — leaving substantial accelerated depreciation on the table

What Is Cost Segregation for Data Centers?

Cost segregation is a tax strategy that identifies and reclassifies individual building components from real property (39-year life) to personal property (5-, 7-, or 15-year life), allowing depreciation deductions to be taken much sooner. By front-loading deductions, owners reduce taxable income in the early years of ownership, freeing capital for reinvestment or operations.

Data centers differ in one key way from typical commercial real estate in this context. Standard office buildings or retail spaces contain relatively little personal property—perhaps 15–25% of total costs. Data centers, by contrast, pack specialized, depreciable technical infrastructure into every square foot, making the depreciation upside far larger.

A data center's core function depends on systems that serve IT operations rather than general building occupancy. These specialized components qualify for significantly shorter recovery periods than the building shell:

- Precision cooling and environmental monitoring systems

- Dedicated electrical circuits and power distribution units

- Backup power infrastructure (generators, UPS systems)

- Physical security systems and access controls

Why Data Centers Are Prime Candidates for Cost Segregation

Exceptional Concentration of Personal Property

Data centers contain more depreciable personal property per square foot than nearly any other commercial property class. Industry studies show that 60–80% of capital allowances typically qualify for accelerated recovery in jurisdictions with similar classification frameworks.

First-Year Deduction Potential by Investment Size

For every $1M invested in a data center facility, a cost segregation study can generate $200,000–$400,000 in additional first-year deductions compared to straight-line depreciation. A recent case study documented $1.19M in first-year tax savings on an $8.5M depreciable basis—achieved by reclassifying 33.3% to 5-year property, 8.6% to 15-year land improvements, and 22.7% to 15-year qualified improvement property.

100% Bonus Depreciation Restored

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, permanently restored 100% bonus depreciation for assets with a class life of 20 years or fewer placed in service after January 19, 2025. For a data center owner who properly classifies $5M–$10M in qualifying assets, this means taking the entire deduction in year one rather than spreading it over 39 years.

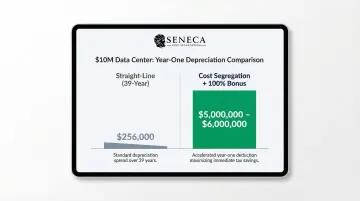

What Happens Without a Study

Without a cost segregation study, that bonus depreciation opportunity disappears entirely. Under straight-line depreciation, all data center assets are lumped into a single 39-year schedule — forfeiting both the time value of money and bonus depreciation eligibility.

| Scenario | $10M Data Center — Year One Deduction |

|---|---|

| Straight-line (39-year) | ~$256,000 |

| Cost segregation + 100% bonus | $5M–$6M |

Current Legislative Urgency

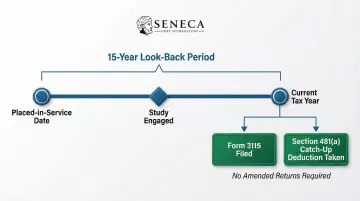

With 100% bonus depreciation now permanent at the federal level, data center investors who delay a study or fail to classify assets correctly are leaving their largest available first-year deduction on the table. The window for retroactive catch-up deductions via Form 3115 is open for 15 years from the property's placed-in-service date.

How a Data Center Cost Segregation Study Works

A proper cost segregation study is an engineering-based analysis that individually itemizes every component of the facility and assigns it to the correct IRS recovery period based on function, not just physical location.

Step 1: Property Review and Document Collection

The study begins with gathering all relevant documentation:

- Construction contracts with line-item cost breakdowns

- Architect and engineer drawings (electrical, mechanical, structural)

- Contractor invoices and equipment specifications

- Purchase agreements and closing statements

The more granular the cost data from the general contractor, the more precise the asset classifications. Invoices that break out cooling systems, power distribution, IT infrastructure, and building shell costs separately enable accurate reclassification.

Step 2: Engineering Site Analysis and Asset Classification

Licensed engineers analyze the facility in person, identifying and categorizing every component by its primary function and applicable IRS class life. This includes dedicated electrical circuits for server loads, precision cooling units, and raised flooring systems.

This site-level detail separates a defensible engineering study from a template-based report. The engineer documents:

- Whether electrical systems serve IT operations or general building functions

- How cooling systems support server environments versus occupant comfort

- Whether raised floors function as cable management pathways or architectural finishes

- Which security systems protect IT assets versus general access control

Each component's classification depends on its documented purpose and technical specifications.

Step 3: Report Delivery, CPA Coordination, and Tax Filing

The completed study report is delivered to the owner and CPA, who use it to claim accelerated depreciation and elect into or out of bonus depreciation by asset class based on broader tax planning priorities.

Seneca Cost Segregation delivers studies within 2–4 weeks and includes AuditDefense with a money-back guarantee, providing documentation support if the IRS reviews the return.

Timing and Look-Back Studies

Cost segregation is most effective when initiated at or shortly after acquisition or construction completion. However, owners of data centers placed in service within the past 15 years can file IRS Form 3115 to catch up on missed depreciation without amending prior returns. The cumulative missed deduction is taken as a Section 481(a) adjustment in the current year.

Which Data Center Assets Qualify for Accelerated Depreciation

5-Year Personal Property (100% Bonus Eligible)

These assets qualify because their primary function serves IT operations, not general building occupancy:

- Server racks and cabinets

- Precision cooling units (CRAC, in-row cooling, hot/cold aisle containment)

- UPS systems and battery backup infrastructure

- Dedicated power distribution units (PDUs) and branch circuits serving IT loads

- Environmental monitoring sensors

- Biometric and security systems protecting server areas

IRS Publication 946 classifies Information Systems (Asset Class 00.12) as 5-year property, including computers and peripheral equipment and related accessories.

15-Year Qualified Improvement Property (QIP)

Interior improvements to an existing building, including:

- HVAC upgrades serving IT environments

- Specialized electrical distribution systems

- Dedicated flooring systems installed as part of renovation

QIP was reclassified to 15-year property by the CARES Act and is eligible for 100% bonus depreciation under current federal law.

Raised Flooring Systems

When installed primarily to support cable management pathways and optimize cooling airflow for IT equipment (rather than serving as architectural flooring), raised floor systems qualify as 15-year property.

IRS Field Service Advice and Revenue Rulings confirm this classification when the floor's function is equipment support rather than building occupancy. Defensible documentation should establish:

- The floor's role in cable routing and airflow management

- That installation was driven by IT infrastructure requirements

- That the floor does not serve general occupancy purposes

What Does NOT Qualify

- Structural building shell and foundation

- Land and site acquisition costs

- Exterior improvements (parking, landscaping)

- Elevators and building-wide transportation systems

- Building expansions

- General-purpose systems serving overall building operations

Allocating costs to these categories without engineering support is one of the most common triggers for IRS scrutiny on data center studies.

State Conformity Caveat

Federal classification sets the foundation — but state treatment can differ significantly. Since the One Big Beautiful Budget Act (OBBBA) made 100% federal bonus depreciation permanent, some states (notably California) do not conform to federal bonus depreciation rules. An engineering-based cost segregation study allows owners to track asset classifications acceptable to both federal and state authorities, preserving maximum flexibility for state filings.

States with confirmed decoupling include:

- California: No conformity to OBBBA bonus provisions

- Oregon: Requires addback of federal deduction and separate state calculation

- Michigan: Reverts to pre-OBBBA rules for state purposes

- Delaware: Decouples for property placed in service after January 19, 2025

Common Misconceptions About Data Center Cost Segregation

"My CPA Already Handles Our Depreciation"

Most CPAs competently handle tax compliance but do not conduct engineering-level component-by-component analysis. Without a dedicated cost segregation study, data center assets are almost always depreciated as a single 39-year asset class, forfeiting all accelerated deductions and bonus eligibility.

Cost segregation requires site inspections, system-by-system functional analysis, and application of IRS precedent to classify components. This specialized engineering work falls outside standard tax preparation services.

"A Cost Segregation Study Will Trigger an IRS Audit"

A well-executed, engineering-based study actually does the opposite: it produces defensible, asset-level documentation that withstands IRS review. The IRS Cost Segregation Audit Techniques Guide explicitly endorses the detailed engineering approach and recommends field inspections as best practice.

What creates audit risk is poor methodology. The IRS distinguishes between:

- Template-based reports that apply generic percentages without property-specific analysis — considered vulnerable to challenge

- Engineering-based studies with contemporaneous cost records and documented site visits — considered "quality" studies by the IRS

The difference comes down to documentation depth, not the existence of the study itself.

"Cost Segregation Only Makes Sense for New Construction"

Data center owners who acquired or built facilities years ago without conducting a study can still benefit. A look-back study filed via Form 3115 captures the cumulative missed depreciation as a catch-up deduction in the current tax year, without requiring amended returns for prior years.

The Section 481(a) adjustment mechanism allows taxpayers to correct their depreciation methodology going forward and claim all previously forfeited deductions in one year. Properties placed in service within approximately 15 years remain eligible.

Frequently Asked Questions

Do data centers depreciate?

Yes, data centers depreciate. The structural building depreciates over 39 years as nonresidential real property. However, the specialized infrastructure inside—cooling, power, IT systems, security—can depreciate over 5, 7, or 15 years through proper cost segregation classification.

Are data centers eligible for bonus depreciation?

Yes. Data center assets with a class life of 20 years or fewer—including servers, precision cooling, backup power systems, and qualified improvement property—are eligible for 100% bonus depreciation, allowing full first-year expensing under current federal law.

What qualifies for 40% bonus depreciation?

40% bonus depreciation referred to the 2025 phase-down rate under the Tax Cuts and Jobs Act before OBBBA. Bonus depreciation was restored to 100% permanently under the One Big Beautiful Bill Act for eligible assets placed in service after January 19, 2025.

Is bonus depreciation 100% for 2026?

Yes. Under OBBBA signed in 2025, 100% bonus depreciation was permanently restored at the federal level for eligible assets placed in service after January 19, 2025. State conformity varies—California, Oregon, Michigan, and Delaware have decoupled.

Is a data center building depreciated over 5 years?

No. The building shell always depreciates over 39 years. Through cost segregation, 40–60% of total costs—the specialized technical infrastructure—can be reclassified to 5-, 7-, or 15-year property, but the building itself is never depreciated over 5 years.

Can I do a cost segregation study on a data center I already own?

Yes. Look-back studies are available for data centers placed in service within approximately the past 15 years. The owner files IRS Form 3115 to claim a catch-up depreciation deduction in the current year without amending prior returns.

Data centers hold some of the largest reclassifiable assets in commercial real estate. Seneca Cost Segregation has completed over 10,200 studies nationwide, delivering an average first-year deduction of $171,243. Our engineering-based methodology, 2–4 week delivery, and AuditDefense guarantee deliver IRS-compliant results—fast. Schedule your complimentary consultation today.