Introduction

Most real estate investors depreciate the entire building as a single asset — 27.5 years for residential, 39 years for commercial. Individual components within that property — carpet, appliances, landscaping, parking lots — qualify for recovery periods as short as 5 or 15 years. Treating everything as one lump asset leaves significant deductions on the table year after year.

This guide is for residential and commercial property owners, rental investors, STR and LTR operators, and anyone looking to reduce taxable income through smarter depreciation strategy.

Component depreciation is an IRS-sanctioned method that can deliver tens of thousands of dollars in front-loaded deductions when applied correctly — not a loophole, but a legitimate tax strategy most investors underuse.

This article covers what component depreciation is, how it differs from standard MACRS depreciation, how the process works in practice, and when it may not suit your portfolio.

TL;DR

- Component depreciation separates individual building parts into IRS asset classes with 5-, 7-, or 15-year recovery periods instead of 27.5 or 39 years

- Front-loaded deductions significantly reduce taxable income in early ownership years

- IRS-compliant under the Modified Accelerated Cost Recovery System (MACRS)

- A cost segregation study is required to qualify components and protect deductions in an audit

- Most impactful on properties valued above $500,000 with significant personal property or land improvements

What Is Component Depreciation in Real Estate?

Component depreciation is the practice of identifying and separating individual physical elements of a property—flooring, lighting, landscaping, appliances—and depreciating each at its own shorter useful life, rather than treating the entire building as a single asset.

Standard MACRS depreciation lumps everything together:

- Residential rental properties: 27.5 years, straight-line

- Commercial properties: 39 years, straight-line

When you depreciate carpet and concrete at the same rate, you're effectively lending money to the IRS interest-free.

The IRS Framework Behind Component Depreciation

MACRS recognizes multiple asset classes for non-structural property components. Under IRC §168, certain elements qualify for 5-year, 7-year, or 15-year recovery periods when classified as tangible personal property (§1245) or land improvements (§1250), rather than structural building components.

This distinction is what makes component depreciation work — and why the asset classification process matters so much.

Component depreciation is not a tax loophole. The IRS explicitly permits it, supported by decades of case law, IRS Publication 946, and the Cost Segregation Audit Techniques Guide. The agency even provides detailed guidance on correct application.

GAAP vs. IRS Tax Treatment

The two frameworks handle depreciation very differently:

| US GAAP (ASC 360) | IRS Tax Treatment | |

|---|---|---|

| Building classification | Single asset unit | Component-level separation |

| Component depreciation | Not required | Actively rewarded |

| Depreciation schedule | Uniform across asset | Multiple recovery periods (5, 7, 15 years) |

| Primary goal | Financial reporting accuracy | Tax liability optimization |

This gap between book and tax depreciation is where real estate investors capture the most value.

Why Real Estate Investors Use Component Depreciation

Front-Loaded Deductions Mean More Cash Now

Component depreciation shifts deductions to the early years of ownership. Instead of writing off $50,000 of carpet and landscaping over 39 years ($1,282 annually), you can depreciate it over 5-15 years ($3,333-$10,000 annually). The difference stays in your pocket, improving cash flow even on profitable rental properties.

Tax Deferral Effect

Larger early deductions reduce taxable income now. This is tax deferral, not elimination—you may owe more at sale due to depreciation recapture—but the time value of money makes earlier deductions far more valuable.

Bonus Depreciation: 100% Deduction in Year One

As of 2025, the One Big Beautiful Bill (P.L. 119-21) permanently restored 100% bonus depreciation for qualified property with a recovery period of 20 years or less acquired and placed in service after January 19, 2025.

That means components reclassified to 5- or 15-year property qualify for 100% bonus depreciation in the first year, allowing investors to deduct the entire cost immediately — a significant amplifier for cost segregation results.

Use Case for Active Investors

Investors who qualify for Real Estate Professional Status (REPS) under IRC §469(c)(7) or the STR exception (average customer use of 7 days or less) can use depreciation losses to offset non-passive income like W-2 wages or business income. Component depreciation amplifies those losses, creating substantial tax savings for active participants.

The Cost of Inaction

Example:

You purchase a $1,000,000 commercial property. $50,000 of that cost is carpet, landscaping, and parking lot improvements.

- Standard approach: Depreciate $50,000 over 39 years = $1,282 annual deduction

- Component depreciation: Depreciate over 5-15 years = $3,333-$10,000 annual deduction

- With 100% bonus depreciation: Deduct the entire $50,000 in year one

The difference in early-year deductions can exceed $30,000-$40,000 on a single property.

How Component Depreciation Works Step by Step

The process has three distinct stages: allocating costs, identifying components through a cost segregation study, and assigning each component its correct MACRS recovery period. Here's how each stage works.

Step 1: Cost Allocation

Break down the total acquisition or improvement cost into four buckets:

- Land (not depreciable)

- Structural building components (27.5 or 39 years)

- Personal property components (5 or 7 years)

- Land improvements (15 years)

This allocation must be defensible and well-documented. The IRS will challenge arbitrary classifications.

Step 2: Component Identification via Cost Segregation Study

A cost segregation study, conducted by a qualified engineering-based firm, is the standard method for identifying and classifying components. The study involves:

- Physical inspection of the property

- Review of construction documents or purchase records

- Engineering analysis to separate costs qualifying for shorter recovery periods

That engineering analysis typically uncovers more reclassifiable cost than most property owners expect. According to ASCSP case studies, approximately 20% of a residential property's basis, 25% of a commercial property's basis, and 30% of an industrial property's basis can be reclassified into 5-year and 15-year categories.

Step 3: Assign Recovery Periods and Report

Each classified component receives:

- Its IRS-prescribed MACRS recovery period

- The appropriate depreciation method (for example, 200% declining balance for 5/7-year, straight-line for 27.5/39-year)

- Listing on Form 4562

Replacement components receive a new placed-in-service date and begin their own depreciation schedule.

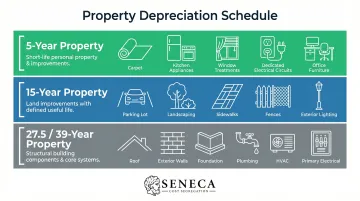

Common Property Components and Their Depreciation Timelines

5-Year Property

- Carpet

- Appliances (refrigerators, dishwashers)

- Window treatments

- Dedicated electrical branch circuits serving appliances

- Furniture and fixtures not permanently affixed

These are tangible personal property elements (§1245) that can be removed without structural damage.

15-Year Property

- Parking lots

- Landscaping

- Sidewalks and walkways

- Fences

- Exterior lighting

- Underground utilities

These are land improvements (asset class 00.3)—separate from the building but affixed to the land.

What Stays at 27.5 or 39 Years

Structural components integral to the building fall into the longest recovery periods:

- Roof

- Exterior walls

- Foundation

- Plumbing systems

- Primary HVAC systems

- Primary electrical distribution

Scale matters here. Replacing one furnace in a three-furnace HVAC system is not considered a replacement of a major component and may not need to be capitalized as a structural restoration. But when a replacement restores a substantial structural part of the building, it typically depreciates over 27.5 years — the determining factor is whether the work rises to the level of a structural restoration.

Classification Criteria

The IRS applies a function and permanence test to determine asset class. In practice, two questions drive the classification:

- Can it be removed without structural damage? If yes, it's more likely to qualify for a 5- or 15-year recovery period.

- Does it serve a specific piece of equipment or the building as a whole? Dedicated systems (like electrical circuits wired solely for appliances) qualify as 5-year property, while building-wide systems do not.

Getting this classification right is where engineering-based cost segregation studies earn their value — the line between a 5-year component and a 39-year structural element can be worth tens of thousands of dollars in accelerated deductions.

Misconceptions About Component Depreciation (and When It May Not Apply)

Misconception 1: "This only works for large commercial properties"

Component depreciation applies to any income-producing real estate. The economic benefit is more significant on higher-value properties where tax savings justify the cost of a study, but even properties with a $300,000 building basis (excluding land) can see meaningful returns. Seneca Cost Segregation reports an average first-year deduction of $171,243 across completed studies.

Misconception 2: "You can reclassify anything you want under a shorter life"

Misclassification invites IRS scrutiny. All classifications must be defensible under MACRS guidelines and supported by documentation. The IRS has assessed penalties under IRC §6701 against engineers who mischaracterized 39-year components as 5-year property, resulting in $1,000 penalties per individual return and $10,000 per corporate return. The Cost Segregation Audit Techniques Guide outlines 13 principal elements of a "quality" study, including preparation by qualified individuals, detailed methodology descriptions, and appropriate contemporaneous documentation — which is exactly why engineering-based studies are the IRS-preferred approach.

When Component Depreciation May Not Make Sense

Compliance isn't the only filter — sometimes the economics simply don't justify a study. Three situations where component depreciation typically falls short:

- Low building basis: Properties below $300,000 in building value (excluding land) may not generate enough tax savings to offset professional fees.

- Short hold periods without a 1031 exchange: Selling within 1-2 years triggers depreciation recapture, which can erode the gains — especially without a tax-deferral strategy in place.

- Few reclassifiable components: Older buildings with updated interiors or properties on small lots with minimal landscaping offer limited opportunity to shift costs to shorter depreciable lives.

Conclusion

Component depreciation is a legitimate, IRS-sanctioned approach that allows real estate investors to accelerate deductions by treating building components as individual assets with their own recovery periods. When done correctly, it can meaningfully reduce taxable income in the years that matter most—often delivering six-figure deductions in year one with 100% bonus depreciation.

Proper implementation requires defensible documentation and correct classification, not just good intentions. Investors should work with an ASCSP-credentialed cost segregation firm like Seneca Cost Segregation to conduct an engineering-based study that identifies every eligible component, supports IRS compliance, and includes AuditDefense with a money-back guarantee.

With over 12 years of experience, more than 10,200 properties assessed nationwide, and licensed professional engineers on staff, Seneca delivers studies completed within 2-4 weeks that can withstand IRS scrutiny.

The cost of inaction is measurable: Seneca clients average $171,243 in first-year deductions. Every year without a cost segregation study is a year of recoverable savings that's gone for good.

Frequently Asked Questions

Frequently Asked Questions

What is component depreciation in real estate?

Component depreciation separates a property's individual elements (carpet, appliances, landscaping) and depreciates each at its own IRS-prescribed recovery period (5, 7, or 15 years), rather than treating the entire building as one asset over 27.5 or 39 years.

What is component depreciation and when must it be used?

It's an elective strategy, not a requirement — investors choose to use it when they want to accelerate deductions. A cost segregation study is typically required to identify, classify, and document components eligible for shorter recovery periods.

How does property depreciation work?

The IRS allows property owners to deduct a property's cost over its useful life using MACRS (residential: 27.5 years, commercial: 39 years). Component depreciation is a strategy within that framework, enabling faster write-offs for qualifying elements by reclassifying them into shorter recovery periods.

Does US GAAP allow component depreciation?

US GAAP generally does not require component depreciation for buildings, treating them as a single unit for financial reporting. In contrast, IRS tax rules actively support and incentivize component depreciation through MACRS asset class definitions.

What are the three types of depreciation in real estate?

The three types are physical deterioration (wear and tear over time), functional obsolescence (outdated design or systems), and economic obsolescence (external factors reducing value). Tax depreciation through MACRS is how investors recover these costs on their returns.

How many years do you depreciate electrical work?

Structural electrical wiring is typically depreciated over 27.5 years (residential) or 39 years (commercial). Specific components serving personal property uses, like dedicated appliance circuits, may qualify for a 5-year recovery period through component depreciation.