Introduction

Commercial tenants spend an average of $139 per square foot transforming bare rental spaces into functional, branded environments, yet most don't fully own what they're building. These interior upgrades, known as leasehold improvements, legally belong to the landlord and revert to the property at lease end, creating unique accounting, tax, and negotiation challenges for both parties.

Whether you're a tenant planning a build-out, a landlord structuring a concession package, or a real estate investor managing depreciation, leasehold improvements affect your bottom line. This guide covers:

- What leasehold improvements are (and what they aren't)

- Who pays and how tenant improvement allowances work

- Accounting treatment under ASC 842

- Tax rules after the TCJA and CARES Act

- How leasehold improvements differ from building improvements

TLDR

- Leasehold improvements are interior alterations made to leased space for a specific tenant's needs

- Funding comes from landlords (via TIA, build-out allowance, rent discount, or turnkey) or tenants directly

- Capitalized as long-term assets and amortized over the shorter of useful life or remaining lease term

- Qualify as 15-year Qualified Improvement Property (QIP), making them eligible for bonus depreciation

- Write off remaining net book value as a loss at lease end or early termination

What Are Leasehold Improvements?

Leasehold improvements are customizations or alterations made to the interior of a leased building to suit a specific tenant's operational or business needs. Also called "tenant improvements" or "build-outs," these modifications can be initiated by either the landlord or the tenant, depending on the lease terms.

Ownership Dynamics

Even though the tenant benefits from (and often pays for) leasehold improvements, the improvements legally belong to the landlord and revert to the property at lease end. This ownership dynamic drives both accounting treatment and tax classification.

What Qualifies as a Leasehold Improvement

Improvements must meet specific criteria:

- Attached to the building (not moveable)

- Made to the interior of the leased space

- Designed for one specific tenant's use

- Placed in service after the building was first placed in service

What does NOT qualify:

- Moveable furniture, freestanding equipment, or personal property removable without structural damage

- Exterior building changes or structural enlargements

- Common area renovations benefiting multiple tenants

- Routine repairs for normal wear-and-tear

- Whole-building HVAC systems, roofs, elevators, escalators

- Fire protection, alarm, and security systems at the building level

Common Examples of Leasehold Improvements

Interior structural work:

- Installing or removing partition walls to divide open space into offices

- Adding drop ceilings or modifying doorways

- Reconfiguring space layout for specific departments

Finishing and fixture upgrades:

- Painting, wallcovering, or decorative finishes

- Replacing or installing new flooring (carpet, hardwood, tile)

- Upgrading lighting fixtures

- Adding plumbing or restroom facilities

Industry-specific installations vary widely by tenant type. Common examples include retail display shelving with integrated electrical, service counters and point-of-sale areas, dedicated server rooms with raised flooring, and restaurant kitchen plumbing and ventilation systems.

Who Pays for Leasehold Improvements?

Because leasehold improvements ultimately remain with the property and benefit the landlord long term, landlords often fund or partially fund these improvements, particularly to attract quality tenants or extend lease terms. Tenants may pay when improvements are highly specific to their use or when landlords lack the capital. The specific arrangement depends on which of the four structures below the parties agree to at signing.

According to CBRE data, average tenant improvement allowances dropped to $87.51 per square foot in 2024, down from $97.55 in 2023, as financially strained building owners pulled back on concessions amid high interest rates. Meanwhile, Cushman & Wakefield reports average fit-out costs reached $139 per square foot, creating a $51 gap that tenants must bridge through out-of-pocket spending or extended lease terms.

Funding Structure Comparison

| Funding Structure | Who Controls Project | Who Pays Cost Overruns | Typically Used When |

|---|---|---|---|

| Tenant Improvement Allowance (TIA) | Tenant | Tenant | Competitive office and retail markets |

| Build-Out / Building Standard Allowance | Landlord | Tenant (for upgrades beyond standard) | Landlord manages project; tenant wants reduced project management burden |

| Rent Discount | Tenant | Tenant | Landlords want to preserve cash / have limited liquidity |

| Turnkey Project | Landlord | Landlord | High-value, long-term leases with creditworthy tenants |

Tenant Improvement Allowance (TIA)

The landlord provides a set dollar amount, typically calculated per square foot, and the tenant manages the entire project. Key characteristics:

- Tenant controls design, contractor selection, and timeline

- Tenant is responsible for any cost overruns beyond the agreed allowance

- Most common arrangement in competitive office and retail markets

Build-Out / Building Standard Allowance

The landlord offers a predefined package of improvements at no cost to the tenant. Characteristics include:

- Standard finishes: basic flooring, paint, lighting, and fixtures

- Landlord manages the project and contractor relationships

- Tenants wanting upgrades beyond the standard package pay the difference

- Reduces tenant's project management burden

Rent Discount

The landlord offers rent-free months or reduced rent for a set period, and the tenant applies those savings toward funding their own improvements. This works well when landlords want to preserve cash:

- Tenant bears full responsibility for costs and project management

- Provides maximum design flexibility but requires upfront capital

- Common in markets where landlords have limited liquidity

Turnkey Project

The tenant submits a detailed improvement proposal with plans and cost estimates. Once the landlord approves it, they fund and oversee all construction, delivering a move-in-ready space. Because the landlord absorbs all cost and project risk, this option is typically reserved for high-value, long-term leases with creditworthy tenants.

How Are Leasehold Improvements Accounted For?

Capitalization

Once an improvement is made, its total cost is recorded as a long-term (fixed) asset on the balance sheet, not expensed immediately. Capitalized costs include:

- Construction and materials

- Design and architectural fees

- Permit costs

- Other directly attributable costs

Note: Improvements below a company's internal capitalization threshold (often $2,500 to $5,000) may be expensed in the current period rather than capitalized.

Amortization

Under ASC 842-20-35-12, the capitalized cost is amortized over the shorter of:

- The estimated useful life of the improvement, or

- The remaining lease term

Salvage value is assumed to be zero because the asset reverts to the landlord at lease end.

Worked Example:

A tenant spends $200,000 on leasehold improvements with a 40-year useful life under a 10-year lease. Because the lease term (10 years) is shorter than the useful life (40 years), amortization is calculated as:

$200,000 ÷ 10 years = $20,000 per year

Annual journal entry:

Debit: Amortization Expense $20,000

Credit: Accumulated Amortization – Leasehold $20,000

Lease Renewal Consideration

If renewal is reasonably certain at lease inception, the amortization period may extend to cover the renewed term — provided it doesn't exceed the improvement's useful life. Factors that typically support this determination include:

- A signed renewal option at below-market rent

- Significant remaining improvement value

- Documented operational necessity at that location

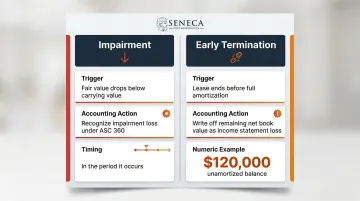

Impairment and Early Termination

Two scenarios require immediate accounting action:

| Scenario | Accounting Treatment |

|---|---|

| Impairment (fair value drops below carrying value) | Recognize an impairment loss under ASC 360 in the period it occurs |

| Early termination (lease ends before full amortization) | Write off the remaining net book value as a loss on the income statement |

For example, if $120,000 in unamortized improvements remain when a lease terminates early, the tenant records a $120,000 loss immediately.

Tax Treatment and Depreciation of Leasehold Improvements

Legislative History: From PATH Act to TCJA to CARES Act

Step 1 – PATH Act (2015)

The PATH Act (2015) established a 15-year straight-line cost recovery period for qualified leasehold improvements.

Step 2 – Tax Cuts and Jobs Act (TCJA) of 2017

The Tax Cuts and Jobs Act (TCJA) of 2017 replaced that category with "Qualified Improvement Property" (QIP), removing the related-party restriction and the three-year waiting period. Improvements now qualify as soon as they are made to an already-in-service building's interior.

However, the TCJA contained a drafting error that inadvertently assigned QIP a 39-year recovery period, making it ineligible for bonus depreciation.

Step 3 – CARES Act (2020)

The CARES Act (2020) corrected this error, officially assigning QIP a 15-year recovery period and making it eligible for 100% bonus depreciation, meaning the entire cost of qualifying interior improvements could be deducted in the first year.

Current Bonus Depreciation Phase-Down

While QIP qualifies for bonus depreciation, the percentage is phasing out under the TCJA:

| Period | Bonus Depreciation |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 | 100% (if acquisition date is January 19, 2025 or later) |

If acquisition date is before January 19, 2025:

- 40% bonus depreciation applies in 2025

- 20% bonus depreciation applies in 2026

Accelerating planned interior renovations captures remaining bonus depreciation before it fully expires; Section 179 expensing is available as an alternative for qualifying property.

What Does NOT Qualify as QIP

The IRS explicitly excludes from QIP treatment:

- Roofs

- HVAC systems

- Fire protection systems

- Alarm and security systems

- Elevators and escalators

- Internal structural framework

- Building enlargements

These components default to 39-year nonresidential real property depreciation.

Maximizing Tax Benefits Through Cost Segregation

A professional cost segregation study can analyze leasehold improvements and identify components that qualify not just for the 15-year QIP category, but potentially for even shorter 5- or 7-year personal property lives, which can dramatically accelerate depreciation deductions.

Firms like Seneca Cost Segregation use an engineering-based methodology to ensure every qualifying component is captured. Their licensed engineers conduct detailed on-site inspections, review architectural drawings, and apply industry-standard cost databases to identify components such as:

- Removable partitions and modular wall systems (5-year)

- Decorative lighting and specialized task lighting (5-year)

- Specialized electrical serving retail displays or equipment (5-year)

- Dedicated plumbing for process-specific functions (5-year)

- Custom cabinetry and built-in fixtures (5-year)

This approach often converts a significant portion of improvement costs into immediate first-year deductions while maintaining full IRS compliance. Seneca's studies are backed by their AuditDefense guarantee, which provides complete IRS representation at no additional charge if an audit occurs. With over 12 years of experience and 10,200+ properties assessed, their average client captures $171,243 in first-year deductions.

Leasehold Improvements vs. Building Improvements

Key Distinction

Leasehold improvements benefit only one specific tenant and are limited to the interior of the leased space. Building improvements, by contrast, benefit all occupants, enhance or extend the life of the entire structure, and affect the building as a whole, regardless of tenancy.

Examples of Building Improvements (Not Leasehold)

- Installing a new roof

- Upgrading whole-building HVAC systems

- Adding or repairing an elevator

- Repaving a parking lot

- Renovating a shared lobby

- Adding a new building wing

Tax Treatment Comparison

| Improvement Type | Recovery Period | Bonus Depreciation Eligible |

|---|---|---|

| Leasehold (QIP) | 15 years | Yes (phasing out) |

| Building Improvements | 39 years | Generally no |

Getting this distinction right has real tax consequences. Structural upgrades (roof, elevators, and shared systems) funded through turnkey delivery or base building budgets keep the tenant's Tenant Improvement Allowance (TIA) dollars focused on 15-year QIP interior work, where bonus depreciation is available and the tax benefit is far greater.

Frequently Asked Questions

Can you make changes to a leasehold property?

Yes, tenants can make changes, but typically require landlord approval, especially for permanent interior alterations. Lease agreements usually specify the type and scope of changes permitted and determine who pays and what happens to improvements at lease end.

What happens to leasehold improvements at the end of a lease?

Leasehold improvements generally revert to the landlord at lease end at no cost. From an accounting standpoint, any remaining unamortized book value is written off as a loss. Some lease terms may require the tenant to restore the space to its original condition before vacating.

What are examples of leasehold improvements?

Common examples include painting and wallcovering, installing partition walls or ceilings, new flooring (carpet or tile), upgraded lighting, plumbing additions, display shelving, security systems, and office reconfiguration: any interior, permanently attached alteration made for a specific tenant's use.

Who pays for leasehold improvements: landlord or tenant?

Either party can pay depending on the lease terms negotiated. Common landlord-funded arrangements include tenant improvement allowances, build-out packages, and rent discounts. Tenants may fund improvements themselves if they are highly specific to their operations or if the landlord is unwilling to cover the cost.

Are leasehold improvements tax deductible?

Leasehold improvements cannot be directly deducted as an expense. However, qualifying improvements (known as Qualified Improvement Property or QIP) are eligible for a 15-year cost recovery period and bonus depreciation, which lets owners recover much of the cost in the year the improvement is placed in service.

What is the difference between leasehold improvements and building improvements?

Leasehold improvements are interior changes that benefit one specific tenant. Building improvements affect the entire structure and benefit all occupants, such as a new roof or HVAC upgrade. Building improvements are typically depreciated over 39 years, compared to the 15-year schedule for qualified leasehold improvements.