Understanding what drives pricing up or down, how fee structures work, and how to calculate whether a study delivers positive ROI is essential before committing to any provider. This article breaks down typical cost ranges, explains the key factors that affect pricing, compares flat-fee and contingent-fee models, and provides the framework you need to determine if a study is worth it for your property.

TL;DR

- Typical cost range: Studies generally run $4,000–$15,000 for residential and small commercial properties, up to $40,000–$60,000+ for large-scale commercial properties

- Key price drivers: Property value, building complexity, provider methodology (engineering-based vs. invoice-based), and professional credentials

- ROI benchmark: Most quality studies return 3–10x their cost in first-year tax savings for investors who can deploy the accelerated losses

- Best fit for properties with a depreciable basis above $300K–$500K, high-bracket investors, and long-term hold strategies

How Much Does a Cost Segregation Study Cost?

Cost segregation study fees vary based on property type, square footage, depreciable basis, and the level of engineering analysis required. Misunderstanding these ranges leads to predictable mistakes: underbudgeting for high-value properties or overpaying for unnecessary complexity on smaller assets. Some investors dismiss cost segregation entirely due to sticker shock — without ever calculating the actual return on investment.

Typical Cost Ranges by Property Value

| Property Value / Depreciable Basis | Typical Fee Range | What's Included |

|---|---|---|

| Under $500K | $495–$2,500 | Streamlined remote analysis, basic documentation |

| $500K–$1.5M | $2,500–$15,000 | Engineering-based review, construction document analysis, component reclassification |

| $1.5M–$3M | $10,000–$20,000 | Detailed engineering takeoff, site inspection, comprehensive audit documentation |

| $3M–$10M | $20,000–$40,000 | Full engineering analysis, multi-building or complex-use properties |

| $10M+ | $40,000–$60,000+ | Large commercial/industrial portfolios, extensive documentation |

What's typically included: Quality providers deliver construction document and cost record review, component-level asset reclassification, bonus depreciation identification, a written report reconciling allocated costs to actual total costs, and audit-defense documentation.

What's typically NOT included: CPA or tax advisor fees to implement the study results in your tax filings, amended return preparation fees for retroactive lookback studies, or consulting for related strategies like Section 179D energy deductions or 45L tax credits.

Entry-Level Studies (Smaller Residential or STR Properties)

These studies serve single-family rentals, small short-term rental (STR) properties, and buildings with a depreciable basis under $500K. Entry-level studies use streamlined virtual or remote methodologies to keep costs accessible.

The tradeoff: less comprehensive documentation can be harder to defend in an IRS audit. That said, modern flat-fee providers have lowered the viable threshold to properties with a depreciable basis of $150,000 or more — especially relevant with the return of 100% bonus depreciation.

Mid-Range Studies (Multi-family, Small Commercial)

This is the most common tier for real estate investors. Moving up from entry-level, properties in this range include:

- Multi-family properties (duplexes, triplexes, small apartment complexes)

- Small commercial buildings ($1M–$3M depreciable basis)

- Mixed-use properties with moderate complexity

Engineering-based studies in this tier offer the best balance of cost and IRS defensibility. Providers typically conduct site visits (virtual or in-person), review construction documents, and deliver comprehensive reports that meet the IRS's 13 principal elements for quality studies.

High-End Studies (Large Commercial, Industrial, or Mixed-Use)

At this tier, the scope expands significantly. Properties that typically fall here include:

- Large apartment complexes and commercial office facilities

- Manufacturing plants and industrial buildings

- New construction projects with complex component structures

In-person site visits, extensive engineering analysis, and comprehensive documentation justify the higher fees. For properties over $5M in depreciable basis, the study cost is often less than 1% of the first-year deduction generated — making it a straightforward financial decision.

Key Factors That Affect the Cost of a Cost Segregation Study

The price of a cost segregation study reflects the work required to accurately break down and reclassify property components — and several factors determine how complex that work gets.

Property Value and Depreciable Basis

Higher-value properties contain more components to analyze, more documentation to review, and more at stake for IRS compliance — all of which increase study complexity and cost. The depreciable basis (property cost minus land value) is often the primary driver of study fees. A $10M building contains exponentially more line items, systems, and specialized components than a $500K property.

Property Type and Complexity

Property type shapes the scope of analysis as much as property value does. A simple warehouse requires far less work than a medical office building, hospitality property, or multi-use commercial facility. Properties with specialized equipment, custom tenant buildouts, or unique building systems — HVAC zoning, specialized electrical, complex plumbing — take longer to classify correctly.

Typical reclassification percentages by property type:

- Apartment/Multi-family: 20%–50% of basis reclassified to shorter schedules

- Hotels/Hospitality: 25%–45%

- Manufacturing: 25%–60%

- Office buildings: 10%–40%

- Warehouses: 10%–30%

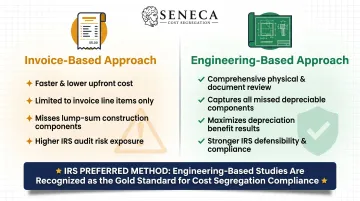

Methodology: Engineering-Based vs. Invoice-Based

The methodology your provider uses determines both the cost of the study and the size of your deductions. The two core approaches differ substantially in accuracy and IRS defensibility:

Invoice-based approach:

- Faster and cheaper

- Only captures costs that appear as line items on invoices

- Misses reclassifiable components buried in lump-sum contractor costs

- Higher audit risk due to incomplete documentation

Engineering-based approach:

- Examines the physical building, construction documents, and cost records

- Identifies components that an invoice-only review would miss

- Produces larger depreciation benefits that routinely outweigh the higher study fee

- Stronger IRS defensibility

The IRS Cost Segregation Audit Techniques Guide explicitly states that a "detailed engineering approach from actual cost records" is the "most methodical and accurate approach." The IRS also warns examiners to view "rule of thumb" approaches — estimating personal property as a fixed percentage without documentation — with caution.

Provider Credentials and Expertise

Credentials matter beyond price. Firms with ASCSP-certified Certified Cost Segregation Professionals (CCSPs) and licensed engineers on staff typically charge more — but produce studies that are more thorough and far more defensible under audit.

CCSP credential requirements:

- Minimum 7,000 hours of direct cost segregation experience over 7 years

- Comprehensive exam covering tax law, engineering methodology, and IRS compliance

- Peer-reviewed application process with sample report review

- Only ASCSP Certified Members are permitted to certify reports

Providers without recognized credentials may offer lower prices but create audit exposure and often miss deductions that engineering-based analysis would capture.

Geographic Location and Site Visit Requirements

Studies requiring in-person site inspections add travel-related costs. This is common for larger or more complex commercial properties. Virtual or remote studies may work for simpler residential properties, but large commercial assets need physical inspection to accurately classify specialty systems and improvements.

How Cost Segregation Studies Are Priced: Flat Fee vs. Contingent

Two primary fee structures dominate the industry: flat fees and contingent fees. Understanding the difference is critical to avoiding costly mistakes.

Flat fees are a fixed amount agreed upon before the study begins based on estimated scope. This provides cost certainty and aligns the provider's incentive with doing the work correctly, not just finding more savings.

Contingent fees are calculated as a percentage of the tax savings identified by the study. This creates incentives for inflated benefit projections to justify higher fees — or situations where the fee consumes a disproportionate share of actual tax savings.

| Fee Structure | Industry Guidance | Compliance & Ethics |

|---|---|---|

| Contingent | Prohibited by ASCSP Code of Ethics (Article 2.12) for Federal Income Tax Depreciation services | IRS ATG directs examiners to "closely scrutinize" contingency fees; creates incentives to maximize short-life property through aggressive interpretations |

| Flat/Fixed | Recommended industry standard | Based on project scope, complexity, time, and materials |

Reputable providers offer flat-fee arrangements based on property complexity — ask for one upfront. Before committing, compare the total fee against a conservative estimate of expected tax savings to confirm the study pencils out.

Seneca Cost Segregation structures all studies on a flat-fee basis, completed in 2–4 weeks, with an average first-year deduction of $171,243 across more than 10,200 properties assessed nationwide.

Is the Cost of a Cost Segregation Study Worth It?

ROI on a cost segregation study is a math problem, not a judgment call. Use this framework to run the numbers before commissioning a study.

The ROI Calculation That Matters

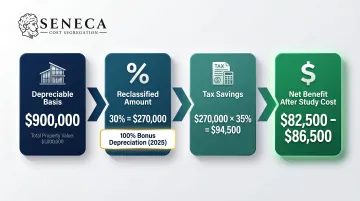

Basic formula: (Estimated first-year tax savings) − (Study cost) = Net benefit

Realistic example using a $1M property:

- Depreciable basis (building only): $900,000

- Estimated reclassification: 30% = $270,000 to shorter schedules

- Investor tax rate: 35% (federal + state)

- Bonus depreciation (2025 onward): 100%

Year-one calculation:

- Accelerated deduction: $270,000 × 100% = $270,000

- Tax savings: $270,000 × 35% = $94,500

- Typical study cost for $1M property: $8,000–$12,000

- Net benefit: $82,500–$86,500 in year one

Seneca Cost Segregation clients achieve an average first-year deduction of $171,243 across their portfolio of 10,200+ completed studies. Using the same 35% tax rate, this translates to approximately $60,000 in year-one tax savings — a strong multiple over typical study costs.

When the Math Works in Your Favor

A cost segregation study clearly delivers strong ROI when:

- Property depreciable basis is above $300K–$500K

- Investor is in a high tax bracket (30%+ combined federal and state)

- Investor can use accelerated depreciation losses:

- Material participation in a short-term rental (STR loophole)

- Real Estate Professional Status (REPS)

- Passive income from other sources to offset

- Long-term hold strategy (5+ years) that avoids near-term depreciation recapture

When the Math Doesn't Add Up

A study may not be worth the cost when:

- Smaller properties where the fee consumes most potential savings

- Passive investors with no offsetting passive income and no ability to use losses

- Very low effective tax rates

- Short hold periods (under 2–3 years) where recapture at sale substantially erodes the time-value benefit

Short hold periods deserve a closer look, because the recapture mechanics can meaningfully change the outcome.

Hold Period and Depreciation Recapture

Cost segregation is a time-value-of-money strategy: it accelerates deductions now at the cost of smaller deductions later and potential recapture tax upon sale.

Two recapture rules apply at sale:

- Section 1245 applies to personal property (5- and 7-year assets) — gain is taxed as ordinary income up to the total depreciation previously taken

- Section 1250 applies to real property — unrecaptured gain is taxed at a maximum rate of 25%

Investors with a short hold period need to model the recapture cost against near-term savings before deciding to proceed. For hold periods under 2–3 years, the ordinary income tax triggered by Section 1245 recapture may largely offset the initial present-value benefit.

Common Mistakes When Evaluating Cost Segregation Study Costs

Three errors consistently reduce the ROI of a cost segregation study — and all three are avoidable with a bit of upfront diligence.

- Choosing price over credentials: A low-cost study using an invoice-based approach or lacking CCSP-certified professionals can miss significant deductions and create audit risk — costing far more than the fee you saved.

- Underestimating implementation costs: The study fee is only part of the investment. Factor in CPA time to incorporate results into your filings, particularly for retroactive lookback studies requiring amended returns and Form 3115 accounting method changes.

- Not confirming you can use the losses first: Passive investors unable to offset losses against active income may carry them forward indefinitely, gutting the study's effective ROI. Confirm your tax classification with an advisor before ordering.

Frequently Asked Questions

How much does a cost segregation study typically cost?

Studies generally range from $4,000 to $15,000 for most residential and small commercial properties. Large commercial assets can reach $40,000–$60,000+. Cost depends on property size, complexity, and provider methodology (engineering-based vs. invoice-based).

Does a cost segregation study have to be done by a professional?

There's no legal requirement, but the IRS expects engineering-based analysis and detailed documentation to support reclassifications. Studies prepared by unqualified providers are difficult to defend in an audit and may not capture the full available benefit.

Are cost segregation studies worth it?

For most property owners with a depreciable basis above $300K–$500K who can use the accelerated depreciation losses, studies generate 3–10x their cost in first-year tax savings. The answer depends on your tax situation, hold period, and ability to use the losses.

How long do you depreciate an office building?

Commercial office buildings are depreciated over 39 years under standard IRS rules. A cost segregation study reclassifies components within the building to shorter 5-, 7-, or 15-year schedules, significantly front-loading early-year deductions.

What is the $2,500 expense rule?

The IRS de minimis safe harbor rule allows taxpayers to immediately deduct items costing $2,500 or less per invoice or item ($5,000 with an applicable financial statement). This can work alongside cost segregation to expense lower-cost building components rather than capitalizing and depreciating them.