Introduction

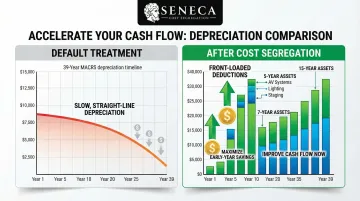

Event and meeting facility owners face a costly oversight: properties loaded with high-value, short-lived assets—AV systems, specialty lighting, staging infrastructure, custom finishes, commercial kitchens—are routinely lumped into a single 39-year depreciation schedule. This default treatment ignores the true useful life of these components and costs owners years of legally entitled tax savings.

Without a cost segregation study, the entire facility defaults to nonresidential real property treatment under MACRS (the IRS depreciation system), treating everything from carpet to AV cabling to patio pavers identically. Event venues are deliberately built for sensory experience and operational flexibility, meaning a disproportionately large share of construction costs go toward non-structural elements that qualify for accelerated depreciation — often 30% to 50% of total project costs.

With 100% bonus depreciation restored for property placed in service after January 19, 2025, qualifying assets can now be fully deducted in the first year rather than stretched across decades.

This article explains why event and meeting facilities are among the most asset-rich property types for cost segregation, what specifically qualifies, how the current tax environment amplifies the benefit, and what to look for in a qualified study provider.

TLDR

- Cost segregation reclassifies short-lived components into 5-, 7-, and 15-year classes instead of 39 years, sharply accelerating depreciation deductions

- Event facilities contain high concentrations of qualifying assets: AV systems, specialty lighting, staging, commercial kitchens, outdoor hardscaping, and modular furnishings

- 100% bonus depreciation for property placed in service after January 19, 2025 enables full first-year write-offs

- Look-back studies let existing facility owners catch up on missed depreciation without amended returns

- Choosing an engineering-based, IRS-compliant provider protects deductions under audit and ensures no qualifying asset is left on the table

Why Event and Meeting Facilities Are Prime Cost Segregation Candidates

Without a cost segregation study, the entire facility—from carpet to AV cabling to patio pavers—defaults to a single 39-year depreciable life under MACRS nonresidential real property rules. That treatment ignores the true short useful life of many components and delays deductions owners are legally entitled to claim now.

Asset-Dense by Design

Event and meeting facilities are far more asset-dense than standard office or retail buildings. They are deliberately built for sensory experience and operational flexibility, meaning an outsized share of construction costs go toward non-structural elements:

- Lighting systems for ambiance and presentation

- Acoustical treatments for speech clarity

- Technology infrastructure for hybrid events

- Guest-facing finishes that create memorable experiences

- Furniture, fixtures, and movable equipment that turn over frequently