But here's the critical insight: cost segregation isn't a one-size-fits-all tool. Certain industries, due to the nature of their building components, specialized equipment, and improvement-heavy interiors, generate far greater tax savings than others. Understanding which property types yield the highest returns helps investors prioritize where to deploy this powerful tax strategy first.

TL;DR

- Cost segregation reclassifies building components to 5-, 7-, or 15-year depreciation schedules instead of 27.5 or 39 years

- Industries with specialized equipment, heavy tenant improvements, or process-specific buildouts capture the largest reclassification opportunities

- Top performers include multifamily real estate, short-term rentals, hospitality, healthcare, manufacturing, and restaurants

- Properties with $1 million+ cost basis typically generate the strongest ROI

- Investors working with an engineering-based provider can average $171,243 in first-year deductions. Seneca Cost Segregation has delivered this across 10,200+ properties nationwide

What Is Cost Segregation and Why Does It Matter for Property Owners?

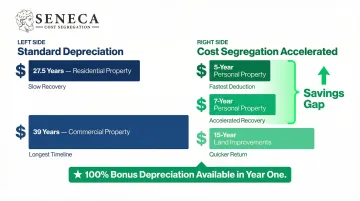

Cost segregation is an IRS-approved, engineering-based tax strategy that identifies and reclassifies building components from real property (depreciated over 27.5 or 39 years) to personal property or land improvements, which depreciate over 5, 7, or 15 years. This reclassification generates larger deductions in the earlier years of ownership, translating directly into improved cash flow.

Accelerated depreciation front-loads tax benefits, reducing taxable income in the critical early years of ownership. The applicable bonus depreciation percentage for qualified property depends on acquisition date and placed-in-service date.

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Date Range | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | — |

| January 1, 2023 – December 31, 2023 | 80% | — |

| January 1, 2024 – December 31, 2024 | 60% | — |

| January 1, 2025 – January 18, 2025 | 40% | — |

| January 19, 2025 – December 31, 2030 | 100% | Acquisition date on or after January 19, 2025 |

| 2025 (TCJA phase-down applies) | 40% | Acquisition date before January 19, 2025, placed in service in 2025 |

| 2026 (TCJA phase-down applies) | 20% | Acquisition date before January 19, 2025, placed in service in 2026 |

Any taxpayer who owns, constructs, acquires, or renovates commercial real estate or residential rental property may qualify. However, not all property types yield equal benefits. Properties with specialized systems, heavy equipment buildouts, or extensive interior improvements consistently outperform basic structures, which is exactly what the rest of this article covers.

Top Industries That Benefit Most from Cost Segregation Services

These industries consistently generate the highest percentage of reclassifiable assets due to their unique building compositions, specialized systems, and improvement-heavy interiors.

Industry Reclassification Benchmarks at a Glance

| Industry | 5-Year Allocation | 15-Year Allocation | Total Accelerated Allocation |

|---|---|---|---|

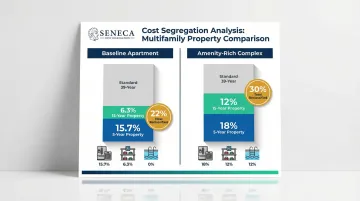

| Multifamily (baseline) | 15.7% | 6.3% | 22% |

| Multifamily (with amenities) | 18% | 12% | ~30% |

| Manufacturing / Industrial | 10.3% | 12.7% | 23% |

| Restaurants | 20–22% | 8% | ~28–30% |

| Retail (standard) | 14% | — | — |

| Hotels / Hospitality | — | — | 25–40% of total basis |

Multifamily and Apartment Buildings

Multifamily properties rank among the most common and high-value candidates for cost segregation. Interior components like appliances, carpet, cabinetry, plumbing fixtures, and parking lots often qualify for 5- or 15-year depreciation rather than the standard 27.5-year residential schedule.

According to engineering benchmarks from over 8,000 studies, multifamily properties average 22% total accelerated allocation at baseline: 15.7% reclassified to 5-year property and 6.3% to 15-year property. Apartment complexes with amenities like clubhouses, pools, and structured parking can reach approximately 30% total reclassification (18% five-year, 12% fifteen-year).

The cash flow freed up from accelerated depreciation is especially valuable for multifamily investors looking to reinvest in their next acquisition or fund property improvements. Even a moderately sized 35-unit complex with a $5.9 million basis can generate over $400,000 in first-year deductions when properly analyzed.

Short-Term Rentals (STRs)

STR owners operating Airbnb, VRBO, or similar properties are uniquely positioned to benefit because the IRS short-term rental exception may allow non-passive losses from cost segregation to offset active income, making the tax benefit even more powerful than for traditional rental owners.

Under IRS regulations, an activity isn't treated as a rental activity if average customer use is 7 days or less, or 30 days or less with significant personal services provided. When combined with material participation (500+ hours annually, or meeting other tests under Reg. §1.469-5T), STR income becomes non-passive, allowing cost segregation deductions to offset W-2 wages or business income.

Common qualifying assets in STRs include:

- Furniture and appliances (5-year property)

- Electronics and specialty décor (5-year property)

- Landscaping and patios (15-year land improvements)

- Pool equipment and hot tubs (5-year property)

- Outdoor kitchens and fire pits (15-year improvements)

Most STR owners never get a cost segregation analysis, meaning the deductions sit unclaimed. A property with a $420,000 basis can generate $119,000+ in first-year deductions when bonus depreciation is applied strategically.

Hospitality (Hotels, Motels, and Resorts)

Hotels and resorts are packed with assets that qualify for accelerated depreciation. Carpeting, decorative lighting, furniture, HVAC for pool areas, laundry equipment, signage, parking lot improvements, and landscaping features like fountains all fall into shorter depreciation classes.

Engineering guidance for hotels shows typical reclassification ranges of 25-40% of total depreciable basis, with first-year benefits often reaching $100,000 to $400,000 per $1 million of cost basis. High-end hotels and resort properties often have a particularly large volume of interior personal property components compared to standard office or industrial buildings.

Hospitality operators deal with thin margins and constant reinvestment pressure. Front-loaded tax savings from cost segregation free up working capital to fund renovations, refresh aging FF&E (furniture, fixtures, and equipment), and cover revenue gaps during off-peak seasons.

Healthcare Facilities (Medical Offices, Dental Practices, Nursing Homes)

Healthcare facilities contain numerous qualifying assets that many accountants miss. The IRS Cost Segregation Audit Techniques Guide explicitly identifies several healthcare-specific components as personal property, including:

- ADA-compliant features and specialized accessibility systems

- Medical-grade ventilation and electrical systems

- Special gas systems (oxygen, nitrogen, nitrous oxide)

- Special waste systems (bio-hazard, medical waste)

- Built-in cabinetry and lab equipment foundations

- Dental chairs and X-ray machine installations

- Process plumbing dedicated to specific medical equipment

Even a relatively small healthcare building, such as a 10,000 square foot dental office, can yield six-figure tax benefits in year one when specialty-use assets are properly reclassified.

Case studies show medical offices with a $3.58 million basis generating over $1 million in additional first-year deductions, while hospital facilities with $21.5 million basis produce over $7 million in accelerated deductions. Most healthcare owners miss these savings because their accountants aren't engineering specialists, which is precisely where an engineering-based study pays for itself.

Manufacturing and Industrial Facilities

Manufacturing plants rank among the highest-value candidates for cost segregation because of the sheer volume of "specialized use" assets built into their structures. Baseline industrial facilities average 23% total accelerated allocation (10.3% five-year, 12.7% fifteen-year).

Process-intensive manufacturing operations routinely exceed these benchmarks, sometimes by a wide margin.

Qualifying components include:

- Equipment foundations and specialized mounting systems (5-year)

- Process piping and compressed air systems (5-year)

- Specialized electrical systems dedicated to machinery (5-year)

- Loading docks and material handling infrastructure (15-year)

- Purpose-built flooring designed for specific production needs (5-year)

- Process-specific HVAC and ventilation (5-year)

The combination of high property values and heavy equipment buildouts means manufacturing clients often see the largest absolute dollar amounts of reclassified assets. Those accelerated deductions convert directly into cash that can fund equipment upgrades or facility expansion without waiting on a depreciation schedule.

Retail Stores and Restaurants

Retail and restaurant properties contain numerous qualifying components, but restaurants in particular outperform standard retail on five-year property allocations. Restaurant studies frequently show 20-22% five-year allocations and 8% fifteen-year allocations at baseline, compared to 14% five-year for standard retail.

Common qualifying assets include:

- Specialized lighting and display fixtures (5-year)

- Refrigeration systems and walk-in coolers (5-year)

- Commercial kitchen equipment foundations (5-year)

- POS and security infrastructure (5-year)

- Outdoor signage and monument signs (15-year)

- Drive-through infrastructure (15-year)

- Parking lot improvements and landscaping (15-year)

Restaurants benefit particularly from frequent renovations and tenant improvements. Each renovation cycle can trigger a new cost segregation opportunity, and older improvements can often be caught up through a look-back study. The IRS even published a specific field directive for restaurants to reduce unnecessary disputes over kitchen equipment and specialty systems.

Franchise owners and multi-location retail operators can compound their savings across multiple properties. Across a portfolio of five or ten locations, the cumulative first-year deductions can reach seven figures, making cost segregation one of the highest-leverage tax strategies available to multi-unit operators.

What Makes a Property an Ideal Candidate for Cost Segregation?

A depreciable cost basis of at least $1 million, or $300,000 for leasehold improvements, characterizes an ideal candidate property. Meaningful tax liability is also a qualifying factor. Without both, the ROI on a study may be limited. Industry guidance consistently cites these thresholds to ensure positive returns.

| Qualifying Criterion | Minimum Threshold |

|---|---|

| Depreciable cost basis | $1,000,000+ |

| Leasehold improvements basis | $300,000+ |

| Tax liability | Meaningful tax liability required |

Ideal timing scenarios:

- New construction - Capture accelerated depreciation from day one

- Recent acquisition - Maximize deductions in early ownership years

- Major renovation - Reclassify improvement costs immediately

- Look-back study - Claim missed depreciation from prior years

Look-back studies are especially valuable for investors who acquired property before learning about cost segregation. Using Form 3115 (Application for Change in Accounting Method), they can claim all unclaimed depreciation in a single year through a Section 481(a) adjustment, with no amended returns required. Under Rev. Proc. 2015-13, negative adjustments that decrease taxable income are taken entirely in the year of change, delivering immediate cash flow benefits.

All of these approaches, whether timed at acquisition or applied retroactively, depend on the quality of the study itself. Studies conducted by licensed engineers who evaluate actual building components, rather than relying on estimates or software-only tools, result in more defensible deductions and stronger audit protection.

The IRS Cost Segregation Audit Techniques Guide emphasizes that quality studies are prepared by individuals with relevant expertise, include detailed methodology descriptions, and contain thorough legal analysis to support property classifications.

How Seneca Cost Segregation Helps Clients Across Industries

With over 10,200 properties assessed nationwide, Seneca Cost Segregation applies a detailed, engineering-driven methodology to every property type, from single-family rentals to large-scale manufacturing facilities. The firm serves clients in all 50 states, completing most studies within 2-4 weeks while maintaining a 95% client referral rate.

Key differentiators across industries:

- CCSP-certified team: Seneca's professionals hold the Certified Cost Segregation Professional (CCSP) designation through the ASCSP, meeting IRS-compliant industry standards.

- In-house proprietary technology: Built by engineers and tested for compliance, the platform identifies components more accurately than off-the-shelf software and adapts quickly to regulatory changes.

- Documented results: The firm averages $171,243 in first-year deductions per study, ranging from $40,000 on smaller properties to over $1 million for large commercial facilities.

- AuditDefense with money-back guarantee: Every study includes AuditDefense protection backed by detailed engineering documentation, designed to hold up under IRS scrutiny.

A complimentary assessment is available through Seneca to determine how much a specific property could generate in first-year deductions.

Frequently Asked Questions

Who benefits from cost segregation?

Any taxpayer who owns, purchases, constructs, or renovates commercial real estate or residential rental property may benefit. The greatest benefits go to owners of capital-intensive properties with specialized assets and a cost basis of $1 million or more, though properties with $300,000+ in leasehold improvements can also generate strong returns.

What are the best properties for cost segregation?

The best property types include multifamily apartments, hotels and resorts, healthcare facilities, manufacturing plants, and retail/restaurant spaces. Properties with a high proportion of personal property assets (equipment, fixtures, specialized systems) yield the highest reclassification rates, typically 20-40% of depreciable basis.

What are the benefits of cost segregation in real estate?

Cost segregation delivers accelerated depreciation deductions, deferred income tax, and increased short-term cash flow, plus potential bonus depreciation eligibility. STR owners who materially participate can also generate non-passive losses that offset active income, turning real estate into an active tax strategy.

How much can I save with a cost segregation study?

Savings vary by property type, cost basis, and tax bracket. Seneca's average first-year deduction is $171,243, though actual results range from $40,000 to over $1 million depending on property characteristics.

When is the best time to do a cost segregation study?

Ideally at acquisition or completion of construction to maximize early-year deductions. That said, look-back studies allow owners to claim prior-year missed depreciation in a single tax year via Form 3115, even for properties placed in service years ago.

Can cost segregation be applied to a property I already own?

Yes. Look-back studies apply to properties already in service, and any unclaimed depreciation can be accelerated into the current tax year through an accounting method change (Form 3115), with a Section 481(a) adjustment capturing all missed deductions at once, no amended returns required.