This guide explains which marina assets qualify for accelerated depreciation, how the real vs. personal property distinction works, how bonus depreciation interacts with marina infrastructure, and what a cost segregation study can do for both current tax liability and long-term property value.

TLDR:

- Marina owners typically reclassify 20-40% of property costs into accelerated depreciation schedules

- 100% bonus depreciation is now permanent for qualifying assets placed in service after January 19, 2025

- A $2.78M marina generated $472,865 in first-year tax savings through cost segregation

- Floating docks, electrical pedestals, and fuel systems often qualify as 5-year personal property

- Look-back studies capture missed deductions from prior years without amending returns

What Is a Depreciation Study and Why Marina Owners Need One

A cost segregation (or depreciation) study is an engineering-based tax analysis that breaks a commercial property into individual components and reclassifies assets from 39-year straight-line depreciation into 5-, 7-, or 15-year accelerated schedules. This produces front-loaded deductions that improve near-term cash flow.

Why Marinas Are Uniquely Positioned to Benefit

Marinas hold a high share of personal property and land improvements that qualify for reclassification — far more than a typical office or retail building:

- Floating dock sections and modular dock systems

- Electrical pedestals and shore power hookups

- Fuel dispensing systems and pump-out stations

- Parking lots and access roads

- Exterior lighting and security systems

- Seawall improvements

A marina acquired for approximately $2.78M generated $472,865 in first-year tax savings through a cost segregation study — illustrating the scale of potential benefit when assets are correctly classified.

Who Qualifies for a Cost Segregation Study

Marina owners qualify if they:

- Hold the property as a business or investment asset (not a primary residence)

- Have a depreciable cost basis typically above $200,000

- Expect to hold the property for at least 3 years

Look-back studies can also be performed retroactively on properties acquired since 1986. Under IRS Revenue Procedure 2015-13, you can capture all previously missed accelerated depreciation in the current tax year via an IRC §481(a) adjustment — without amending prior returns.

Tax Mechanics: A Simple Before/After Comparison

The mechanics are straightforward: larger deductions in early ownership years lower taxable income and reduce federal tax liability directly.

Example:

- Without cost segregation: A marina owner depreciates the entire $2M property over 39 years = ~$51,000/year

- With cost segregation: $800,000 reclassified into 5- and 15-year categories

- Under 100% bonus depreciation: The owner deducts the full $800,000 in year one

- Tax savings (37% bracket): $800,000 × 37% = $296,000 immediate tax savings

Marina Assets That Qualify for Accelerated Depreciation

A marina's asset mix is one of the richest in commercial real estate for depreciation reclassification. While general commercial properties typically see 20-40% of their basis reclassified, marinas often skew higher because so much of the property's value sits in components that are not structural.

5-Year Personal Property (Most Aggressive Depreciation)

Marina-specific assets that typically fall into the 5-year category include:

- Floating dock sections (when classified as personal property due to removability)

- Electrical pedestals and shore power systems

- Specialized slip and walkway lighting

- Pump-out station equipment

- Security systems and cameras

- Boat lift mechanisms

- Point-of-sale and marina management software systems

Assets in this category must be tangible personal property — not permanently affixed to or a structural component of the building. Floating docks are the clearest example: their modular, removable design helps them withstand IRS scrutiny as personal property rather than real estate.

15-Year Land Improvements (Significant Opportunity)

According to IRS Revenue Procedure 87-56, Asset Class 00.3 explicitly includes "wharves and docks" as 15-year land improvements, along with:

- Fixed dock systems attached to permanent pilings (when classified as site improvements)

- Parking lots and access roads

- Seawall improvements

- Landscaping

- Exterior lighting systems

- Fencing and gates

- Boat ramp surfaces

These categories are particularly valuable for marina owners because facilities like parking areas, access lanes, and exterior lighting often represent 20-30% of total site investment — yet are routinely lumped into 39-year real property by owners who never conducted a formal study.

39-Year Real Property (Unavoidable but Minimize Where Possible)

Components that typically remain in the 39-year category are those that form the physical structure of the building itself — items that cannot be removed without compromising the building's integrity:

- Main building shell (harbormaster's office, boathouse, repair shop structure)

- Permanent structural foundations

- Core plumbing systems integrated into the building

In most marina studies, a well-executed cost segregation analysis shifts a meaningful portion of property basis out of this 39-year bucket — often enough to generate six figures in first-year deductions on a mid-size facility.

How Bonus Depreciation Amplifies Marina Tax Savings

The One Big Beautiful Bill Act (OBBBA), enacted July 4, 2025, permanently reinstated 100% bonus depreciation for assets acquired or placed in service after January 19, 2025. This allows marina owners to deduct the full cost of qualifying 5-year and 15-year property in the year placed in service — rather than spreading deductions over the depreciation schedule.

Simplified Illustrative Scenario

If a cost segregation study reclassifies $600,000 of a marina's total cost into 5-year and 15-year categories:

- 100% bonus depreciation means the owner deducts the full $600,000 in year one

- At a 37% effective tax rate, that represents $222,000 in immediate tax savings

This is a hypothetical illustration based on the tax mechanics, not a guaranteed outcome. Results vary by property mix, tax situation, and professional implementation.

Bonus depreciation is powerful on its own — but it's not the only lever available.

Section 179 as an Alternative or Complement

Marina owners can also use Section 179 expensing for specific personal property assets. According to IRS Publication 946, the maximum Section 179 deduction for tax years beginning in 2026 is $2,560,000, with a phase-out threshold beginning at $4,090,000 in qualifying property.

Used strategically, the two approaches complement each other:

- Bonus depreciation applies broadly to qualifying 5-year and 15-year property placed in service

- Section 179 offers flexibility for specific personal property assets, particularly when phase-out limits are not a concern

The right sequencing depends on the owner's overall tax picture. A qualified cost segregation professional works alongside the owner's CPA to determine the optimal approach.

Real Property vs. Personal Property: The Marina Classification Challenge

The most consequential decision in any marina depreciation study is how the docks are classified.

Floating Docks vs. Fixed Docks

Floating docks that are modular and removable (not permanently embedded in the seabed) are generally treated as personal property eligible for 5-year depreciation or immediate expensing under bonus depreciation.

Fixed docks with pilings permanently embedded in the seabed are more likely to be treated as real property (39-year) or at best land improvements (15-year).

This is a fact-specific determination that varies by structure type. The Tax Court case Estate of Shirley Morgan v. Commissioner (1969) ruled that floating docks attached to guide pilings were "tangible personal property" because they were not inherently permanent, while the pilings driven into the harbor bottom were inherently permanent.

Utility Infrastructure Classification

Electrical pedestals, shore power hookups, and pump-out stations are typically personal property because they serve a specific equipment function rather than being structural components of a building.

This is where many marina owners miss significant deductions — these systems appear "built in" but are actually reclassifiable under IRS Cost Segregation Audit Techniques Guide standards.

The Importance of Engineering-Based Documentation

Getting these classifications right — and defending them — depends entirely on the quality of your documentation.

IRS guidance (including Revenue Procedure 87-56 and relevant court cases) supports engineering-based documentation as the gold standard for defending asset classifications. Studies lacking engineering methodology rarely survive an audit challenge; properly documented ones do.

This is why the methodology behind a cost segregation study matters as much as the study itself. Seneca Cost Segregation's CCSP-certified engineers apply IRS-compliant engineering analysis to each property, with AuditDefense coverage included if the IRS ever questions the classifications.

Look-Back Opportunity: Capturing Missed Deductions

Marina owners who purchased or improved their property years ago and never conducted a study can still capture the missed accelerated depreciation in the current tax year via a catch-up deduction.

How it works:

- A marina acquired five years ago can have a study done today

- All previously unclaimed accelerated depreciation is claimed in the current filing year

- This uses an IRC §481(a) adjustment filed on Form 3115

- No need to amend prior returns

How a Depreciation Study Affects Marina Valuation and Sale Price

The Connection Between Depreciation and Valuation

Buyers and lenders use Net Operating Income (NOI) and cap rates to determine what a marina is worth. Depreciation itself is added back in EBITDA calculations, but a strategic depreciation study that has improved the owner's cash flow creates real financial statements that show a stronger, more liquid operation — which translates to better sale positioning.

According to Marina Dock Age, sellers who prepare financials carefully — including documented non-recurring expenses and accurate P&L statements — achieve higher sale prices.

A marina with well-organized depreciation schedules, documented asset classifications, and clean financial records gives buyers fewer questions to ask and fewer reasons to negotiate the price down. That means faster due diligence and a cleaner path to closing.

Depreciation Recapture: What to Know Before You Sell

When a marina is sold, accumulated depreciation has tax consequences:

- Section 1245 recapture: Depreciation on personal property is recaptured at ordinary income rates

- Section 1250 unrecaptured gains: Real property depreciation is subject to 25% unrecaptured gains tax

Discuss exit strategy with your CPA before conducting a study. Depreciation recapture does not eliminate the benefit; it affects timing and structuring decisions.

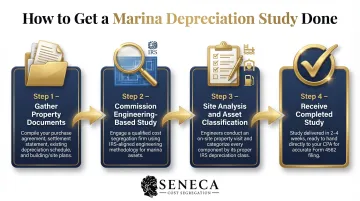

Steps to Get a Depreciation Study Done for Your Marina

1. Gather property documents

- Purchase agreement

- Settlement statement

- Existing depreciation schedule

- Building plans or as-built drawings

2. Commission an engineering-based study

- Choose a qualified firm with marina or waterfront property experience

- Ensure the firm uses IRS-aligned engineering methodology

3. Site analysis and asset classification

- The engineering team visits the property

- Reviews purchase documents and construction records

- Categorizes every component by depreciation class

4. Receive completed study

- Typically delivered within 2-4 weeks

- Provided to your CPA to apply on the tax return via Form 4562

What to Look for in a Qualified Provider

- IRS-aligned engineering methodology — ensures your study holds up under IRS scrutiny

- CCSP certification (Certified Cost Segregation Professional)

- Audit defense protection — ideally with a money-back guarantee

- Experience with marina or waterfront property specifically

Seneca Cost Segregation has completed over 10,200 studies across all 50 states, with an average first-year deduction of $171,243 for clients. Marina owners can request a complimentary tax assessment to see what their property qualifies for before committing to a full study.

Frequently Asked Questions

How profitable is owning a marina?

Marina profitability hinges on slip occupancy, ancillary revenue (fuel, retail, dry storage), and infrastructure costs. According to Marina Dock Age's 2025 survey, median occupancy hit 92%, yet 78% of operators expect rising expenses. Cost segregation studies directly improve net cash flow by accelerating depreciation and cutting federal tax liability.

What marina assets qualify for accelerated depreciation?

Common qualifying categories include:

- Floating dock sections and modular dock systems (5-year)

- Electrical pedestals and shore power systems (5-year)

- Parking lots and fixed site improvements (15-year)

- Seawall and access road improvements (15-year)

The main building shell typically remains at 39-year depreciation.

Are floating docks considered personal property or real property for tax purposes?

Floating docks are generally classified as personal property because they are modular and removable — not permanently embedded in the land. This means they may qualify for 5-year depreciation or immediate expensing under bonus depreciation rules, confirmed through an engineering analysis.

Can marina owners claim bonus depreciation on dock infrastructure?

Yes. Qualifying personal property and 15-year land improvements identified in a cost segregation study may be eligible for 100% bonus depreciation, reinstated under the OBBBA for assets placed in service after January 19, 2025. This allows the full deduction in the year the asset is placed in service.

How much can a marina owner save with a cost segregation study?

Savings vary by property value, asset mix, and tax rate. Published case study data shows a marina purchased for approximately $2.78M generated $472,865 in first-year tax savings, with a general industry benchmark of up to $100,000 in tax savings per $1M in depreciable building costs.

Can I do a depreciation study on a marina I purchased several years ago?

Yes. A look-back study can be performed on properties acquired since 1986, allowing owners to claim all previously uncaptured accelerated depreciation as a catch-up deduction in the current tax year under IRS rules, without amending prior returns.