Introduction

Laboratory buildings—whether biotech facilities, pharmaceutical research centers, or R&D campuses—rank among the most cost-segregation-friendly commercial properties available, yet most owners still depreciate them on a standard 39-year schedule. Lab owners underestimate how much of their building's total cost qualifies for accelerated depreciation, given the extraordinary density of specialized systems embedded in these facilities.

Research shows that R&D facilities commonly reallocate 30–55% of basis to 5-, 7-, and 15-year property, compared to just 10–40% for standard office buildings. That gap translates to hundreds of thousands of dollars in accelerated first-year deductions that most lab owners are simply leaving on the table.

What follows breaks down exactly why lab buildings outperform standard commercial real estate in cost segregation studies—and what that means for your tax position.

TLDR

- Cost segregation reclassifies lab building components from 39-year real property into 5-, 7-, or 15-year classes, front-loading tax deductions

- Lab facilities qualify for high reclassification percentages reclassification percentages of 30–55%, driven by process gas systems, dedicated HVAC, purified water infrastructure, and cleanroom equipment

- 100% bonus depreciation (restored for property placed in service after January 19, 2025) lets lab owners deduct reclassified assets entirely in Year 1

- Retroactive studies via Form 3115 recover missed depreciation from prior years without amending returns

- IRS guidance explicitly classifies lab-specific systems as §1245 personal property, creating a defensible legal foundation

What Is Cost Segregation for Laboratory Buildings

Cost segregation is an engineering-based tax analysis that breaks a building's total cost into component asset classes with different IRS-assigned recovery periods, rather than depreciating the entire structure over 39 years as nonresidential real property.

For laboratory buildings specifically, this means identifying which systems serve the building's general operation (§1250 structural components) versus which systems serve the laboratory processes themselves (§1245 personal property with shorter lives). The IRS Cost Segregation Audit Techniques Guide contains a dedicated section and matrix for the Pharmaceutical and Biotechnology industry, making this distinction part of official IRS guidance.

Cost segregation is a cash flow acceleration tool. It does not reduce the total depreciation a lab owner claims over time — it front-loads those deductions, freeing capital for reinvestment immediately.

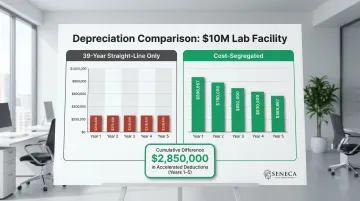

Consider a $10 million lab facility where 35% of costs are reclassified to 5-year property. Cumulative depreciation in Years 1–5 jumps from $1.28 million (39-year straight-line) to $4.13 million (cost-segregated treatment): a $2.85 million difference that stays in the owner's hands, not the IRS's.

Key Advantages of Cost Segregation for Laboratory Buildings

Laboratory buildings consistently generate higher reclassification percentages than standard offices or retail spaces because their infrastructure is purpose-built around scientific processes, not general occupancy. The advantages below are directly tied to the physical and operational characteristics of lab buildings, not generic real estate tax theory.

Advantage 1: Laboratory Buildings Contain an Unusually High Density of Short-Life Personal Property

Standard commercial buildings typically see 20–30% of total cost reclassified through cost segregation, while laboratory facilities routinely exceed this range, with R&D facilities commonly reallocating 30–55% of basis to shorter-lived assets. This advantage is created by the sheer volume of specialized systems embedded within the structure:

Systems that qualify as §1245 personal property in lab buildings:

- Process gas delivery systems – Nitrogen, argon, CO₂, and oxygen distribution networks separate from building natural gas

- Purified water infrastructure – Deionized and water-for-injection systems distinct from building plumbing

- Special waste collection – Toxic, biohazardous, and nuclear waste systems separate from building sewer

- Equipment-specific electrical – Dedicated branch circuits tied to specific machinery, not building operation

- Specialty HVAC units – Systems meeting the IRS sole-justification test for equipment operation (not occupant comfort)

- Cleanroom air handling – Special air filtration and climate control equipment

Why this is an advantage:

Each of these systems, when properly classified, converts from a 39-year straight-line deduction into a 5- or 7-year accelerated deduction. Lab owners recover their capital cost roughly 5–8 times faster on those components and can deploy that tax savings into operations, new equipment, or additional real estate.

Hypothetical example: For a $10M laboratory building where 35% of costs are reclassifiable:

| Year | 39-Year SL Only | Cost-Segregated | Difference | Cumulative Difference |

|---|---|---|---|---|

| 1 | $256,410 | $866,667 | $610,257 | $610,257 |

| 2 | $256,410 | $1,286,667 | $1,030,257 | $1,640,513 |

| 3 | $256,410 | $838,667 | $582,257 | $2,222,769 |

| 4 | $256,410 | $569,867 | $313,457 | $2,536,226 |

| 5 | $256,410 | $569,867 | $313,457 | $2,849,682 |

Front-loaded deductions in Years 1–5 reduce federal tax liability in the same years that lab owners face the heaviest capital expenditures, creating a natural offset.

KPIs impacted:

- Annual federal tax liability

- Cumulative depreciation deductions in first 5 years of ownership

- Effective tax rate

- After-tax return on investment for the property

When this advantage matters most:

This advantage is strongest in new construction (where full cost records enable the most accurate engineering analysis) and upon acquisition of an existing lab building (where purchase price can be allocated across asset classes using a detailed engineering estimate approach).

Advantage 2: Process-Specific Lab Systems Qualify as Tangible Personal Property Under IRS Guidance

The IRS Cost Segregation Audit Techniques Guide contains specific guidance for the Biotech/Pharmaceutical industry that formally recognizes lab-specific systems as §1245 property, giving lab building owners a well-documented legal basis for reclassification that holds up better under scrutiny than in mixed-use commercial properties, where the distinction between process-serving and building-serving infrastructure is far less clearly defined in IRS guidance.

Specific categories covered:

- IRS ATG explicit recognition – The Biotech/Pharmaceutical ATG names special gas, water, and waste systems as §1245 property by category, not analogy

- Sole-justification test codified – HVAC units serving equipment (not occupant comfort) are addressed directly, removing interpretive ambiguity

- Structural components addressed – Interstitial areas, catwalks, and equipment foundations qualify when built to serve specific process machinery, per the ATG's functional allocation framework

- Case law backing – Classifications are supported by Hospital Corporation of America and the functional allocation principles from Scott Paper, providing judicial precedent alongside administrative guidance

Why this matters for audit risk:

Because these classifications are supported by IRS field directives and case law, an engineering-based cost segregation study for a lab building is highly defensible if conducted properly. Unlike some accelerated depreciation strategies that rely on interpretive gray areas, lab building cost segregation is explicitly addressed in IRS guidance — the legal foundation is built in.

KPIs impacted:

- Audit risk exposure

- Compliance confidence

- Asset-level depreciation accuracy

- Long-term depreciation schedule reliability

When this advantage matters most:

This is especially valuable for lab owners with complex builds—GMP pharmaceutical facilities, BSL-2/3 research labs, semiconductor fabs—where the density and cost of process systems is highest, and the distinction between building-serving vs. process-serving infrastructure is most critical to document.

Advantage 3: Bonus Depreciation Amplifies First-Year Deductions on Reclassified Lab Assets

Cost segregation reclassifies lab building components into MACRS property with recovery periods of 20 years or less — typically 5, 7, or 15 years. Those reclassified assets are automatically eligible for bonus depreciation in the year placed in service, provided they meet applicable requirements.

Public Law 119-21, the "One Big Beautiful Bill Act," signed July 4, 2025, permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. When 100% bonus applies, a lab owner deducts the entire reclassified amount in a single tax year — potentially millions of dollars — rather than spreading it across 5–7 years.

Why timing amplifies this benefit:

A dollar recovered in Year 1 compounds differently than one recovered in Year 5. For lab owners carrying heavy upfront capital costs from construction or acquisition, the combined effect of cost segregation plus 100% bonus depreciation can reduce or eliminate federal taxable income in the same year those costs hit the books.

A practical illustration: A lab owner who places a $12M facility in service in 2025 and reclassifies 40% of costs ($4.8M) to 5- and 7-year property could potentially claim that entire $4.8M as a Year-1 deduction under current bonus depreciation rules — rather than deducting roughly $308K per year over 39 years under standard straight-line depreciation.

KPIs impacted:

- Year-1 federal tax liability

- Net operating loss carryforward potential

- Cash-on-cash return for the first year of lab ownership

- Investment payback period

When this advantage matters most:

This advantage is strongest when a lab owner is in a high-income tax year (such as the year a facility opens and begins generating revenue), or when the owner has passive income from other real estate that accelerated losses can offset.

What Happens When Lab Building Owners Skip Cost Segregation

Without a cost segregation study, every specialized system in the laboratory—process gas delivery infrastructure, deionized water systems, dedicated HVAC built solely to support lab operations, dedicated electrical runs—defaults to the 39-year straight-line depreciation schedule. That means waiting nearly four decades to recover costs that could have been deducted in years 1–7.

National average fit-out costs for life sciences facilities range from $660/rsf for Bio/Chem Labs to $1,729/rsf for Gene/Cell Therapy spaces. At those costs, skipping cost segregation means forfeiting hundreds of thousands of dollars in annual deductions—capital that could be reinvested into operations, equipment, or the next facility instead of sitting in deferred tax limbo.

The retroactive option exists, but delays compound the problem. The IRS does allow a catch-up depreciation deduction through Form 3115 for owners who skipped a study at acquisition or construction. However, the longer you wait, the harder it becomes to reconstruct and verify historical depreciation data—which reduces both the study's accuracy and its defensibility in an audit.

How to Maximize Cost Segregation Benefits for Laboratory Buildings

Lab building cost segregation demands an engineering-based methodology—not a "rule of thumb" or residual estimation approach. Distinguishing building-serving infrastructure from process-serving infrastructure requires construction expertise, lab-specific system knowledge, and familiarity with IRS guidance for the pharmaceutical and biotech sectors.

Seneca Cost Segregation's licensed professional engineers bring that expertise directly to each study. With over 10,200 studies completed nationwide and a 95% client referral rate, the firm follows the IRS Cost Segregation Audit Techniques Guide to ensure reclassification accuracy and audit defensibility.

Start at the Right Time

The ideal moment for a lab building cost segregation study is at construction completion or acquisition—before the first tax return is filed. Two common scenarios:

- New construction: Cost records, blueprints, and contractor pay applications are available, enabling precise asset-by-asset cost allocation.

- Acquisitions: Even for older lab buildings, a detailed engineering cost estimate can reconstruct values and unlock accelerated depreciation retroactively.

Revisit After Every Major Change

Cost segregation isn't a one-time event. Each major renovation, tenant improvement, or equipment installation in a lab building can create new opportunities to accelerate depreciation on added systems. Updating the asset schedule to reflect disposals and replacements ensures you capture every available tax benefit over the building's life.

Conclusion

Laboratory buildings are uniquely well-positioned for cost segregation. Their specialized infrastructure—process gas systems, dedicated HVAC, purified water systems, and equipment-specific electrical—qualifies for significantly shorter depreciation lives under IRS guidance. Those accelerated timelines produce first-year tax savings that compound further when paired with bonus depreciation.

The strongest results share three common factors:

- Engineering-based methodology that accurately classifies lab-specific components

- Studies conducted at acquisition, construction completion, or after major renovations

- Consistent updates as the facility expands or equipment changes

The study cost itself is typically a fraction of the deductions it generates. Lab owners who haven't yet done a study—even on properties placed in service years ago—can still recover missed deductions through a retroactive analysis. Seneca Cost Segregation has completed this process across more than 10,200 properties nationwide, including complex commercial facilities.

Frequently Asked Questions

What is the $2,500 expense rule for cost segregation?

The $2,500 de minimis safe harbor under IRS tangible property regulations allows businesses to immediately expense individual items costing $2,500 or less per invoice ($5,000 with audited financial statements). This is distinct from cost segregation, which identifies and reclassifies personal property and land improvements into shorter depreciation classes, regardless of individual item cost.

How does a cost segregation study work?

A qualified engineer reviews construction documents, blueprints, and contractor invoices, then conducts a site inspection. The engineer identifies and assigns each component to its correct IRS asset class and recovery period, producing a report the property owner uses to file or amend depreciation schedules.

What makes laboratory buildings especially good candidates for cost segregation?

Labs are filled with process-serving infrastructure—dedicated gas lines, purified water systems, specialized HVAC, equipment-specific electrical—that the IRS explicitly classifies as §1245 personal property rather than building structural components. This results in a higher-than-average percentage of total cost being eligible for accelerated depreciation.

What percentage of a laboratory building's total cost can typically be reclassified through cost segregation?

Reclassification percentages vary depending on lab type, construction methods, and equipment density. Research shows that R&D facilities commonly reallocate 30–55% of basis to shorter-lived assets, compared to 10–40% for standard office buildings. A property-specific benefit estimate will give you the most accurate projection for your lab.

Can I conduct a cost segregation study on a laboratory building I purchased or built several years ago?

Yes. The IRS allows retroactive cost segregation through a Form 3115 accounting method change, enabling lab owners to claim all missed depreciation from prior years as a catch-up deduction in the current tax year without amending prior returns—taken in full in the year the method change is filed.

Do laboratory buildings qualify for bonus depreciation on reclassified assets?

Yes. Reclassified assets with recovery periods of 20 years or less (the 5, 7, and 15-year categories produced by cost segregation) are eligible for bonus depreciation. The current rate is 40% for property placed in service in 2025 under existing law, though proposed legislation may restore higher rates. Confirm the applicable percentage with your tax advisor before filing.