Introduction

According to 2019 RSMeans national construction data, building a standard 20,000-square-foot gymnasium costs approximately $189.23 per square foot when including contractor and architectural fees—totaling roughly $3.78 million in total capital investment. Yet most gym owners default to depreciating this entire investment over 39 years as a single commercial building, effectively giving the IRS an interest-free loan on tax savings that could be accessed immediately.

Treating a $1M+ facility as a single 39-year asset means accepting a 2.56% annual write-off on flooring, equipment, and site improvements that wear out in 5–15 years. That gap between IRS default treatment and economic reality is exactly where cost segregation recovers value.

This article breaks down how cost segregation applies specifically to gyms and fitness centers—which assets qualify for accelerated depreciation, how the numbers work, and which strategies deliver the most advantage depending on where you are in ownership.

TL;DR

- Standard 39-year depreciation leaves tax value on the table—cost segregation reclassifies 20%–40%+ of gym property costs into 5-, 7-, or 15-year categories

- Gyms are especially well-suited to cost segregation due to high concentrations of personal property and short-lived assets like equipment, specialty flooring, AV systems, and locker room buildouts

- Strategic timing matters: apply cost segregation at acquisition, post-renovation, or retroactively via Form 3115 on properties already in service

- Bonus depreciation (100% for qualifying assets placed in service after January 19, 2025) can push first-year deductions far higher when layered with a cost segregation study

How the Tax Burden Builds Up for Gym and Fitness Center Owners

When a gym is purchased or built, the IRS default is to depreciate the entire property over 39 years as a commercial building—meaning every dollar invested in equipment bays, locker rooms, rubber flooring, and specialty lighting is written off at the same slow rate as the structural walls and foundation.

That slow schedule is the problem. Each year a gym owner skips accelerated deductions, they're overpaying federal taxes on income that qualified for faster write-offs. The gap widens with every renovation, equipment upgrade, or expansion.

Cost build-up is triggered or worsened by specific events:

- Opening a new facility

- Completing a renovation or expansion

- Acquiring an existing gym

- Adding amenities like pools, saunas, or studio spaces

Each event creates new depreciable investment that defaults to 39-year depreciation — unless a cost segregation study reclassifies those assets into 5- or 15-year schedules first.

Key Cost Drivers for Gym Cost Segregation Savings

Three variables determine how much a gym owner actually saves through cost segregation. Understanding each one helps set realistic expectations before a study begins.

Depreciable Asset Base

The size and composition of the gym's depreciable asset base is the primary driver. Facilities with significant personal property (equipment, specialty flooring, lighting systems, AV, lockers) and land improvements (parking lots, landscaping, outdoor signage) typically unlock 20–40% reclassification rates — the highest of any commercial property type.

reclassification rates](https://file-host.link/website/senecacostseg-88wktt/assets/blog-images/5776261c-127e-4d00-a3b2-1743ce876726/1776373032857796_37533adf74f44c378e0aaf990173157a/360.webp)

Study Timing

Study timing relative to when the property was placed in service shapes which approach makes sense:

- Newly acquired or recently renovated gyms can take advantage of current-year bonus depreciation

- Older properties require a catch-up approach (lookback study via Form 3115) that delivers deductions retroactively in the current year

Owned vs. Leased Space

- Full building ownership unlocks the broadest reclassification — every structural component is in play

- Leasehold tenants with substantial improvements can still apply cost segregation to Qualified Improvement Property (QIP) under a 15-year depreciation schedule

Cost Segregation Strategies for Gyms and Fitness Centers

Gym owners can apply cost segregation at several distinct decision points. The right approach depends on whether you're planning a new project, managing an existing facility, or recovering deductions missed in prior years.

Strategies That Reduce Tax Burden by Changing Decisions Upfront

These choices are made before or during a gym buildout, acquisition, or renovation, and they directly determine how much of the investment can be reclassified.

Segregate costs during construction:

Ensure contractors provide line-item invoices that distinguish personal property (equipment mounts, specialty lighting, rubber flooring) from structural work. This documentation is the foundation of a defensible study. Construction records get lost, contractors move on, and building modifications complicate analysis. Fresh documentation from recent construction produces the most accurate and audit-defensible results.

Make the cost segregation decision before or during closing:

Early engagement allows the study to be completed before the first tax return is filed, capturing maximum first-year deductions without needing an amended return.

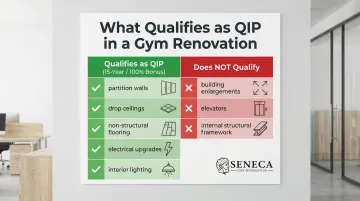

Identify Qualified Improvement Property (QIP) during renovations:

Interior improvements to nonresidential space—including partition walls, ceilings, non-structural flooring, and electrical upgrades—are classified as 15-year property and eligible for 100% bonus depreciation under current law. Note that building enlargements, elevators, and internal structural framework do not qualify as QIP.

Confirm the investment threshold:

Study fees are typically a fraction of the first-year tax benefit — but not every property clears the bar. Commonly cited minimums for gym properties are in the $500K+ range for newly built or acquired facilities, though some firms recommend a $300,000 minimum depreciable basis (excluding land).

Strategies That Reduce Tax Burden by Changing How the Property Is Managed

These ongoing practices preserve and extend the value of a cost segregation study over the life of the gym.

Track asset costs at the component level:

When individual asset costs are documented separately (e.g., sauna heaters, cardio machines, studio mirrors), they can be depreciated at their correct individual lives rather than bundled into the building's 39-year schedule.

Use partial disposition elections:

When gym components are replaced or removed (e.g., replacing rubber flooring, removing locker room fixtures, upgrading HVAC), this allows the owner to deduct the remaining undepreciated basis of the retired component in the year of removal instead of continuing to depreciate a no-longer-existing asset.

Revisit the cost segregation study after major renovations:

A gym that adds a pool, converts studio space, or builds out a new wing has created additional depreciable assets that may warrant a supplemental study or updated asset classification.

Maintain IRS-defensible records:

- Site inspection documentation

- Photographs of building components

- Construction invoices

- Asset-level depreciation schedules

Gym-specific assets like specialty flooring and built-in equipment attract IRS scrutiny without solid classification support — thorough records are what keep a study defensible.

Strategies That Reduce Tax Burden by Changing the Context Around the Investment

These broader approaches enhance or extend what cost segregation can deliver, particularly when combined with other tax provisions or applied to properties already in service.

Layer bonus depreciation on qualifying reclassified assets:

When a cost segregation study identifies 5-year and 15-year property in a gym (equipment systems, specialty lighting, QIP), those assets can be fully deducted in the first year under the reinstated 100% bonus depreciation rules for property placed in service after January 19, 2025. The full tax benefit lands in year one rather than spread across decades.

Conduct a retroactive (lookback) cost segregation study:

For gyms that have been in service for several years without a study, owners can use Form 3115 to claim catch-up depreciation on missed deductions in a single tax year without amending prior returns. This generates a cumulative Section 481(a) adjustment that captures all the depreciation that could have been claimed from day one.

Engage an engineering-based cost segregation firm:

Engineering-led studies, like those provided by firms with certified CCSP professionals and licensed engineers on staff, apply physical inspection and cost allocation methodology that holds up under IRS audit and typically identifies more qualifying assets than generalist CPA estimates. The IRS Cost Segregation Audit Techniques Guide explicitly warns examiners to view "rule of thumb" approaches with caution, noting that estimating personal property as a fixed percentage of project costs lacks sufficient documentation.

Seneca Cost Segregation offers engineering-backed studies with AuditDefense and typical turnaround of 2–4 weeks, combining technical accuracy with quick implementation timelines.

Conclusion

Cost segregation for gyms and fitness centers is about accurately representing how different parts of the facility depreciate — and the IRS framework explicitly accounts for that. Accelerating deductions on flooring, HVAC systems, and specialized equipment isn't a workaround; it's the methodology working as intended.

The most effective strategies start with an honest assessment of where you are in the ownership lifecycle, which assets you hold, and whether you've already left years of deductions on the table. Gym owners who move at the right moment free up capital that can go back into equipment, facility upgrades, or the next acquisition. The three windows where action pays off most:

- At acquisition — capture maximum first-year deductions before depreciation schedules lock in

- Post-renovation — reclassify newly installed components before filing the next return

- Retroactively — file a catch-up study to recover deductions missed in prior years

Frequently Asked Questions

Who qualifies for cost segregation for gyms?

Any gym or fitness center owner who owns the commercial property (or has made significant leasehold improvements as a tenant) and has a depreciable basis above $500K is a strong candidate. Both newly acquired properties and existing facilities qualify, and studies can be applied retroactively using Form 3115.

What is the typical cost of a cost segregation study for a gym?

Study fees typically range from $5,000–$15,000 depending on property size and complexity. For most eligible gym properties, that cost represents a small fraction of the first-year tax benefit — properties with a depreciable basis of $300K–$500K or more (excluding land) generally justify the investment.

What type of asset is gym equipment and how is it depreciated?

Most gym equipment (cardio machines, free weights, strength training stations) is classified as 5-year personal property under MACRS Asset Class 57.0, making it eligible for accelerated depreciation and potentially 100% bonus depreciation in the year of purchase.

What is the depreciation rate for a commercial building?

The IRS default for commercial (nonresidential) real property is straight-line depreciation over 39 years, which is why cost segregation is valuable—it reclassifies portions of the building into shorter lives (5-, 7-, or 15-year) rather than accepting the full 39-year schedule.

Can I deduct gym equipment purchases on my taxes?

Yes, gym equipment purchases are deductible through depreciation. Under current bonus depreciation rules, qualifying equipment placed in service after January 19, 2025, may be fully deductible in the year of purchase—a cost segregation study ensures all eligible items are properly identified and classified.

What is a depreciation study?

A depreciation study (also called a cost segregation study) is an engineering and tax analysis that breaks down a property's total cost into individual asset components and assigns each the correct IRS depreciation life. The resulting report is used by your CPA to front-load deductions — and because it's engineering-based, it holds up to IRS scrutiny.