Introduction

Dental offices represent one of the most capital-intensive commercial buildouts in healthcare. According to industry data, dental office construction costs typically range from $300 to $430 per square foot when including both construction and equipment—meaning a 2,500-square-foot office can easily require an investment of $750,000 to over $1 million.

Despite this substantial capital outlay, most dental practice owners default to a 39-year straight-line depreciation schedule. This standard approach means the IRS-approved opportunity to accelerate tens or hundreds of thousands of dollars in deductions goes unclaimed every year, leaving taxable income artificially high and cash flow tighter than it needs to be.

This article walks through specific cost segregation strategies dental office owners can use—from decision-making before construction to structural approaches after purchase—to legally reduce their tax burden and free up cash flow.

TL;DR

- Dental offices contain unusually high densities of short-lived assets—specialty plumbing, electrical circuits, cabinetry, imaging rooms, and equipment—making them strong cost segregation candidates

- Engineering-based studies typically reclassify 20% to 40% of dental buildout costs into 5-, 7-, or 15-year property, accelerating deductions to year one

- Bonus depreciation was permanently restored to 100% for property acquired after January 19, 2025, maximizing first-year savings

- Catch-up studies, grouping elections, and entity structuring unlock savings for offices that haven't done a study yet

- First-year savings reinvested into the practice can fund equipment upgrades, additional operatories, or a second location

How the Tax Burden Quietly Compounds for Dental Office Owners

How the Tax Burden Quietly Builds for Dental Office Owners

Without cost segregation, the tax cost of owning a dental office builds gradually across years of missed accelerated depreciation. Every year without reclassification keeps taxable income artificially high, forcing practice owners to pay taxes on income they could have legally shielded.

This build-up is triggered by specific events:

- Purchasing a building

- Completing a major buildout

- Renovating operatories

- Acquiring new imaging or sterilization equipment

Each event creates a depreciation opportunity — one that the standard 39-year straight-line schedule largely wastes. That schedule spreads deductions so thinly that practice owners see minimal cash flow benefit in the years they need it most.

The financial gap stays hidden because 39-year straight-line depreciation is the default CPA approach — no one flags what isn't being claimed. A cost segregation analysis draws the "before vs. after" comparison directly, and the results are concrete: dental offices routinely uncover $50,000 to $200,000+ in first-year deductions that were left on the table.

What Makes Dental Offices Uniquely Suited for Cost Segregation

Unlike generic commercial office space, dental offices require extensive specialty infrastructure embedded in the structure itself. These components qualify for accelerated depreciation under MACRS but are frequently overlooked without engineering-based analysis.

High-Value Specialty Systems

Dental facilities contain:

- Dedicated electrical circuits for imaging systems, X-ray machines, and sterilization equipment

- Medical-grade plumbing for operatories, sterilization centers, and suction systems

- Lead-lined walls for X-ray compliance and radiation safety

- Soundproofing to isolate operatory noise

- Custom cabinetry with integrated sterilization units and storage

- Specialty flooring and lighting designed for clinical environments

Three Primary Asset Categories

Personal Property — 5 to 7-Year Depreciation

- Dental chairs and delivery units

- Imaging systems and X-ray machines

- Vacuum pumps and compressors

- Computers and digital scanners

- Sterilization equipment

Land Improvements — 15-Year Depreciation

- Exterior paving and parking lots

- Landscaping and irrigation systems

- Signage and exterior lighting

- Sidewalks and fencing

Specialty Interior Improvements — 5 to 15-Year Depreciation

- Custom cabinetry and millwork

- Specialty lighting and electrical

- Plumbing configurations for operatories

- Flooring and wall finishes in clinical areas

Leasehold Improvements Are Eligible

Owning the building isn't a requirement. Dental practices that lease their space and have invested in tenant-specific buildouts can still conduct a cost segregation study. Qualified leasehold improvement property is reclassified under the same accelerated depreciation rules as owned buildings.

Real-World Impact

A CSSI case study documented a dental office acquired for $1,506,900. The cost segregation study identified:

- $411,381 reclassified to 5-year property

- $235,075 reclassified to 15-year property

- $236,373 in first-year tax savings with 100% bonus depreciation

Engineering-based studies typically identify 20% to 35% of a dental clinic's total project cost as eligible for reclassification, which runs higher than most standard commercial properties. On facilities with extensive technical infrastructure, that figure can climb to 30% to 50%.

Cost Segregation Strategies That Cut Tax Costs for Dental Offices

The strategies dental practice owners use to maximize cost segregation savings vary depending on whether the office has been recently built or purchased, is currently owned and unstudied, or involves a self-rental arrangement. Each scenario calls for a different approach.

Strategies That Reduce Tax Costs by Changing Decisions Around Your Dental Office

Make these decisions before or during property acquisition, construction, or renovation. They directly influence how much of the investment can be accelerated—and delay increases the carrying cost of over-taxed income.

Strategy 1 — Time the Study to the Year of Acquisition or Buildout Completion

Conducting a cost segregation study in the same tax year the property is placed in service unlocks maximum first-year benefit. The One Big Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025.

Timing Impact:

| Acquisition Date | Placed in Service | Bonus Depreciation |

|---|---|---|

| Before Jan 20, 2025 | 2025 | 40% (TCJA phase-down) |

| After Jan 19, 2025 | 2025 or later | 100% (permanent) |

For property acquired before January 20, 2025, the TCJA phase-down still applies. Property acquired after that date qualifies for full expensing of reclassified assets in year one—turning hundreds of thousands in depreciation into immediate deductions.

Strategy 2 — Choose an Engineering-Based Study Over Rule-of-Thumb Estimates

Not all cost segregation studies carry equal weight with the IRS. Generic percentage-allocation or "desktop" studies without site-level documentation can be challenged on audit. Engineering-based studies maximize reclassification accuracy and IRS defensibility.

Engineering-based studies include:

- Licensed engineers reviewing blueprints and contractor invoices

- On-site property inspections

- Component-by-component asset classification

- Documentation aligned with IRS Cost Segregation Audit Techniques Guide

Seneca Cost Segregation's engineering-based methodology follows IRS guidelines precisely and includes an AuditDefense guarantee—so the study holds up if the IRS asks questions.

Strategy 3 — Document All Construction and Improvement Costs at the Time of Buildout

Retaining detailed documentation prevents costly reconstruction later:

- Contractor invoices (itemized)

- Architect drawings and blueprints

- Equipment purchase receipts

- Renovation plans and change orders

- Build-out specifications

The more granular the documentation, the more precisely assets can be classified—especially for specialty installations like lead-lined imaging rooms, custom plumbing configurations, and integrated cabinetry systems.

Strategy 4 — Evaluate Section 179 Expensing Alongside Bonus Depreciation for Equipment

For 2025, the Section 179 deduction limit is $2,500,000, with a phase-out beginning at $4,000,000 in total equipment purchases.

Dental equipment like chairs, imaging units, delivery systems, and digital scanners qualify as personal property regardless of cost segregation. Section 179 expensing can complement or replace bonus depreciation, depending on your tax situation.

Ordering rules matter: Section 179 must be computed first, then bonus depreciation, then regular MACRS depreciation. Strategically applying each tool to the right asset class optimizes the deduction stack.

Strategies That Reduce Tax Costs by Changing How Cost Segregation Is Managed Over Time

Ongoing visibility, timing, and consistency matter just as much as the initial study. These approaches reduce tax costs across the full life of the property.

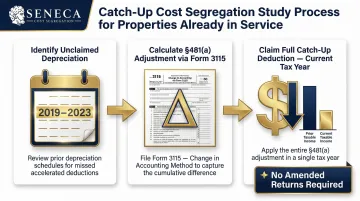

Strategy 1 — Conduct a Catch-Up Study on Properties Already in Service

Dental offices placed in service in prior years without a cost segregation study are not excluded. A "lookback" study allows the owner to claim all previously unclaimed accelerated depreciation in a single year via IRS Form 3115 (change of accounting method)—without filing amended returns.

How it works: The difference between the depreciation actually deducted and the amount allowable under accelerated schedules is calculated as a §481(a) adjustment. A negative adjustment (decrease in taxable income) is taken entirely in the year of change.

This is particularly valuable for owners who have owned their building for 5–10 years and missed hundreds of thousands in cumulative deductions.

Strategy 2 — Track Component Dispositions to Trigger Write-Offs

When dental office components that have been segregated are later replaced or retired—such as replacing cabinetry, updating plumbing, or renovating an operatory—the remaining depreciable basis of the old component can be written off in full at the time of disposal.

Without segregated asset tracking, these write-offs are invisible and missed. Proper tracking turns routine renovations into additional tax deductions.

Strategy 3 — Schedule Cost Segregation Strategically in High-Income Years

Timing matters. Dental practice owners who see a surge in profitability—from adding associates, opening a second location, or acquiring new equipment—can use a cost segregation study in that same year to offset the income spike with accelerated depreciation.

This reduces effective tax rate at the peak income point, preserving cash flow during expansion.

Strategy 4 — Coordinate with the CPA Annually, Not Just at Tax Filing

Cost segregation is most effective when treated as a living part of the tax plan. Annual coordination allows the owner to evaluate:

- Renovation plans

- Equipment acquisitions

- Refinancing decisions

- Expansion opportunities

Capturing reclassification opportunities as they occur—rather than retroactively—maximizes cumulative savings over time.

Strategies That Reduce Tax Costs by Changing the Structural Context Around the Practice

Operational management only goes so far. How the dental office is owned, structured, and eventually sold determines whether cost segregation benefits are fully accessible or partially trapped.

Strategy 1 — Use the Grouping Election to Neutralize Self-Rental Passive Activity Limits

Many dental practice owners hold their building in a separate LLC and lease it to their practice. Under IRS rules, rental income from property leased to a business where the owner materially participates is classified as active income, but losses remain passive.

This creates an uneven result: rental income is taxed, but depreciation losses (from cost segregation) are trapped and cannot offset practice income.

Solution: The grouping election under Treas. Reg. §1.469-4 allows the rental activity and the practice activity to be treated as a single economic unit. This converts passive losses into ordinary losses that can offset business income or W-2 wages.

Requirements:

- Activities must form an "appropriate economic unit"

- Same proportionate ownership interest in both entities

- Taxpayer materially participates in the operating trade or business

Strategy 2 — Optimize the Entity Structure to Preserve Cost Segregation Benefits

The tax treatment of accelerated depreciation deductions depends on the entity type through which the dental office is owned (S-corp, partnership, individual).

Incorrect entity structuring can trigger:

- Passive activity limitations

- At-risk rules

- Self-employment tax complications

A real estate holding entity separate from the operating practice is a common structure. When done correctly, it preserves full deductibility while maintaining liability separation.

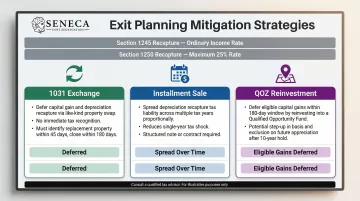

Strategy 3 — Integrate Cost Segregation into Exit and Sale Planning

Cost segregation delivers immediate tax savings, but depreciation recapture upon sale is a real consideration:

- Section 1245 property (5-, 7-year): Taxed as ordinary income to the extent of depreciation taken

- Section 1250 property (real property): Unrecaptured §1250 gain taxed at a maximum 25% rate

Mitigation strategies:

- 1031 exchanges: Defer gain and recapture by exchanging real property for like-kind real property

- Installment sales: Spread recapture tax over multiple years

- Qualified Opportunity Zone (QOZ) reinvestment: Defer eligible capital gains by investing in a QOF within 180 days

Understanding this trade-off before implementing a study allows dental office owners to model the net benefit over their expected ownership horizon.

Strategy 4 — Reinvest Tax Savings to Compound Practice Growth

The real long-term value of cost segregation is not the deduction itself but what the freed-up capital enables.

Example: A Seneca case study of a $398,600 dental office yielded $50,367 in first-year tax savings. Reinvested at an 8% annual return over 10 years, that grows to $506,778.

That's equipment upgrades, debt paydown, or a second location—financed by taxes that would otherwise have left the practice.

Conclusion

Most dental offices are depreciating assets at the slowest rate the IRS allows, even when faster, fully legal rates apply to the majority of their buildout. That gap between what owners are claiming and what they're entitled to claim is where the real tax savings live.

The strategies covered—from timing a study correctly to using the grouping election—are most effective when implemented as part of a broader tax plan. Dental practice owners who engage cost segregation as part of that plan routinely capture six-figure first-year deductions — savings that can be directed toward equipment, expansion, or debt reduction.

Take the first step by requesting a complimentary tax assessment from Seneca Cost Segregation. Beyond cost segregation, the assessment covers bonus depreciation, §179 elections, and other strategies specific to your property and practice structure.

Frequently Asked Questions

How many years do you depreciate an office building?

Nonresidential commercial real estate, including dental offices, is depreciated over 39 years under standard IRS rules using the straight-line method. However, cost segregation allows specific components of the building to be reclassified into 5-, 7-, or 15-year categories, accelerating the deduction timeline and front-loading tax savings.

Is office equipment 5 or 7 year property?

Most general office equipment is classified as 7-year property under MACRS; computers and some tech equipment qualify as 5-year property. In dental offices, specialized clinical assets—imaging systems, dental chairs, delivery units, and X-ray machines—are typically treated as 5-year property due to their specialized-use classification.

What is the $2,500 expense rule?

The IRS safe harbor under the tangible property regulations allows taxpayers to immediately expense items costing $2,500 or less per invoice or item, rather than capitalizing and depreciating them. For dental offices, this can apply to smaller equipment purchases, fixtures, or repair costs. Taxpayers with applicable financial statements may use a $5,000 threshold instead.

What is the cost segregation study in Florida?

A cost segregation study in Florida follows the same engineering-based process used nationwide, reclassifying building components into shorter depreciation categories to accelerate federal deductions. Because Florida has no state income tax, savings are concentrated at the federal level, but the methodology and benefits are identical to those available in any other state.

Can dental practices claim cost segregation on leased space?

Yes. Dental practices with significant tenant improvements or leasehold buildouts can apply cost segregation to those costs under the same accelerated depreciation rules. The IRS does not restrict cost segregation to owned buildings, so leased dental offices are fully eligible.

How much can a dental office save with cost segregation in the first year?

Savings vary based on property value and bonus depreciation rates, but dental offices routinely see 20%–40% of total buildout costs reclassified into shorter schedules. On a $1.5 million dental office, that can exceed $200,000 in first-year deductions. Seneca Cost Segregation's average first-year deduction across all property types is $171,243.